updated 1449 GMT 3rd February

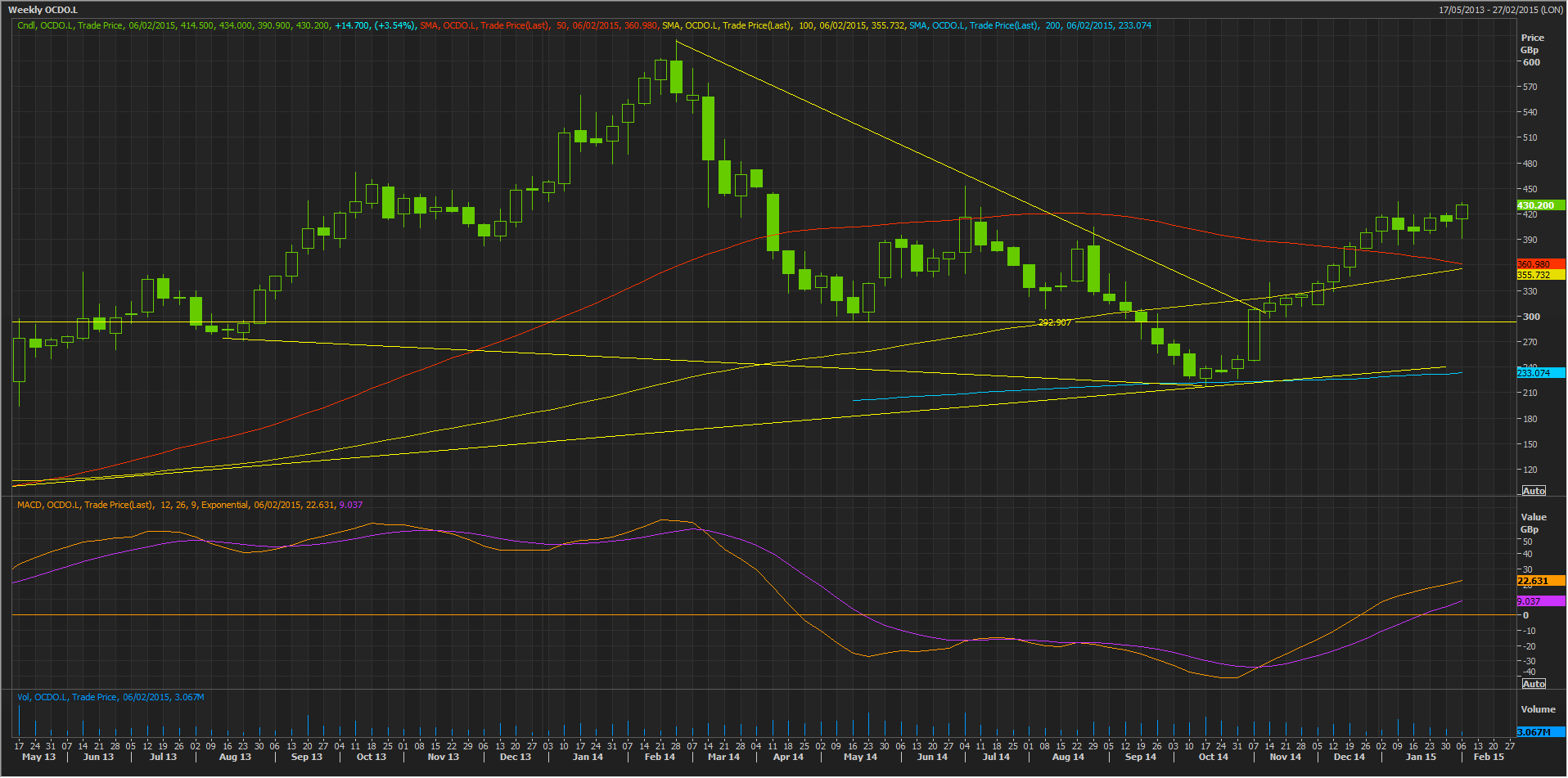

Long-suffering Ocado investors showed their displeasure at a minor let-down from the online grocery delivery company this morning, sending the shares almost 4% lower earlier.

Having been reassured Ocado would deliver its first annual profit with full-year results on Tuesday, implicitly and quite clearly by dint of the firm stating it would meet market expectations, the report turned out to have one-off items that sliced circa £3m from the widely expected £10m bottom line.

One-offs aside, and the fact that a profit had been widely expected, priced-in to an extent and that shares are 11% higher on the month, the beneficent effects of a profit are not to be sniffed at, for investors in a stock with such a solid reputation as a favoured short.

“Signficant opportunities”

After a pause for thought, investors seemed to take the glass-half-full option as the morning progressed, lifting the shares as much as 4% in the black.

Perhaps the odd judicious statement by the company helped—including that it’s “confident” of “significant opportunities” for revenue growth and “shareholder value”, it’s targeting its first third-party agreement and, perhaps most importantly for operating outlook, its CEO, “sees no reason not to continue” the Waitrose contract until 2020.

These comments help reassure the market that following an inevitable risk of anti-climax from the much anticipated maiden profit, there should be further incremental medium-term positives in the pipeline.

The market ought to also factor in the solid revenue trend, especially in light of management’s confident outlook.

Full-year saw a 19.8% rise revenues to £948m and a 15.3% advance in gross retail sales to £972m.

Ocado as tech ‘start-up’?

The firm has been careful to frame comments on opportunities “with multiple potential international partners” for the year ahead as possible “technology” deals.

Its CEO Tim Steiner struck a confident but cautious tone about these initiatives on Tuesday in comments to the media.

“We are targeting to sign the first such agreement during 2015 although there is no guarantee we can meet this timeline,” he said, adding he was talking to parties in Europe, North and Latin America and Asia.

It was with specific reference to development of an “Ocado Smart Platform” single service solution that the firm aims to “target international online retail business opportunities”, according to the statement.

Ocado has yet to break out any specific sales targets from such deals, though it continues to “enhance end-to-end technology systems” and cast a “web of (intellectual property) protection…with filing of more patents” on what it suggests are the proprietary systems it is building.

The online retailer’s 25-year agreement with Wm. Morrisons Supermarkets inked a little less than two years ago may provide a clue.

Morrisons agreed in May 2013 to pay Ocado £216m to acquire control of half of its distribution centre at Dordon in Warwickshire.

The deal included £82m for warehousing, £58m for half of the installed equipment, £16m to extend it, and a £30m licence and integration fee.

Additionally, over the next few years Morrisons said at the time it would pay £8m a year towards Ocado’s research and development costs, 1% of online sales in IT costs, a management fee equivalent to 4% of costs, and a bonus fee equal to 25% of Morrisons.com EBIT.

It’s worth bearing in mind in theory, that deal still faces a potential threat from The John Lewis Partnership.

The upmarket retailer has in the past made clear its unease with being a major Ocado supplier whilst the latter was also in partnership with a rival.

Even so, one potential reading to be drawn from Ocado’s full-year statement is that the case for Ocado being regarded more as a technology providing logistics company might be more material than before.

Has seldom looked stronger on balance

Finally, a quick look at the balance sheet suggests Ocado has never been stronger at £186.6m on standardised tangible book value as of May last year.

All in all, including strengthening evidence of nous by the current management team, led by long-time insider Tim Steiner, who relatively recently took the helm overseen by food retail grandee Stuart Rose as chairman, Ocado may never have looked in better shape.

That’s even with net debt having almost doubled to £99.4m, taking total debt closer to completely covering the value of Ocado’s equity, with implied knock-on for financing costs on top of the circa £150m capex planned for 2015.

The latter may be somewhat out of sync with the market’s spending view, whilst the Ebitda outlook could be judged as light.

The leverage picture is worth bearing in mind, especially whilst trailing and forward price/earnings are still too skewed by the company belatedly having established itself as a profit earner, if not a dividend payer.

But this is not to rain on Ocado’s parade today.

It looks like the underpinning has finally set.