November recap USD reigns but upstart Aussie takes the cake

For anyone trading FX through the month of November, the most obvious theme was the resurgence of the US dollar bullish trend. This move was […]

For anyone trading FX through the month of November, the most obvious theme was the resurgence of the US dollar bullish trend. This move was […]

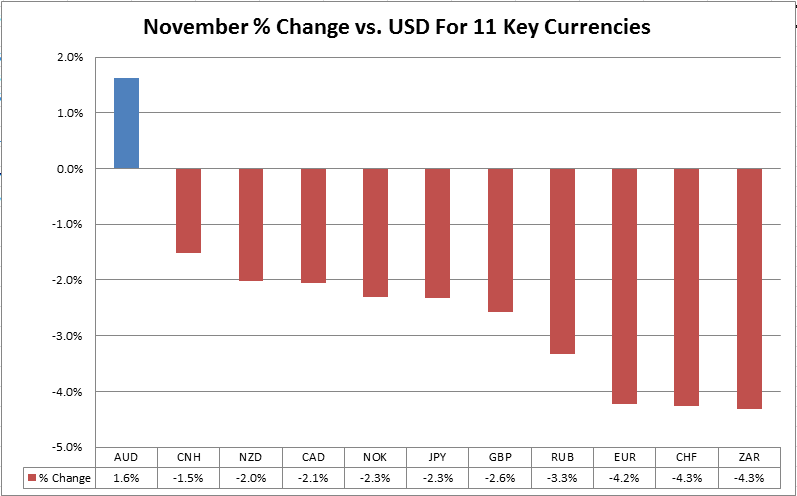

For anyone trading FX through the month of November, the most obvious theme was the resurgence of the US dollar bullish trend. This move was driven almost exclusively by increasing expectations that the Federal Reserve would raise interest rates at its upcoming December meeting, and throughout the month, economic data continually reinforced this view.

The dollar’s explosive November started out with the blowout October NFP report, which showed 271k new jobs created, carried through last week’s solid GDP reading, and was supported by hawkish Fedspeak throughout, to the point that Fed Funds futures traders are now pricing in a 78% probability that the FOMC hikes interest rates in two weeks. While we believe that the dollar’s rally could stretch further in the run-up to the Federal Reserve’s highly-anticipated meeting on December 16, the greenback may struggle in the latter half of the month with the most obvious bullish catalyst behind us and generally slow holiday trading conditions.

Meanwhile, one development that caught a lot of traders off guard last month was the surprise rally in the Australian dollar against all the other major currencies, including the dollar. Even before last night’s optimistic economic assessment by the RBA and solid PMI figures out of China, the Aussie was supported by decent data. The highlight of the month was no doubt the stellar mid-month labor market report, which drove unemployment rate from 6.2% to 5.9% Down Under.

Heading into the month, many analysts assumed that the RBA would be forced to cut interest rates before 2016, but after the raft of strong economic data, some are now suggesting that the RBA’s next move may be to hike interest rates, an inconceivable notion five weeks ago. The Australian dollar’s outperformance last month shows that it’s not the absolute position of central bank policy that drives currency values, rather how the expectations for monetary policy evolve relative to the market’s expectations. With the Aussie peeking out above a 14-month bearish trend line off the September 2014 highs up at .9400, we could see more short-term strength in the Aussie moving forward, especially if China’s economy shows signs of accelerating once again and/or the price of industrial metals bounces.