No FOMC Existing Exit Strategy

As powerful as the Fed’s December decision to go “all in” via its $85bn in monthly asset purchases, evidence is increasingly showing that such aggressive […]

As powerful as the Fed’s December decision to go “all in” via its $85bn in monthly asset purchases, evidence is increasingly showing that such aggressive […]

As powerful as the Fed’s December decision to go “all in” via its $85bn in monthly asset purchases, evidence is increasingly showing that such aggressive easing may have been supported by a slim majority inside the FOMC.

The most immediate question in reaction to yesterday’s market-moving FOMC minutes is:

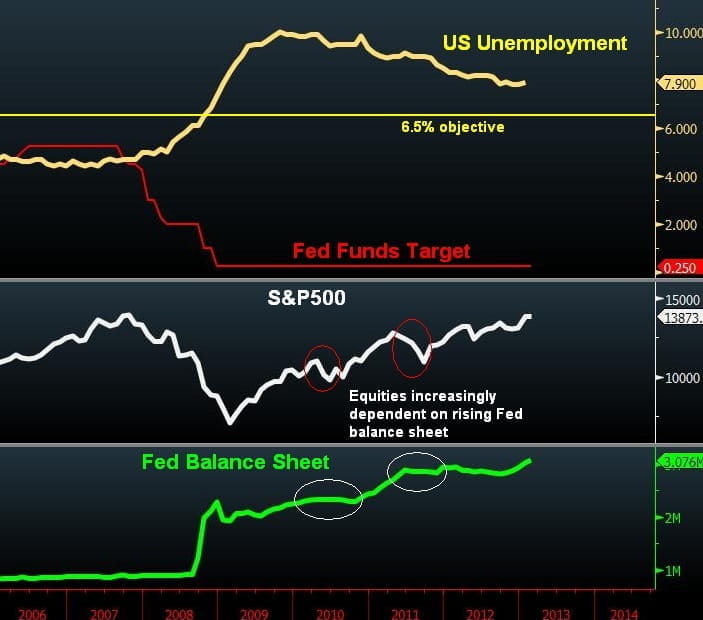

How can the Fed bring about a decline in the unemployment rate to the 6.5% target from the current 7.9% while considering the slowdown or ending of asset purchases?

The contraction in Q4 GDP may end up being reversed by the improving December international trade figures, but today’s release of eight-month lows in the Philly could be a sign of things to come if the $1.2 trn spending cuts sequester goes into effect next month. If the sequester deadline is averted as all dangerous US fiscal deadlines have proven to be in the past two years, then the Fed may afford to signal slowing the pace of asset purchases as the economy will be spared an 8% erosion from the overall economy.

But “signalling” a slowdown in asset buys is all the Fed can do at this point—at a time when global central banks are increasingly resorting to monetary easing while the much needed fiscal tightening risks a renewed global growth contraction.

No Existing Exit Strategy

Last but not least, the Fed’s shift towards an implicit targeting of 6.5% unemployment rate leaves precludes the case for any normalisation (not to mention tightening)—especially as the rate currently stands at 7.9%. In fact, a decline of such magnitude in unemployment has historically taken as long as two years.

This is by no means 1994, 1999 or 2004, when Fed tightening cycles were delivered during a strengthening US economy and stabilising global conditions.

But this time it is different.

Global equities may be nearing record highs, but neither is the US nor the global economy equipped with robust conditions meriting a normalisation in monetary policy at a time of tightening fiscal conditions, a quadruple dip-bound UK economy and a barely recession-exiting Japanese economy. And so, even if the dovishly-slanted FOMC of 2013 takes the improbable decision of voting for slower asset purchases in H2, the reactionary pullback in asset markets combined with an already weak consumer fabric will shall make a full exit premature.

All that Bernanke can do in next week’s Congressional testimony is to list the possible risks of continuing asset purchases forever, but implementing any exit is not at all in the cards.