August 16, 2021 2:23 AM

Key Asian equity indices are mostly trading lower today, likely in some part a delayed response to Friday's University of Michigan's index of consumer sentiment that declined by 11.0pt to 70.2, the lowest level since 2011 on concerns over the virus's resurgence.

Also playing a part in today's falls, evidence that slowing global demand and rising delta cases are hindering the reopening of the Chinese economy as activity data released earlier today was significantly weaker than expected.

Retail sales increased by 8.5% in July, well below the 12.1% rise viewed in June. Industrial production increased 6.4% versus the median estimate of 7.9% and well below Junes 8.3% rise. The unemployment rate rose to 5.1% from 5.0% in June.

All of this has overshadowed preliminary Q2 Japanese GDP data released this morning, which showed a stronger than expected annualized gain of 1.3%. Robust private consumption helped the Japanese economy avoid slipping back into recession following its -3.9% fall in Q1.

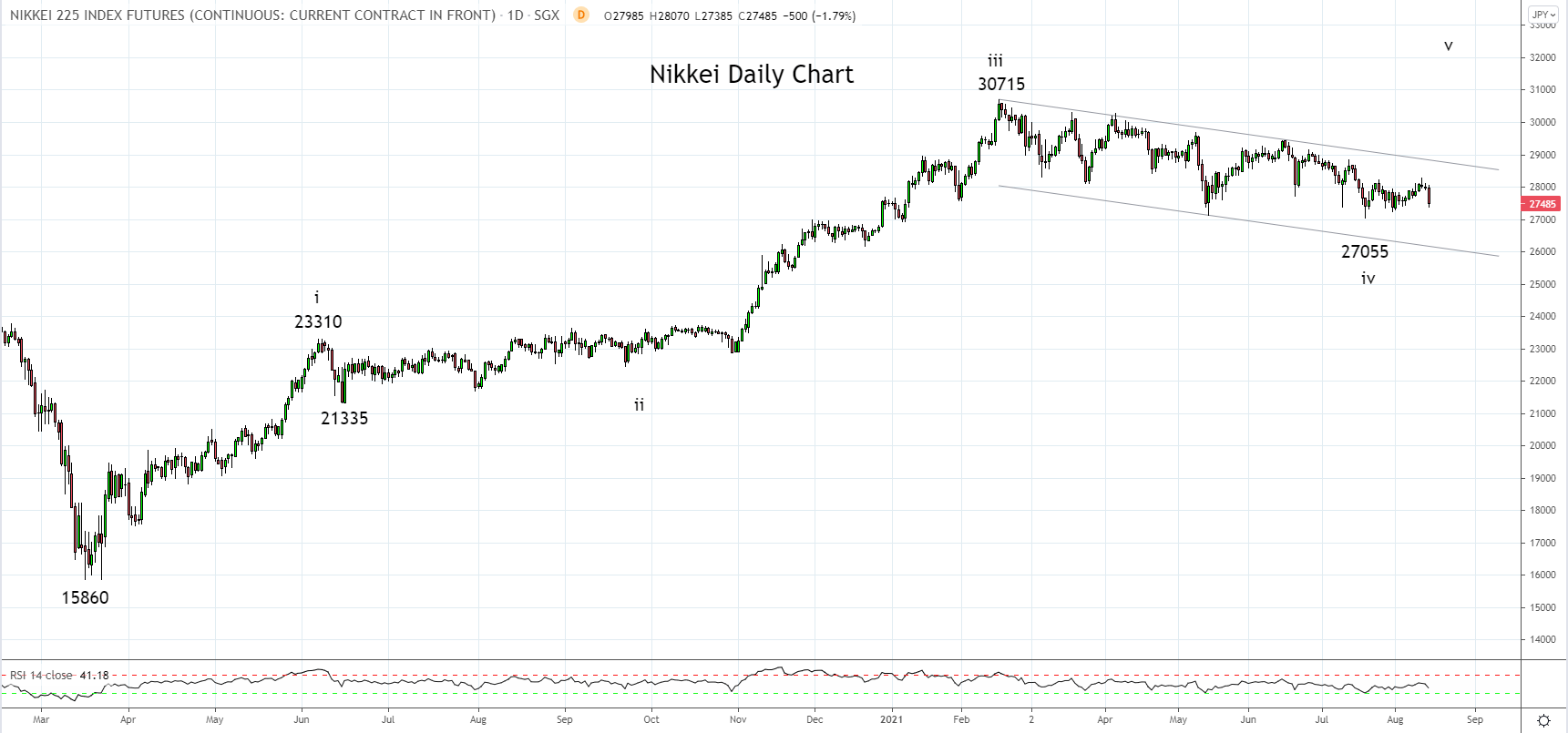

However, with virus cases also rising sharply in Japan, the Nikkei 225 has been caught up in the downdraft of negative sentiment to be trading down -1.95% at 27740 as we go to press.

After reaching its highest level since 1990 in February this year, the Nikkei has spent the past six months correcting the strong run higher, within a trend channel viewed on the chart below.

Horizontal support is viewed at 27,000, however, should that level break, there is room for the decline to extend towards trend channel support near 26,000, which is the medium-term buying level.

Aware that if the Nikkei breaks and closes above trend channel resistance at 28,900, it would signal the correction is complete, and the uptrend has resumed.

Source Tradingview. The figures stated areas of 16th of August 2021. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM