NFP Recap Good enough for the Fed

After yesterday’s massive ECB-induced moves across all markets, traders were a bit shell-shocked heading into the always important Non-Farm Payrolls report. Today’s jobs report was […]

After yesterday’s massive ECB-induced moves across all markets, traders were a bit shell-shocked heading into the always important Non-Farm Payrolls report. Today’s jobs report was […]

After yesterday’s massive ECB-induced moves across all markets, traders were a bit shell-shocked heading into the always important Non-Farm Payrolls report. Today’s jobs report was even more highly anticipated than usual because it represented the last major US economic release ahead of the Fed’s December monetary policy meeting, where the central bank is mulling its first interest rate hike in nearly a decade.

As we noted in our NFP Preview report though, the stakes may not have been as high as they appeared: after all, recent comments (including from Fed Chair Janet Yellen herself) heavily hinted at an interest rate hike, so it likely would have taken a truly disastrous jobs report to call that plan into question.

Even to the most skeptical of traders, today’s Non-Farm Payroll report was far from disastrous. The US economy created 211k jobs in the month of November, slightly better than the 201k anticipated. Furthermore, revisions added 35k jobs to the previous two months’ reports.

The details under-the-hood were similarly solid. The unemployment rate held steady at 5.0%, though average hours worked dipped modestly to 34.5 hours. Crucially, average hourly earnings rose 0.2% m/m, as expected; this measure is closely watched by the Federal Reserve as a leading indicator for inflation and points to the potential for price pressures to pick up moving forward.

In sum, this jobs report should be “good enough” for the Federal Reserve to go ahead and raise interest rates at its meeting in two weeks, especially with given the big rise in EUR/USD (and therefore pullback in the value of the dollar) yesterday. Fed Funds futures traders seem to agree, with the implied odds of an interest rate hike ticking up to 79% in the wake of the release, according to the CME’s FedWatch tool. In our view, this number could rise further in the coming days, supporting the dollar, especially if Fed officials continue to strike a hawkish tone.

Market Reaction

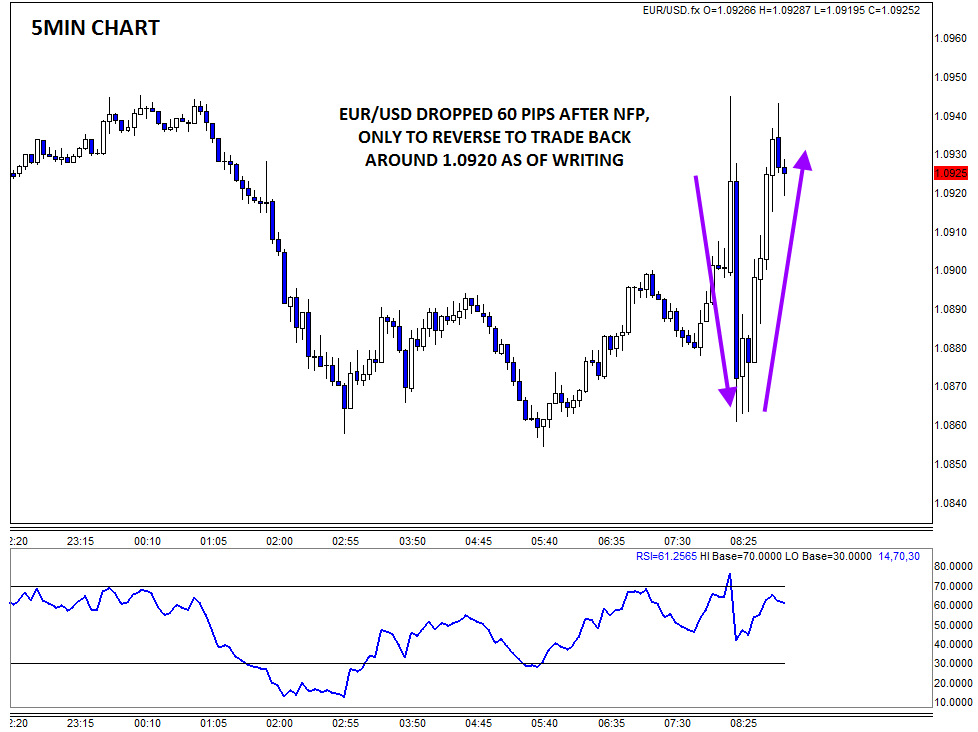

The market reaction to the NFP release was muted, at least in relation to yesterday’s big moves. The dollar initially rose 40-60 pips against the euro and the yen, though those moves have been almost completely unwound as of writing. US equities dropped on the now more likely prospect of tighter monetary policy and now point to an essentially flat open. Bond yields saw a quick spike that has since been unwound, much like the FX market. Finally, gold is trading counter-intuitively higher, while oil is on the back foot ahead of a key OPEC meeting later today.