NFP Recap Could the Huge NFP Beat Help Sway the Fed

While the headline Non-Farm Payrolls (NFP) number came out on Friday way ahead of expectations at 287K jobs added in June against prior forecasts of […]

While the headline Non-Farm Payrolls (NFP) number came out on Friday way ahead of expectations at 287K jobs added in June against prior forecasts of […]

While the headline Non-Farm Payrolls (NFP) number came out on Friday way ahead of expectations at 287K jobs added in June against prior forecasts of 175K, other aspects of the US Labor Department’s report were not as rosy. May’s data was revised down from an already-dismal 38,000 to an even worse 11,000. The unemployment rate in June rose to 4.9% against the 4.8% expected, offsetting May’s better-than-expected 4.7%. Average hourly earnings also fell short of expectations, increasing by only 0.1% in June vs forecasts of 0.2%.

Although this data has created somewhat of a mixed employment picture, the unexpectedly sizeable increase in jobs for June has undoubtedly highlighted May’s bleak data as a likely anomaly within an otherwise healthy US labor market on a path to full employment. If this is considered as such from the perspective of the Federal Reserve, there could yet be hope for at least one interest rate hike this year.

After the pivotal Brexit vote in the UK two weeks ago, the probability of a near-term Fed rate hike has decreased dramatically. As time passes and effects of the EU referendum on the US markets continue to fade, however, the Fed’s focus has begun to turn back to three primary criteria for monetary policy tightening: rising US economic growth, further improvements in the labor market, and increasing inflation.

While June’s much-better-than-expected jobs data has helped support the labor market criterion, however, it is highly unlikely that it will be sufficient in itself in swaying the Fed to raise rates during its next meeting in late July. Rather, it will likely require continued evidence of positive economic data in the months to come, including solid NFP numbers, in order to convince the Fed that a rate hike would be appropriate. Depending on upcoming data, this could potentially occur as early as the September FOMC meeting.

As for the market reactions to Friday’s employment data, the US dollar initially surged as expected before paring most of its gains. Gold plunged immediately from near its new two-year high around $1375 before rebounding once again. Perhaps the most sustained market reaction, however, occurred in the global stock markets. US and European stock indexes surged broadly on the upbeat US employment data, with the S&P 500 rising by over 1%, well above the key 2100 level. This surge extends the post-Brexit rebound for US equities, completely erasing the losses that occurred in the immediate aftermath of the UK’s EU referendum.

Going forward, while the Fed should continue to be dovish and cautious for the near-term, Friday’s optimistic employment data could very well have begun to offer some solid support for a rate hike towards the latter part of the year, provided that data releases in upcoming months continue to show a trend of economic and employment growth.

USD/JPY

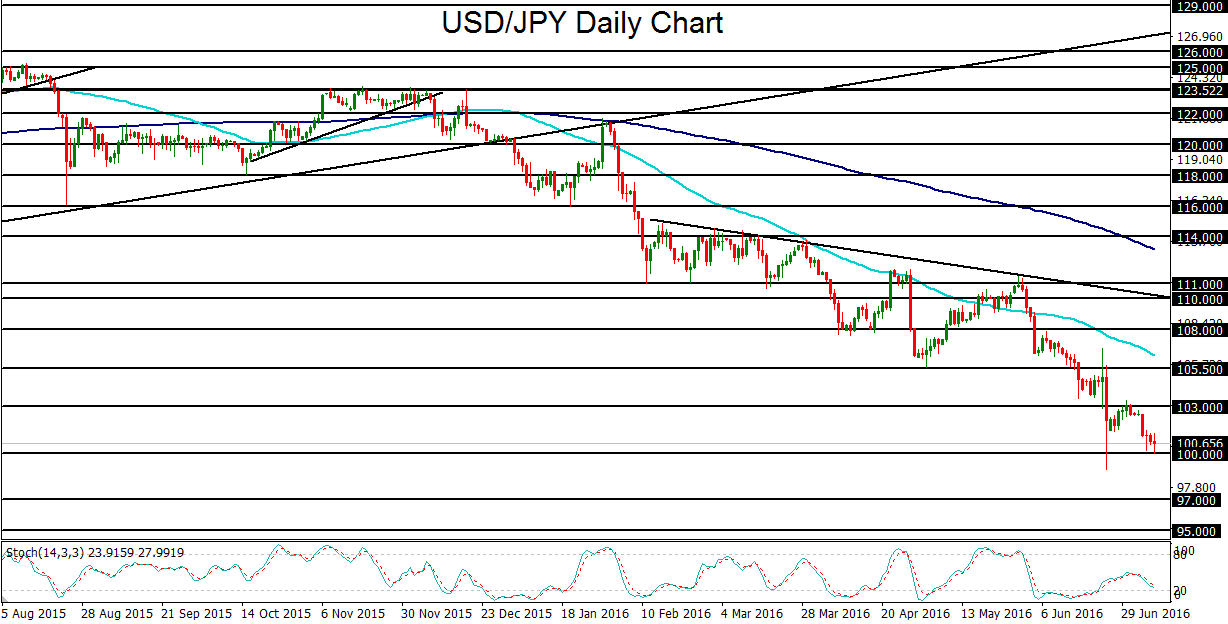

The Japanese yen has clearly made remarkable strides in the past several months against its major rivals, including the US dollar, euro, and British pound. In the case of USD/JPY, the currency pair has dropped within the past week to re-approach the major 100.00 support level, which is not far off from the post-Brexit low just below 99.00 that occurred only two weeks ago. Prior to dropping back down towards 100.00, USD/JPY rebounded to key resistance around 103.00 at the end of June before retreating once again. Since late last year, the currency pair’s downtrend has been sharp and often rapid, which brings to the fore questions on whether and when Japan may step-in to intervene in an attempt to weaken its currency. The psychological 100.00 mark on USD/JPY has long been seen by traders as the key “line-in-the-sand” in terms of the potential risk of Japanese intervention. More likely, however, Japanese officials are watching the speed of yen appreciation, rather than the precise level, to decide on when an intervention might be appropriate. Therefore, while such an intervention is always possible below 100.00, which could lead to a sharp rebound for USD/JPY, the currency pair could well have further to fall before such an event occurs. With any sustained breakdown below 100.00 support, the next major downside target is at the key 97.00 support level.