October 8, 2021 6:28 PM

Non-Farm payrolls released earlier today showed that the US added +194,000 jobs to the economy for the month of September vs an estimate of +500,000. (See our NFP preview here) The Unemployment Rate for September dropped to 4.8% from 5.2% in August and Average Hourly earnings increased by 0.6% vs 0.4% the prior month. The Fed will be pleased to see that wages are increasing with other signs of inflation.

With the big miss in the headline print, one would think that the Fed may be ready to give pause in their decision making regarding the Fed’s consideration to taper bond purchases at the November 3rd meeting. However, it’s important to note that although the headline number was much worse then expected, August’s print was upwardly revised from +235,000 to +366,000. For the revision to be reflected in September’s print, the difference between August’s original value and the revised value (+131,000) should be added to September’s number. Therefore, although the BLS released a headline number of +194,000, when considering the August revision, the number is more like +325,000. Although this still misses expectations, it still seems ”in the realm of positive jobs data” for the Fed to announce tapering at their next meeting. (Remember, Powell seemed to have almost ignored the +235,000 original August print).

Trade USD/JPY now: Login or Open a new account!

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

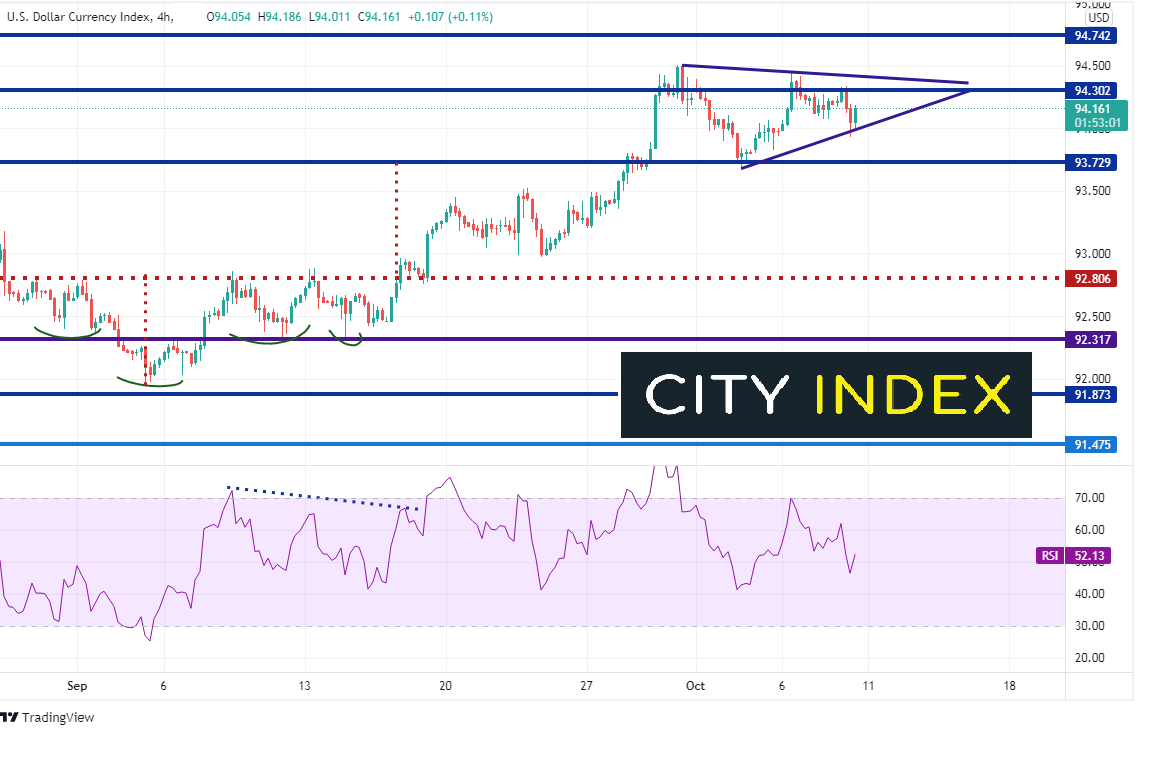

Thus far in October, the US Dollar Index (DXY) had been consolidating September gains between 93.68 and 94.50. Today, the DXY is currently near unchanged as the data appears to be giving mixed signals to US Dollar traders. On a 240-minute timeframe, DXY has been hovering near the highs from November 2020. If markets continue to feel that the Fed is going to announce tapering at the November meeting, the DXY could continue to move higher (as stock markets move lower). Resistance is at the highs of September 30th near 94.50, and then the highs from September 2020 at 94.72. Support is below today’s lows at the upward sloping trendline of a symmetrical triangle at 93.74 and then the previous neckline of an inverse head and shoulders at 92.80.

Source: Tradingview, Stone X

What is the US Dollar Index (DXY)?

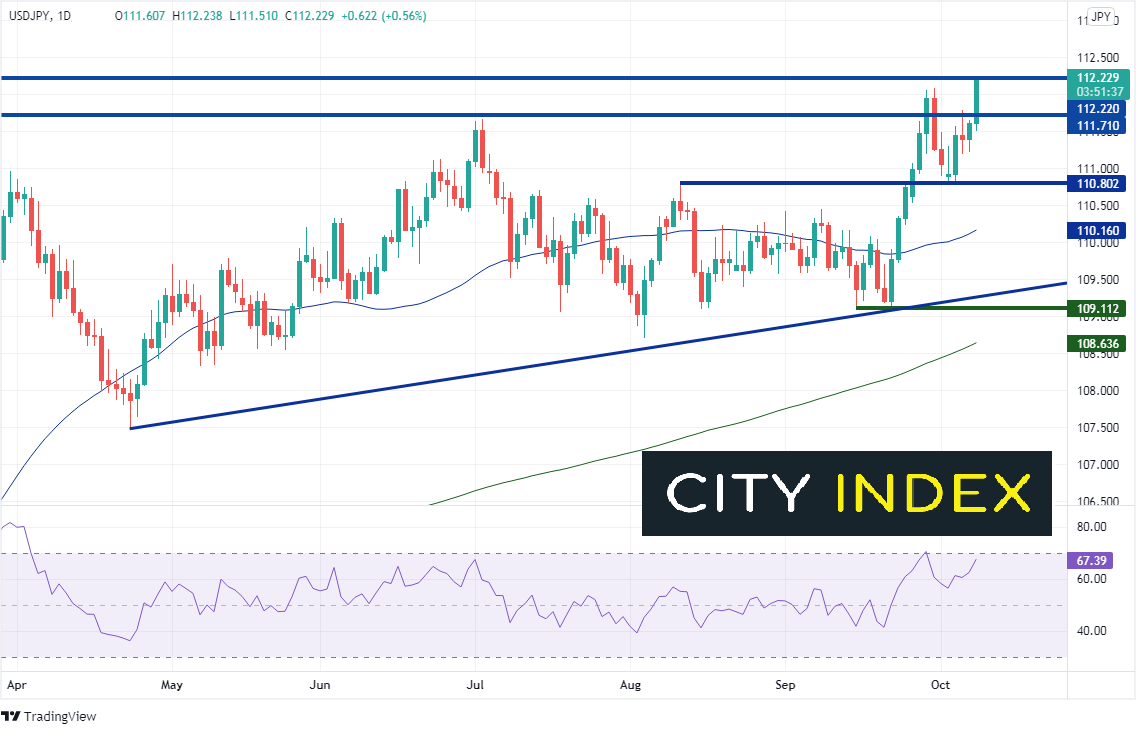

USD/JPY typically moves in concert with US 10-year yields. Rates are moving higher after the NFP print today and USD/JPY has moved with them. The current correlation coefficient is +0.97, which is extremely high. With 10-year yields moving above 1.6% today (bonds selling off on tapering fears), USD/JPY has risen above 112.00, and is testing highs from February 2020 at 112.22. The 127.2% Fibonacci extension from the July 2nd highs to the August 4th lows is at 112.16 and the 161.8% Fibonacci extension is at 113.47. However, notice that RSI is diverging from price, indicating USD/JPY may be ready for a pullback. Support is at the July 2nd highs near 111.65 and then he August 11th highs at 110.80.

Source: Tradingview, Stone X

Next week, there should be continued market digestion of the NFP numbers and questions as to how the Fed will respond to the miss (and the higher revision). If markets think Fed will announce a taper, the US Dollar and USD/JPY should continue to climb. However, if markets feel there wasn’t enough in the NFP print to allow the Fed to taper, watch for the US Dollar and rates to pull back!

Learn more about forex trading opportunities.

Latest market news

Today 11:30 AM

Today 08:18 AM

Yesterday 10:40 PM