NFP preview: When will jobs growth get back into gear?

Overview

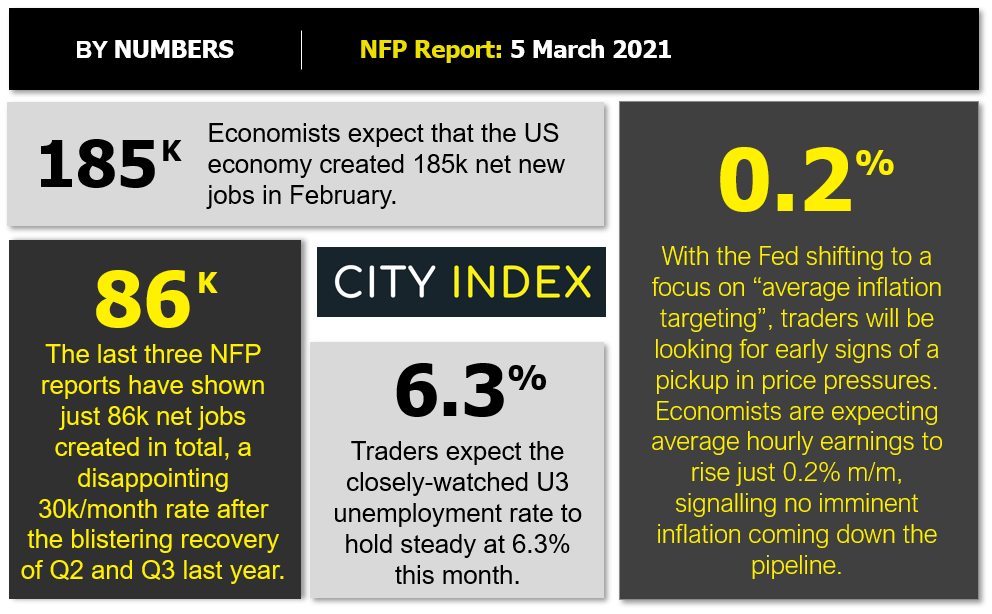

After a blistering recovery from the pandemic-induced recession through Q2 and Q3 of last year, the US labor market has downshifted sharply. Over the last three months, the NFP report has shown total job creation of just 86k jobs, a pitiful pace of less than 30k net new jobs per month.

Despite the lackluster employment figures of late, economists are optimistic that the US economy will start to accelerate sharply in the coming months as vaccinations pick up and another (likely) stimulus bill gets approved by Congress. For the month of February, economists are anticipating a 185k reading in Non-Farm Payrolls, with average hourly earnings expected to rise 0.2% m/m again this month.

Source: StoneX

Are these expectations justified? We dive into the key leading indicators for Friday’s critical jobs report below!

NFP forecast

As regular readers know, there are four historically reliable leading indicators that we watch to help handicap each month’s NFP report:

- The ISM Non-Manufacturing PMI Employment component slipped to 52.7, down from last month’s 55.2 reading.

- The ISM Manufacturing PMI Employment component improved modestly, rising to 54.4 from last month’s 52.6 reading.

- The ADP Employment report came in at just 117k net new jobs below expectations and last month’s upwardly-revised 195k print.

- Finally, the 4-week moving average of initial unemployment claims fell to 791k, down notably from last month’s 857k reading.

As we’ve noted repeatedly over the last few months, traders should take any forward-looking economic estimates with a massive grain of salt given the truly unparalleled global economic disruption as a result of COVID-19’s spread. That said, weighing the data and our internal models, the leading indicators point to a worse-than-expected reading from the February NFP report, with headline job growth potentially coming in somewhere in the 50-150k range, albeit with a bigger band of uncertainty than ever given the current state of affairs.

Regardless, the month-to-month fluctuations in this report are notoriously difficult to predict, so we wouldn’t put too much stock into any forecasts (including ours). As always, the other aspects of the release, prominently including the closely-watched average hourly earnings figure, will likely be just as important as the headline figure itself.

Potential NFP market reaction

|

|

Earnings <0.1% |

Earnings 0.1-0.3% |

Earnings > 0.3% |

|

< 140k jobs |

Bearish USD |

Slightly bearish USD |

Neutral USD |

|

140k-220k jobs |

Slightly bearish USD |

Neutral USD |

Slightly bullish USD |

|

> 220k jobs |

Neutral USD |

Slightly bullish USD |

Bullish USD |

After getting walloped through the last three quarters of 2020, the US dollar has stabilized against its major rivals so far in 2021, though the world’s reserve currency hasn’t seen much in the way of buying pressure lately.

If we see a stronger-than-anticipated NFP reading, traders may look to the EUR/USD as a possible sell candidate. The world’s most widely-traded currency pair is approaching the bottom of the 1.1950-1.2225 range that has contained rates for the past seven weeks, an da break below that area could open the door for a deeper retracement toward 1.1800 as we move through the month of March.

On the other hand, GBP/USD is poised to benefit from a potentially soft US jobs report. The pair is riding its 21-day EMA higher and has shown signs of forming a based this week after pulling back from last week’s multi-year highs. A weak jobs report could be just the bullish catalyst that cable needs to resume its established uptrend.

Learn more about forex trading opportunities.

Latest market news

Yesterday 08:33 AM

Latest Forex articles

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM

April 16, 2024 12:00 PM

April 16, 2024 04:24 AM