NFP Preview: Weak Labor Market May Outweigh GM-UAW Boost

Every month, we remind traders that the Non-Farm Payrolls report is significant because of how it impacts monetary policy. In other words, the Fed is the “transmission mechanism” between US economic reports and market prices, so any discussion about NFP should start with a look at the state of the US central bank.

Last month, we compared the Fed’s announcement of a solidly neutral outlook toward monetary policy to a bridesmaid upstaging the bride (the NFP report) at her own wedding. While we can’t torture the analogy any further, the Fed’s high bar to raising or lowering rates may still tamp down market volatility around this month’s NFP report.

NFP Forecast

At least this time around we have access to all four of the historically-reliable leading indicators for the NFP report:

- The ISM Manufacturing PMI Employment component printed at 46.6, down from last month’s 47.7 reading.

- The ISM Non-Manufacturing PMI Employment component came in at 55.5, up from last month’s 53.7 reading.

- The ADP Employment report dropped to just 67k, below both expectations and the downwardly-revised 121k reading from last month.

- The 4-week moving average of initial unemployment claims rose to 217,750, up from 214,750 last month.

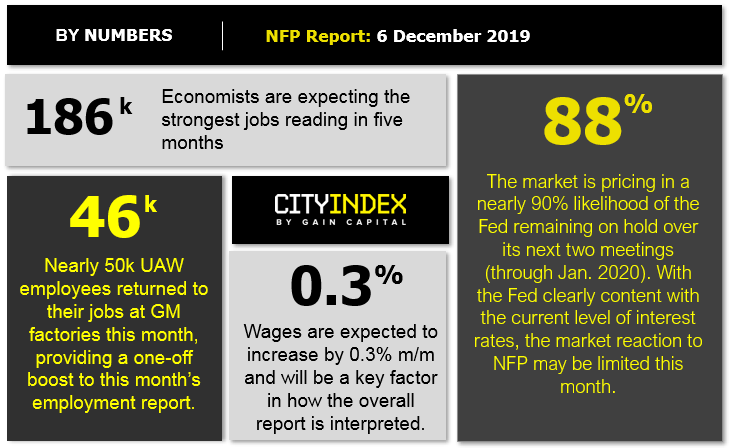

In other words, three of the four leading indicators are pointing to a deteriorating labor market. That said, this month’s report may benefit from the 46,000 United Auto Workers returning to General Motors, a temporary factor that hurt last month’s jobs report. Weighing these factors, we believe the odds are tilted toward a slight disappointment in overall job growth, with internal models pointing toward headline job creation in the 130k-180k range, albeit with more uncertainty than usual.

Regardless, the month-to-month fluctuations in this report are notoriously difficult to predict, so we wouldn’t put too much stock into any forecasts (including ours). Most importantly, readers should note that the unemployment rate and (especially) the wages component of the report will also influence how traders interpret the strength of the reading.

Potential Market Reaction

See wage and job creation scenarios, along with the potential bias for the USD dollar below:

|

Earnings < 0.2% m/m |

Earnings = 0.3% m/m |

Earnings > 0.4% m/m |

|

|

< 150k jobs |

Bearish USD |

Neutral USD |

Slightly Bullish USD |

|

150-225k jobs |

Slightly Bearish USD |

Neutral USD |

Bullish USD |

|

>225k jobs |

Neutral USD |

Slightly Bullish USD |

Strongly bullish USD |

In the event the jobs and the wage data beat expectations, then we would favor looking for short-term bullish trades in USD/JPY, which remains in a near-term uptrend and is testing support in the 108.00s. But if the jobs data misses expectations, then we would favor looking for bullish trades in NZD/USD, which recently saw a major breakout to 4-month highs and may have further to run from here.

Latest market news

Yesterday 10:36 PM

Yesterday 05:36 PM

Yesterday 05:00 PM

Yesterday 01:31 PM

Yesterday 12:26 PM

Yesterday 11:30 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM