NFP preview: Fed needs to see job growth maintained

Overview

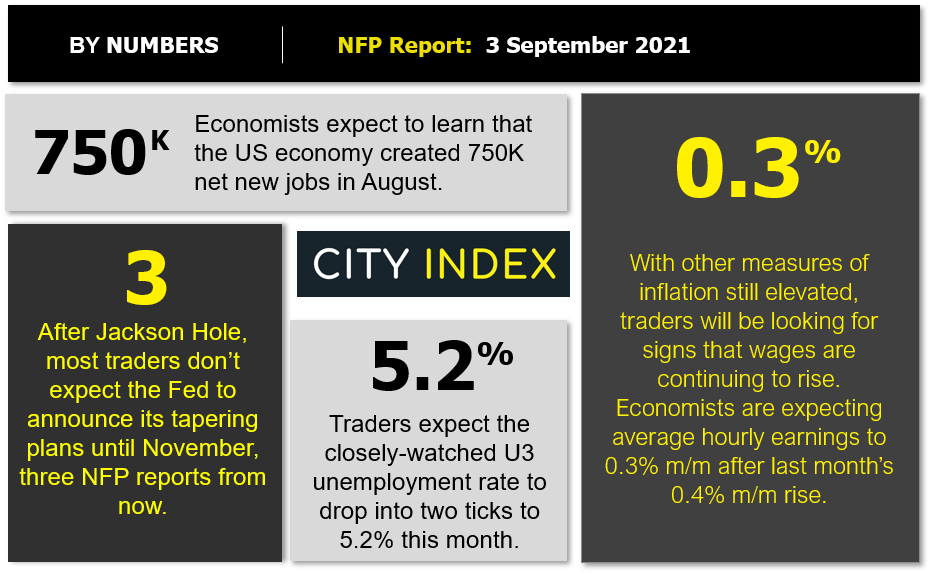

In the wake of last week’s cautious economic assessment from Fed Chairman Jerome Powell, most market watchers aren’t expecting the US central bank to announce its taper plans until its November meeting at the earliest, a full three Non-Farm Payroll (NFP) reports from now. Nonetheless, traders will still key in on Friday’s big jobs report to see if the labor market is recovering as expected or whether further delays may in the cards.

After back-to-back readings above 900K net new jobs, traders and economists are expecting “just” 750K jobs this month, with the average hourly earnings figure expected to rise 0.3% m/m, a tick down from recent readings:

Source: StoneX

Are these expectations justified? We dive into the key leading indicators for Friday’s critical jobs report below!

NFP forecast

As regular readers know, we focus on four historically reliable leading indicators to help handicap each month’s NFP report, but due to the vagaries of the economic calendar, we won’t get access to the ISM Services PMI report until after the NFP report:

- The ISM Manufacturing PMI Employment component printed at 49.0, down nearly 4 points from last month’s 52.9 reading.

- The ADP Employment report came in at 374K net new jobs, well below last month’s downwardly-revised 326K reading.

- Finally, the 4-week moving average of initial unemployment claims fell sharply to 355K from last month’s 394K reading.

As a reminder, the state of the US labor market remains more uncertain and volatile than usual as it emerges from the unprecedented disruption of the COVID pandemic. That said, weighing the data and our internal models, the leading indicators point to a below expectations reading in this month’s NFP report, with headline job growth potentially coming in somewhere in the 500-700k range, albeit with a bigger band of uncertainty than ever given the current global backdrop.

Regardless, the month-to-month fluctuations in this report are notoriously difficult to predict, so we wouldn’t put too much stock into any forecasts (including ours). As always, the other aspects of the release, prominently including the closely-watched average hourly earnings figure which rose 0.4% m/m in August, will likely be just as important as the headline figure itself.

Potential NFP market reaction

|

|

Earnings < 0.2% m/m |

Earnings = 0.3% m/m |

Earnings > 0.4% m/m |

|

< 650K |

Bearish USD |

Slightly Bearish USD |

Neutral USD |

|

650K-850K |

Slightly Bearish USD |

Neutral USD |

Slightly Bullish USD |

|

> 850K |

Neutral USD |

Slightly Bullish USD |

Bullish USD |

After peeking out to new year-to-date highs above 93.40 late in August, the US dollar index has reversed sharply to the downside and is currently testing its 1-month low at 92.50.

In terms of potential trade setups, readers may want to consider EUR/USD sell opportunities on a strong US jobs report. In that scenario, the worlds most widely-traded currency pair could reverse off resistance in the upper-1.1800s and drop back below 1.1800 heading into next week.

Meanwhile, a weak jobs report could present a sell opportunity in USD/CAD. The North American pair is testing rising trend line support near 1.2600, and a break below that support level could lead to a quick continuation toward the 100-day EMA near 1.2500 next.

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 08:33 AM

Latest Forex articles

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM

April 16, 2024 12:00 PM

April 16, 2024 04:24 AM