NFP preview Do payrolls matter for the dollar

All eyes will be on the US Labour Market report this coming Friday at 1330 GMT. The market is expecting a 175k increase in the […]

All eyes will be on the US Labour Market report this coming Friday at 1330 GMT. The market is expecting a 175k increase in the […]

All eyes will be on the US Labour Market report this coming Friday at 1330 GMT. The market is expecting a 175k increase in the Non-Farm Payrolls figure for January, which is higher than the 156k reported for December. The unemployment rate is expected to remain at 4.7%, and earnings growth is expected to fall back slightly to 2.8%, which would still be one of the highest levels for 8 years.

The leading employment indicators for the US lean heavily towards an even larger than expected NFP report for January. The ADP measure of private sector employment rose by 246k last month, the largest monthly increase since June 2016. Also, the employment component of the ISM manufacturing survey rose to its highest level since 2014. Unfortunately the most accurate lead indicator, the ISM non-manufacturing index, will be released after the NFP report on Friday afternoon.

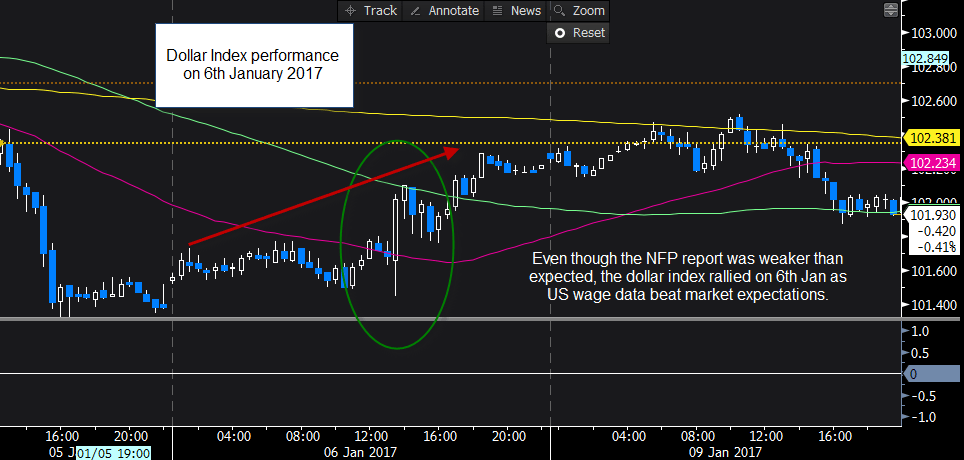

The dollar and NFPs

The dollar is very sensitive to US labour market reports, but even if the headline NFP number disappoints for another month, this does not mean that the US dollar will nose-dive. On 6th January 2017, the date of the last NFP release, the dollar actually rose even though NFPs were weaker than expected (see chart below). Stronger wage data was considered more important by investors and actually lifted the greenback. It is worth remembering that labour market data and its impact on the dollar is not only determined by NFPs, wage data can override concerns about the pace of job growth as it can lift expectations of interest rate hikes from the Federal Reserve, which tend to be dollar positive.

Labour market reports can also be volatile. Historically, January can be a weak month for job growth in the US as seasonal workers get laid off after the Christmas holiday and NFPs can typically see more downside surprises compared to later months of the year. However, an upside surprise to NFPs in a month like January could trigger a dollar rally that may last for the medium-term.

Potential market reactions:

The dollar has had a bad start to January, and is on the back-foot as we lead up to this NFP report. As mentioned above, a mediocre NFP report but strong wage data could trigger a move back above the key 100.00 level and towards the 50-day sma at 101.53, while weak NFP and wage growth could see a break below key support at 99.25 – the 38.2% retracement of the April 2016 low to the early January 2017 high – which would dampen the prospects for the greenback for the medium term.

Figure 1:

Source: City Index and Bloomberg