NFP Preview: Bounce back likely after last month’s disappointing reading

Overview

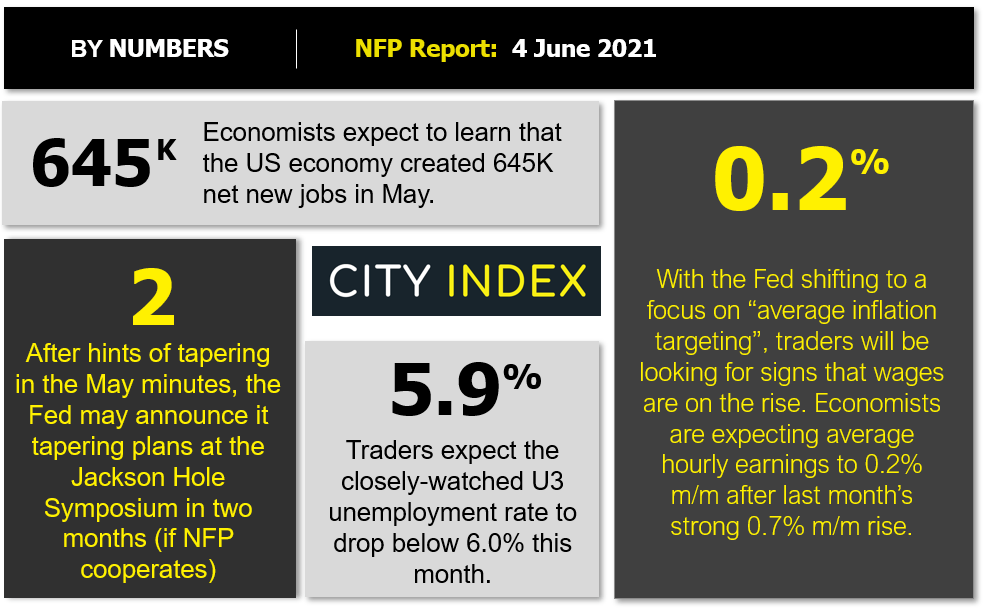

For traders and policymakers that were expecting strong growth of nearly 1M net new jobs, last month’s soft NFP report was an unexpected gut punch. As the graphic below shows, traders have tempered their optimism for this month’s report, which will be more significant than usual as the Fed watches employment and inflation closely as it evaluates when to start tapering its asset purchases:

Source: StoneX

Are these expectations justified? We dive into the key leading indicators for Friday’s critical jobs report below!

NFP forecast

As regular readers know, we focus on four historically reliable leading indicators to help handicap each month’s NFP report:

- The ISM Non-Manufacturing PMI Employment component printed at 55.3, down more than 3% from last month’s 58.8 reading.

- The ISM Manufacturing PMI Employment component printed at 50.9, down more than 4% from last month’s 55.1 reading.

- The ADP Employment report came in at 978K net new jobs, a big improvement over last month’s downwardly-revised 654K reading.

- Finally, the 4-week moving average of initial unemployment claims fell to 428K, down sharply from last month’s 612K reading.

As we were reminded last month, the state of the US labor market remains more uncertain and volatile than usual as it emerges from the unprecedented disruption of the COVID pandemic. That said, weighing the data and our internal models, the leading indicators point to a roughly as-expected reading in this month’s NFP report, with headline job growth potentially coming in somewhere in the 550k-650k range, albeit with a bigger band of uncertainty than ever given the current state of affairs.

Regardless, the month-to-month fluctuations in this report are notoriously difficult to predict, so we wouldn’t put too much stock into any forecasts (including ours). As always, the other aspects of the release, prominently including the closely-watched average hourly earnings figure which rose 0.7% m/m in April, will likely be just as important as the headline figure itself.

Potential NFP market reaction

The greenback dropped against most of its major rivals through the first half of May, largely as a result of last month’s disappointing NFP report, before stabilizing in the final couple of weeks.

USD/CAD is a pair that we highlighted last week as a candidate that could see a short-term rally on any positive US or negative Canadian data (note that the Canadian jobs report will be released at the same time as NFP).

Meanwhile, a weaker-than-anticipated jobs report could present a buy opportunity in GBP/USD, which has spent the last three weeks consolidating in a tight range below multi-year highs in the 1.4200 region. A fundamentally-driven breakout in the pair would confirm the longer-term uptrend and could be the catalyst for bulls to set their sights on the five-year highs in the mid-1.4300s.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM