NFP Preview: Another Weak Report Could Cement a Fed Rate Cut This Month

Background

Every month, we remind traders that the Non-Farm Payrolls report is significant because of how it impacts monetary policy. In other words, the Fed is the “transmission mechanism” between US economic reports and market prices, so any discussion about NFP should start with a look at the state of the US central bank.

When it comes to the Fed, monetary policy is in flux: based on last month’s statement and economic projections, many central bankers wanted to pause rate cuts and see how the economy performed before deciding what to do next. The only problem? The economic data has taken a big turn for the worse in recent days.

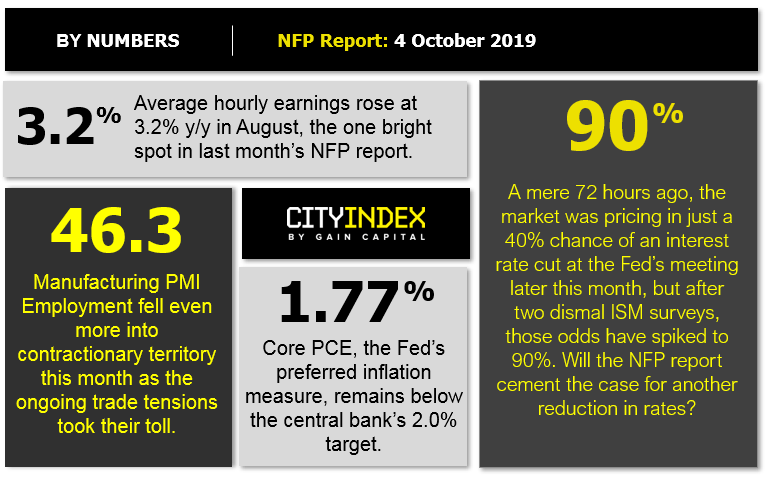

A mere 72 hours ago, traders were pricing in just a 40% chance of an interest rate cut at the end of this month, according to the CME’s FedWatch tool. After back-to-back abysmal ISM surveys though, those odds have surged to 90%! In that light, another weak NFP report may be the proverbial “nail in the coffin” that cements a rate cut later this month, whereas a better-than-anticipated report could open the door a crack for the Fed to hold rates steady.

NFP Forecast

Unfortunately for bulls, the leading indicators for Non-Farm Payrolls are pointing to another soft reading on the US labor market:

- The ADP Employment report dropped to 135k, below estimates of 140k and down from last month’s downwardly-revised 157k print.

- The ISM Manufacturing Survey employment component fell to 46.3 down from last month’s already contractionary 47.4 reading.

- The ISM Non-Manufacturing Survey employment component fell to 50.4, showing essentially no net growth in service sector employment after a 53.1 reading last month.

- The 4-week moving average of initial unemployment claims ticked back down to 212,500 from last month’s 216,250 average.

Overall these leading indicators point to another weak report, with potential for a reading below 100k. That said, the historically low initial unemployment claims figures do provide a (small) reason for optimism among bulls, as does the potential for a recovery after last month’s disappointing reading. Regardless, the month-to-month fluctuations in this report are notoriously difficult to predict, so we wouldn’t put too much stock into any forecasts (including ours). Most importantly, readers should note that the unemployment rate and (especially) the wages component of the report will also influence how traders interpret the strength of the reading.

Source: TradingView, City Index

Potential Market Reaction

See wage and job creation scenarios, along with the potential bias for the USD dollar below:

|

Earnings < 0.2% m/m |

Earnings = 0.3% m/m |

Earnings < 0.4% m/m |

|

|

< 100k jobs |

Strongly Bearish USD |

Bearish USD |

Neutral USD |

|

100k-150k jobs |

Bearish USD |

Slightly Bearish USD |

Slightly Bullish USD |

|

> 150k jobs |

Slightly Bearish USD |

Neutral USD |

Bullish USD |

In the event the jobs and the wage data beat expectations, then we would favor looking for short-term bearish setups in EUR/USD, which remains in a strong medium-term downtrend and has seen a small counter-trend bounce so far this week. But if the jobs data misses expectations, then we would favor looking for bearish setups on the dollar against the yen, given this week’s breakdown below support and potential for safe haven demand for the yen.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM