NFP misses the mark but US job growth still robust

The Non-Farm payrolls report for July was slightly disappointing, payrolls came in at 215k vs. 225k expected, and the June figure was revised up to […]

The Non-Farm payrolls report for July was slightly disappointing, payrolls came in at 215k vs. 225k expected, and the June figure was revised up to […]

The Non-Farm payrolls report for July was slightly disappointing, payrolls came in at 215k vs. 225k expected, and the June figure was revised up to 231k vs. 223k initially. The unemployment rate was steady at 5.3%, still the lowest level for 7 years, while wage data missed the mark, with annual earnings coming in at 2.1% for last month, lower than the 2.3% expected, but still positive when adjusted for inflation.

Even though the headline figure was weaker than expected, the US is still managing to create over 200k jobs per month, which is a decent figure and one that does not preclude a Federal Reserve rate hike in the coming months.

The US jobs market remains in good shape

Digging a bit deeper into the numbers you can see that the US jobs market remains in rude health. The largest creators of jobs included the healthcare and food and drink sectors, however, professional and technical services also created 27k jobs last month, which is positive for the US economy as jobs in this sector – including architects, engineers and software developers – tend to be high paying and full time, rather than part time roles. The Bureau of Labour Statistics also pointed out that productivity rose in 30 out of 49 industries in 2014, which bodes well for productivity in 2015, which is important if inflation and wages are to rise down the line. Weekly hours’ worked also edged up to 34.6 hours per week last month, which is the highest level since February and bucks the usual trend in the summer months of working hours being scaled back slightly.

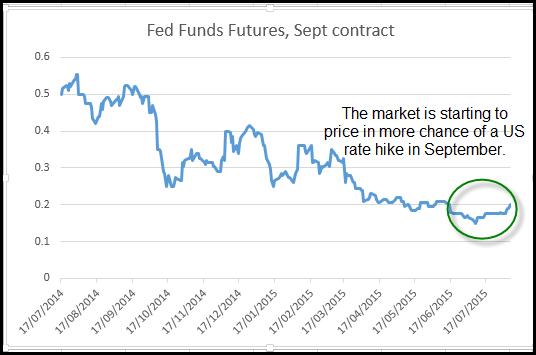

A Fed rate hike in Sept still on the cards

So, even if payrolls were not as strong as expected for last month, the US economy still looks like it could withstand a rate hike from the Federal Reserve in the coming weeks, and we still think the Fed will seriously consider hiking rates next month. In the aftermath of the report, the yield on the September Fed Funds Futures contract crept higher, and is now pricing in 20 basis points of hikes, only 5 bps short of a rate hike (see figure 1). This is up 3 basis points on the week, which may not seem like much, but is a serious adjustment to the short-term Fed Funds Futures market, which could help to reignite the dollar rally.

The impact on FX:

The dollar index jumped above 98.00 in the aftermath of this report, however, without a major surprise from the data and with thin volumes, this pair faltered at 98.35 – a key short term resistance level that also halted the bull-run on the dollar on July 17th.

We need to get above this level for the 100.00 highs from March and April to come back into focus. It was a volatile day for EURUSD, which dipped below 1.0860 at one stage this afternoon before clawing back losses and closing the London session around 1.0950. The ease with which this weaker than expected US data weighed on the EUR makes us think that a more serious decline could be in store for EURUSD in the coming weeks. So far the base of the range has been 1.0850, if we close below this level in the coming weeks then we could see a sharper decline back to the March/ April lows at 1.05.

Figure 1:

Source: City Index