December 6, 2019 10:16 AM

NFP Blows Away Expectations, however Unlikely to Affect Fed Decision Next Week

Nonfarm Payrolls for November released today were 266K vs 183K expectations. In addition, October’s NFP were revised higher from 128K to 156K! Although these numbers include the return of the GM strikers, those workers were already baked in to the expectations. Average Hourly earnings was 0.2% vs 0.3% expectations, slightly worse than expectations. The Unemployment Rate was better than expected, falling to 3.5% from an expectation of 3.6%.

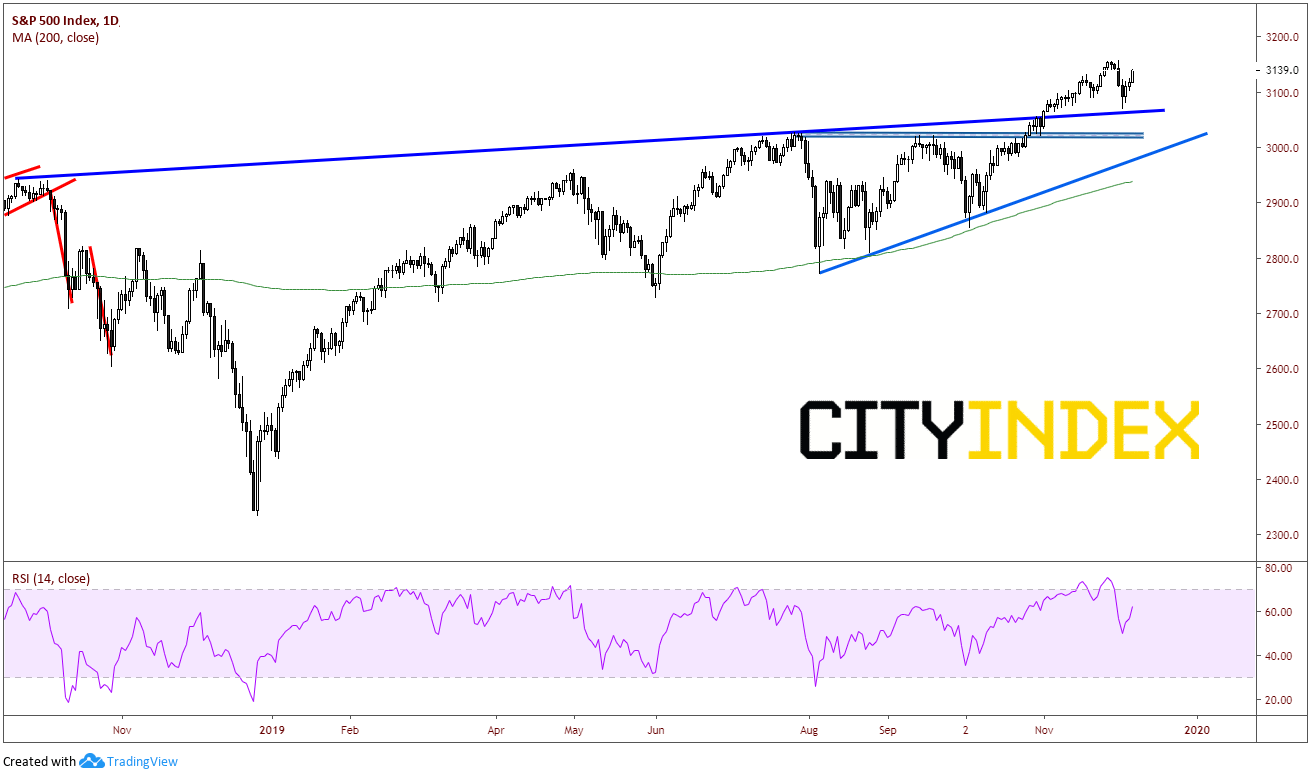

The S&P 500 is up over 20 handles after the release of the data. The major index managed to hold the trendline support dating back to September 2018.

Source: Tradingview, City Index

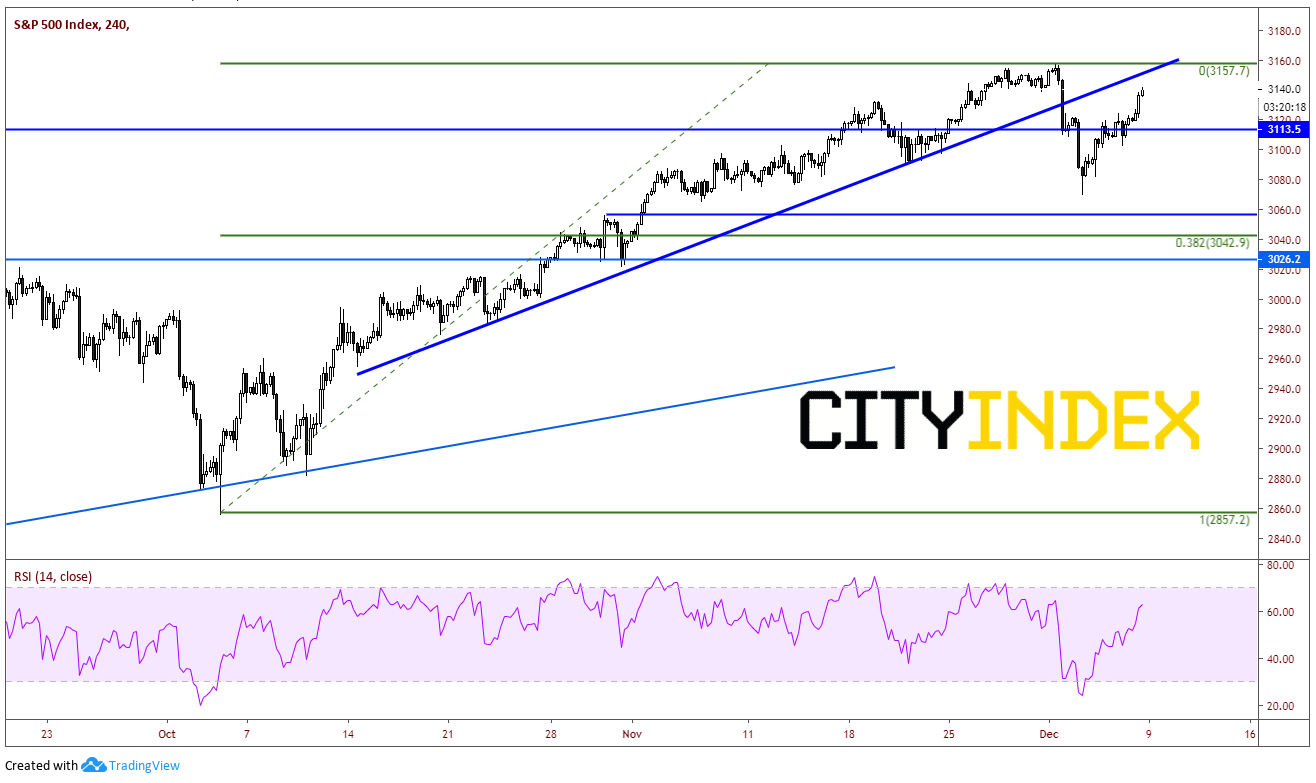

It appears that the index is testing the underside of the upward sloping trendline from mid-October near 3150. Above that, all-time highs in the S&P 500 cash index are 3157.6 from Monday.

Source: Tradingview, City Index

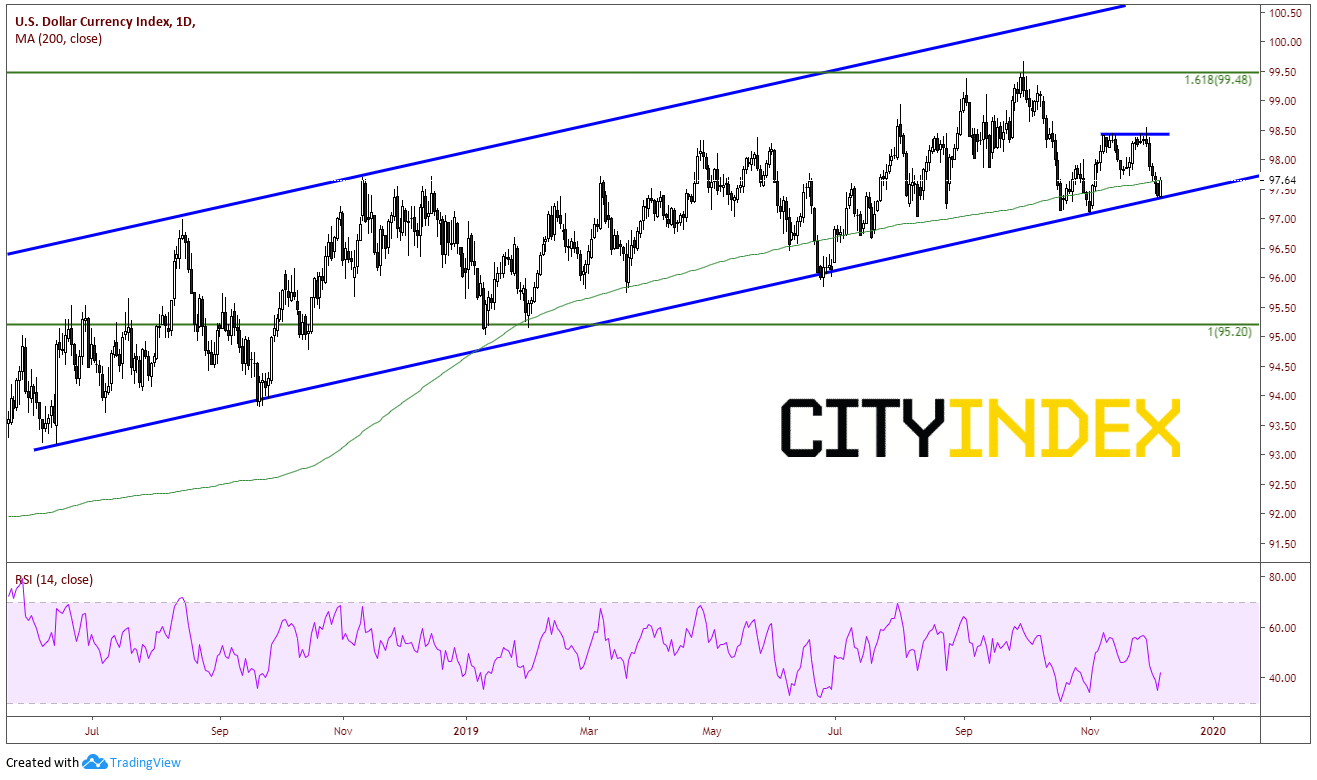

The US Dollar Index took off as well after the data. On a daily chart, DXY is currently putting in a bullish candle which is testing the 200 Day Moving Average. Price held the upward sloping trendline dating back to May of 2018, which continues to act as daily support.

Source: Tradingview, City Index

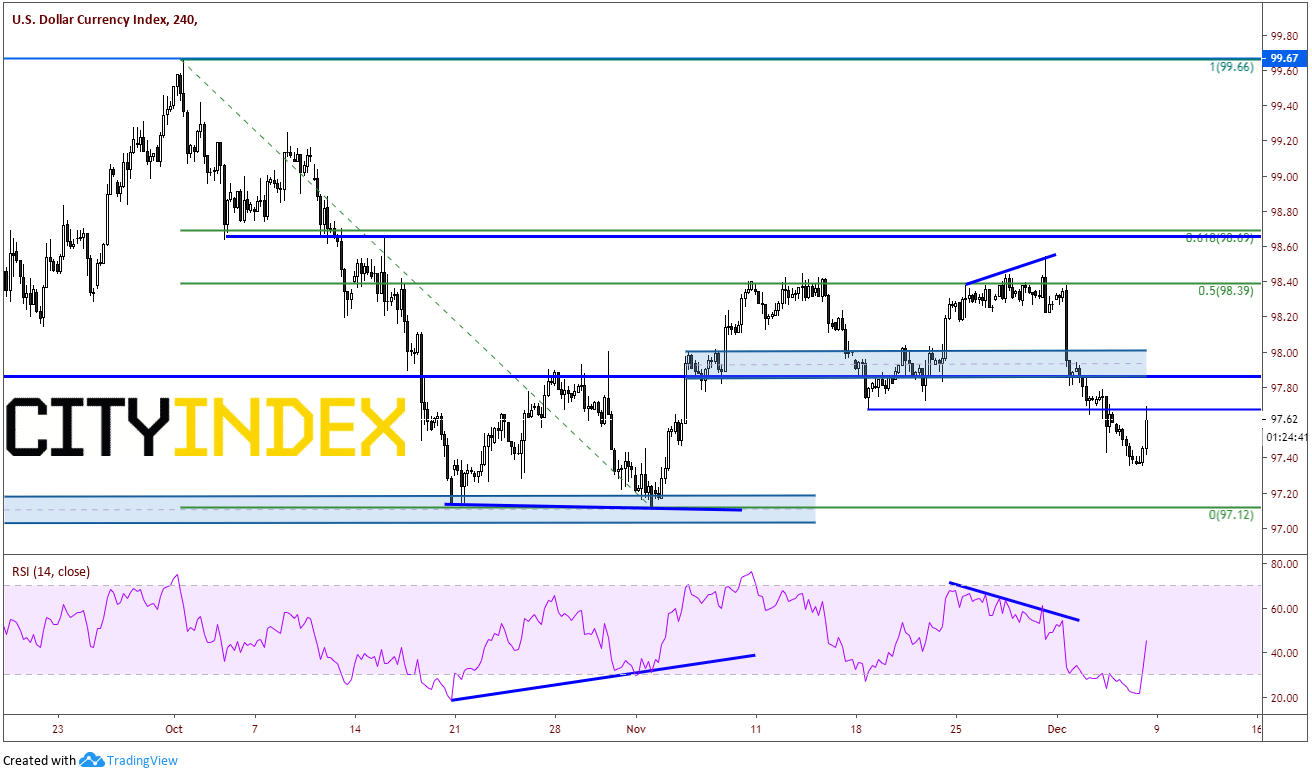

On a 240-minute chart, price is currently testing horizontal resistance at 97.68. There is also a band of resistance just above between 97.85 and 98.00.

Source: Tradingview, City Index

As good as today’s NFP data is, it is unlikely to affect the FOMC’s rate decision next week. According to the CME FedWatch Tool, there is almost a 100% chance that the Fed will remain on hold. Markets will closely watch the Summary of Economic Projects that will be released with statement to see how this data will affect the Committee’s outlook.

Also, there are a number of other pressing matters the markets are watching at the moment, such as the US-China trade deal, Brexit, and the USMCA. Headline risk will be watched carefully heading into the end of the year. The euphoria from today’s data can be reversed with negative headlines.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM