Next share price relief rally faces a trim

Next Plc. shareholders are showing relief on Thursday after the group kept track with profit and outlook revisions it announced in January.

Next Plc. shareholders are showing relief on Thursday after the group kept track with profit and outlook revisions it announced in January.

We query whether Next shares can ‘save the year’—it is the worst FTSE 100 performer so far in 2017, having been among the worst in 2016.

Next is the latest major British retailer to sound alarm bells about the consumer outlook, though there’s clearly a lot about that outlook that is Next-specific. Saying it is “extremely cautious” is a signal that it has identified weak fronts on which it is relatively undefended, beyond the “Three potential threats” to the clothing sector it highlights. We link comments noting a “shift away from spending on clothing, price inflation as a result of sterling’s devaluation and potentially weaker growth in real incomes” to its disclosure elsewhere that the drive to modernise logistical, purchasing and manufacturing methods is taking longer than it would prefer. Reduction of new product purchasing cycle to as little as three months “from concept to shop floor”, after all, is slower than the norm at ‘fast fashion’ retailers, mostly online, which are eating Next’s lunch.

We would expect comparable competitors on a typical large city centre high street to include Primark, M&S, Moss Bros., Top Shop, and perhaps TK Max and Superdry. It would be a surprise if most had a three-month decision-to-shop-floor purchasing cycle; though to be fair, Next’s own-brand mix obviously differs from most. Either way, whilst Next suggests it is widening the reach of clothing segments in which it can move fast, success will only reap modest top-line improvements.

Next also admits it has been distracted from attention on the “best-selling, heartland product from our ranges”. It is taking “corrective action”, having identified the issue in January. We applaud the relative speed with which the retailer captured the issue and candidness in disclosing it, but the revelation illustrates that challenges of operating at speed in its market as consumer habits evolve can wrong-foot even the most experienced players. Challenges will be compounded by the year’s softening consumption environment.

We moderate our views given that Next has probably calibrated guidance slightly lower than it expects to achieve. Notwithstanding margin erosion from start-up costs, wage inflation, and weak total sales vs. fixed costs, the net operating margin looks capable of reclaiming some 100 basis points in 2017. That would leave it close to the mid-point between 2015/16 and 2016/17 (15.8%).

The wide leeway demanded by a 300 basis point range in full-priced sales guidance and £100m for pre-tax profit makes those outcomes more difficult to project this early, though we suspect that a failure by Next to at least hit the lower end of the profit range—£680, almost identical to 2014—would surprise the industry.

Thursday’s share price reaction is also linked to Next’s pledge to generate more cash than capex and dividend commitments require. As we have suggest above however, Next’s biggest challenges this year hinge more on speed of competitive modernisation (perhaps innovation) than on its ability to finance battles on the high street and keep shareholders sweet.

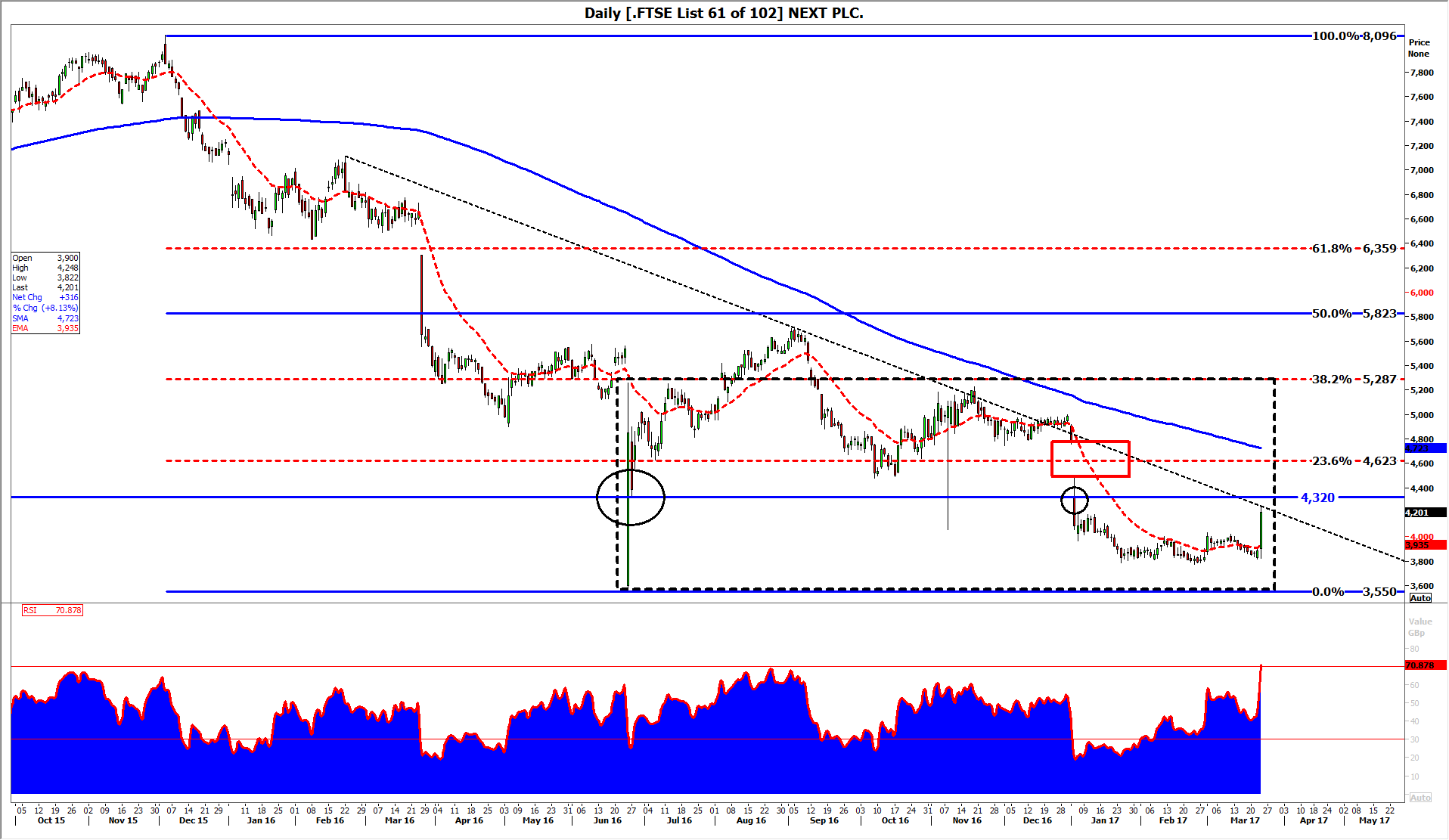

Source: Thomson Reuters, City Index / please click image to enlarge