Next Plc shares out of fashion despite good earnings

Shares of high street fashion retailer Next Plc. have slumped to near the bottom of the UK FTSE 100 stock index today despite the firm […]

Shares of high street fashion retailer Next Plc. have slumped to near the bottom of the UK FTSE 100 stock index today despite the firm […]

Shares of high street fashion retailer Next Plc. have slumped to near the bottom of the UK FTSE 100 stock index today despite the firm reporting a 19% increase in first-half profits.

With the stock having reached its highest-ever level over the last few days, it appears traders have opted to take profits; they may also be influenced by market views suggesting revenue momentum could be slowing.

Britain’s second-biggest clothing retailer by sales value reported a 19.3% rise in first-half profit, with stores and home shopping businesses both showing growth.

Next said pre-tax profits were £324.2m in the six months to July, compared to £271.8m in the same period last year.

The group admitted some of its strong performance might be attributable to factors it cannot claim credit for, for instance, the improving economy, low interest rates and availability of credit.

It suggested if any of these became less favourable in the years ahead, there could be an impact on its earnings.

Despite the cautions, Next is keeping guidance it issued in July, when it upgraded expectations for full-year revenue for the second time in one quarter, expecting sales to increase by 7%-to-10% and pre-tax profit to rise by 11%-to-17% to between £775m-to-£815m.

Next has also broken down forecasts into quarterly periods, with 10% growth expected for the third quarter and 4% foreseen for the fourth, with the slippage likely to be due to the tougher comparable basis seen in the later quarter, according to Next.

On a more qualitative basis, Next is perceived to be outperforming rivals, like Marks & Spencer because of its strong online offering, its steady rate of new store openings (reaching 500 in the UK and Ireland and 200 abroad) plus diversification into new product areas, like home wares.

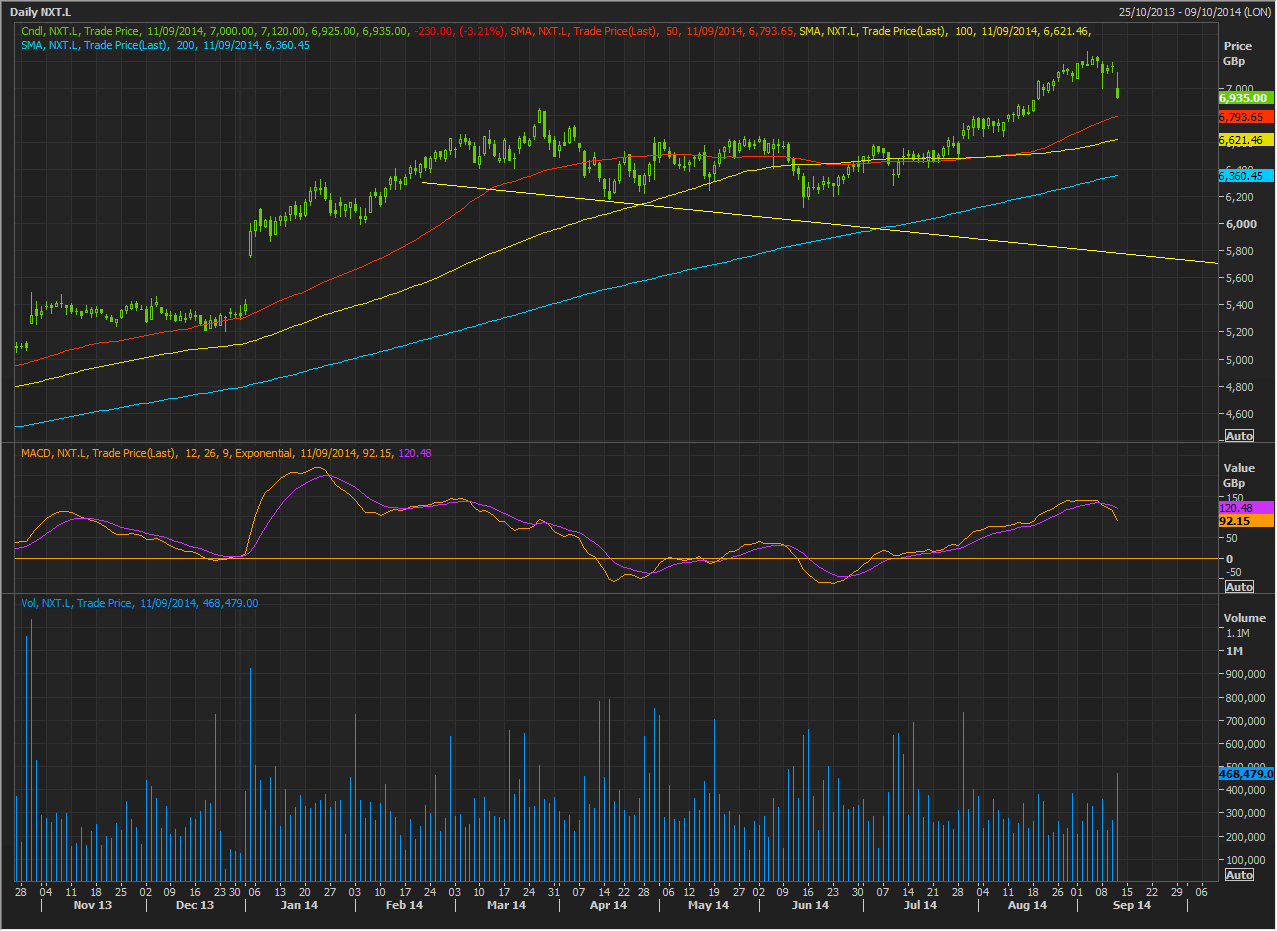

So, the current stock loss of 3.2% at 6940p seems out of kilter with Next’s earnings today and the conditions in the underlying business.

The 39% gain in the year to date, excluding today’s trading, may go some way to accounting for a perceived need by investors to reduce. That and the stock having reached 7180p on 3rd September, an all-time high made all the more pointed because the stock price was reduced in September 2002 by the effect of a stock split.

The stock’s chart reflects these misgivings quite well; note the bearish hammer forming from today’s trading performance.

Should the price fall through the moving averages in the near term—something which at present seems unlikely—support may be seen close to the falling line trend line. At current rates of decline, this might suggest a resumption of the uptrend at a price no lower than 5786p.