Next Plc expects shabbier sales this year than last

Next Plc.’s 12.5% uplift in full-year profit ought to have enabled it to put the shabby performance that marred its business in the second half […]

Next Plc.’s 12.5% uplift in full-year profit ought to have enabled it to put the shabby performance that marred its business in the second half […]

Next Plc.’s 12.5% uplift in full-year profit ought to have enabled it to put the shabby performance that marred its business in the second half of last year behind it.

But the stock has been weak all day, having traded more than 5% lower at one point, wiping out its entire 3-week advance.

That’s despite

Next effectively admitted this morning it still hasn’t managed to re-ignite the sales growth rate it enjoyed in the years prior to the financial crisis, and comments from its CEO do not suggest those hey days will return this year.

Investors nevertheless gave Next the benefit of the doubt since 2008/09, with the share rise since then pushing 900%.

Expectations of a moderate 6% extension of £4bn total annual sales announced this morning have been disappointed.

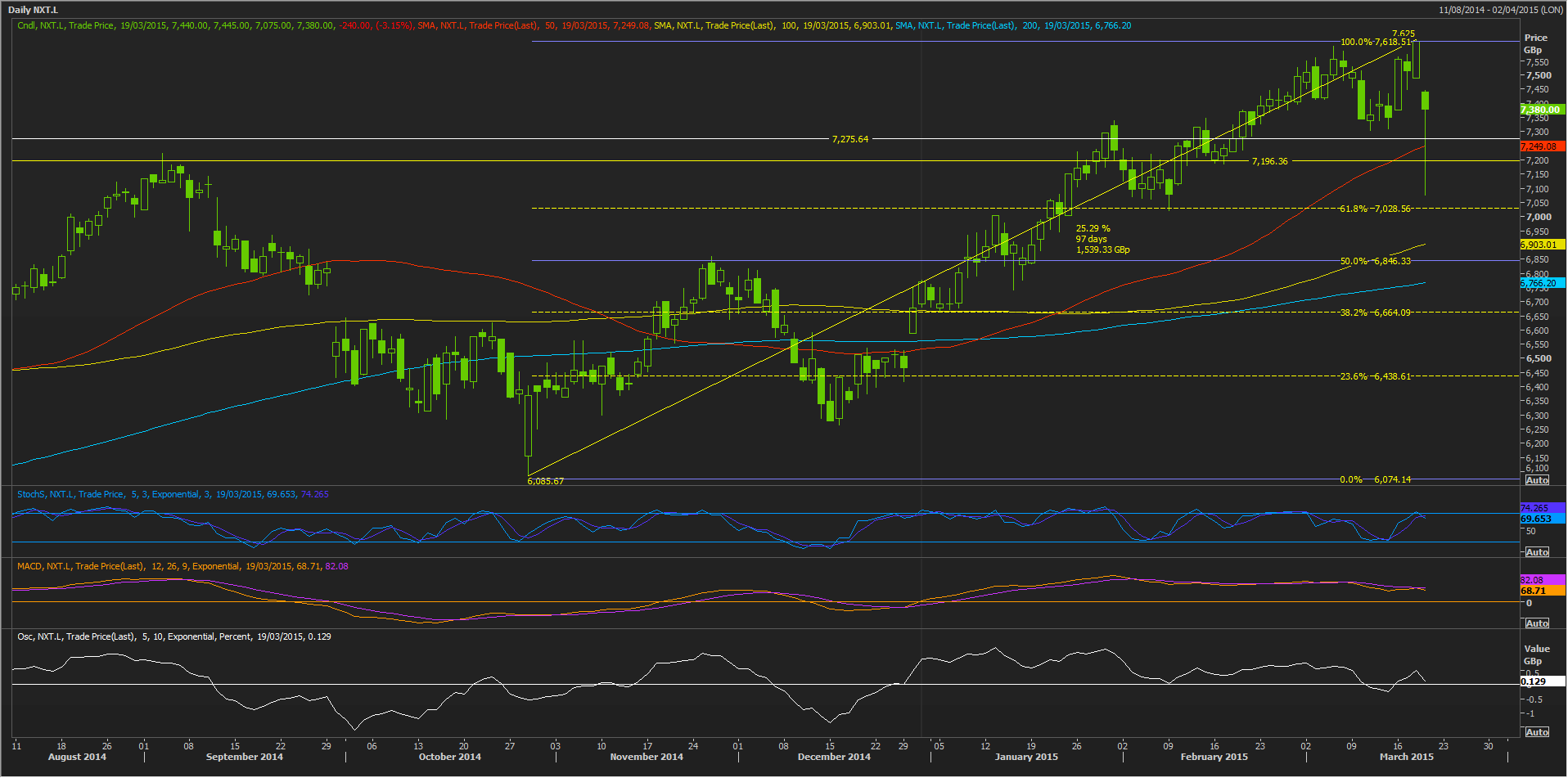

The stock was caught up in yesterday’s post-Budget rally, and rose to a new record high of 7625p, extending its comeback from lows marked in October to 25%.

But on a neutral assessment, that the UK’s largest clothing retailer signaling an inability to provide a more specific forecast for the first part of the year beyond saying that sales would rise between 0%-to-3%, and second half sales by 3.5% to 7.5%, is a problem for investors.

Next itself accepted that in any case, these rates, and the 25% forecast rise for sales at online/catalogue platform Next Directory, were “significantly lower than last year”.

The UK’s largest clothing retailer warned elsewhere in the full-year report that whilst the UK economy looks benign, some of its collections are not as strong as they were at the same point last year.

It also suggested that it faces a tough hurdle from its comparable revenue performance last year when sales had been boosted by unusually warm weather.

Aside from this, whilst the firm which trades from over 500 stores in Britain and Ireland and almost 200 stores overseas guided towards a ‘clean’ pre-tax profit of £765m-to-£785m in December, it has only managed on an underlying basis, £782m.

On a clean basis, which is with all obfuscating impairments and one-off costs stripped out, Next’s pre-tax profit for the year was £773m.

Not a massive ‘miss’ of the top end of guidance, but in the context of guidance from the firm that has a garnered a reputation for being quite conservative, Next is perhaps being marked-down more harshly than it would have been.

There may also be some room for head-scratching in the light of Next CEO’s comments that the 2014-15 year was exceptional in that the firm’s buyers had got “pretty much every range right”.

This might be a fair assessment, though perhaps a generous one given Next’s end-September trading statement indicated limited visibility into the rest of the year.

It said at the time that unusually warm weather lifted sales in August and unusually cold weather damped sales in September.

“This year (2015) is a more normal year, we don’t think we’ve got everything right,” Simon Wolfson added, during a media interview this morning.

He went on to question the general strength of consumer sentiment in the UK, where Next made 94% of its revenues in 2014.

There was little evidence consumers were spending any increases in disposable income on clothing, Wolfson said.

“It doesn’t seem to be coming into clothing but we’ll need to see everybody else’s results before we know that for sure”.

That sounded admirably candid.

But investors will need to square the CEO’s pessimistic view of the consumer outlook with a trailing and forward price/earnings ratio of 18.6x and 17.4x respectively, a considerable lead against the rating oif its comparable UK peer Marks & Spencer, at 14.6x prospectively.

Whilst Next alluded in today’s report to exceptional shareholder pay-outs, saying it assumed £360m “generated and returned as special dividends rather than buybacks”, its yield without these for the year would remain close to the industry average 2%.

(The projected yield for the year could equate to 5.4%. Going by Next’s comments, such a rate should not be counted on for 2015).

Still, investors holding since the end of October booked 25% up to last night’s close.

At the same time, the stock’s average 7-year compounded growth was about 40% per annum, up to last night’s close.

And sections of the market are still expressing reasonable support at 7275p today.

That is well above a helpful 61.8% retracement marker from yesterday’s peak back to that late October low.

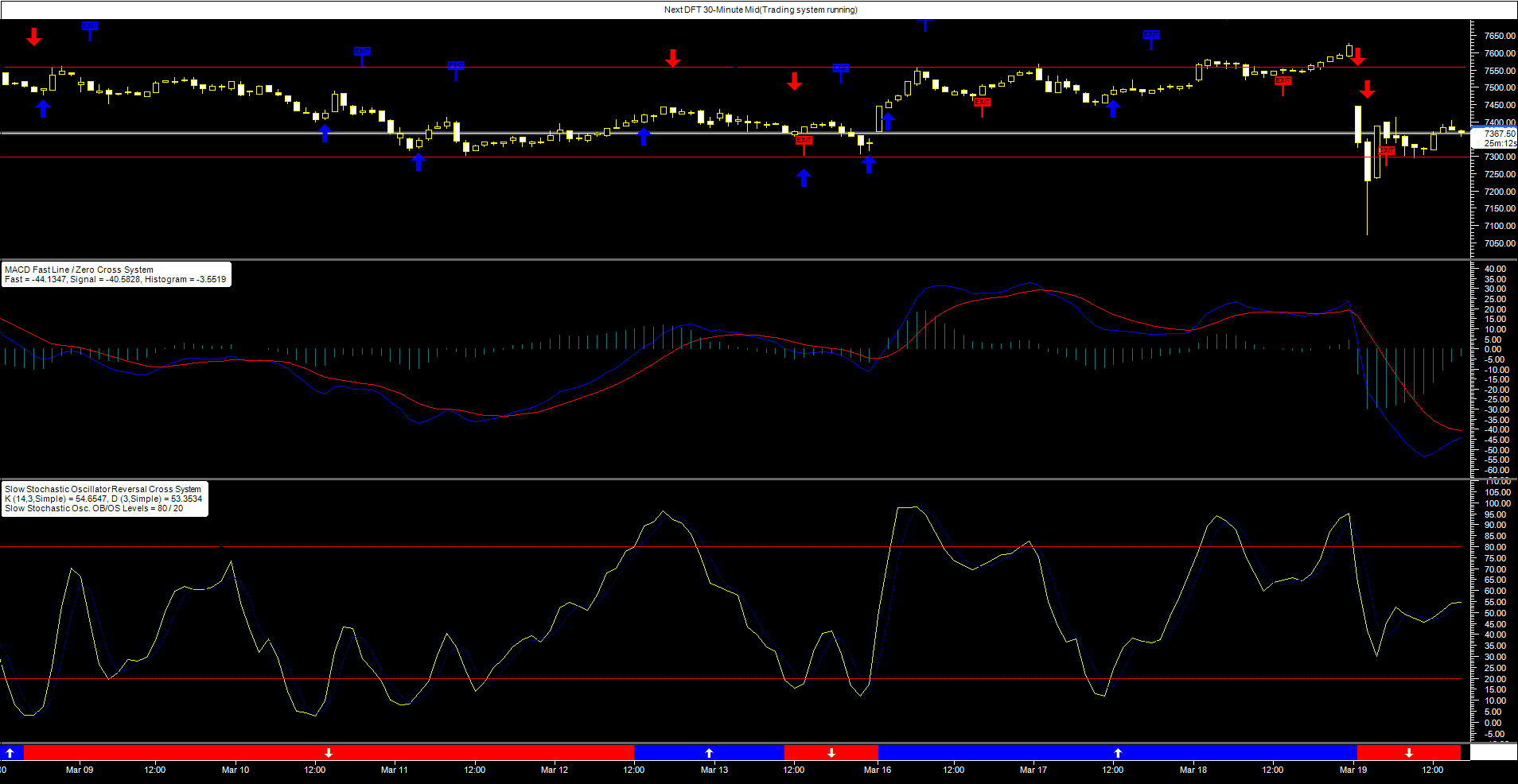

In keeping with this underlying technical underpinning, traders of City Index’s Next Daily Funded Trade today have already bid the title back into its band of support seen this month starting around 7300 and topping out around 7558p, amid firm momentum.