Next beats Brexit Blues for now

This is not how the ‘picky consumer’ story is ‘meant’ to go. After Next Plc. beat the warning drum again on Wednesday about possibly “the […]

This is not how the ‘picky consumer’ story is ‘meant’ to go. After Next Plc. beat the warning drum again on Wednesday about possibly “the […]

After Next Plc. beat the warning drum again on Wednesday about possibly “the toughest” year since 2008 (to quote from the retailer’s March statement) its stock rose to the top of the FTSE 100.

For the 3rd time in five months, Britain’s biggest clothing retailer slashed forecasts, now warning that full-price 2016/17 sales could be somewhere between 3.5% lower to 3.5% higher compared with up or down 1% year-on-year.

The downgrade makes sense given current trading. Those much-prized full-priced sales fell 0.9% in the first quarter against the same period a year earlier, towards the bottom of previous guidance. And Next even threw in its near-customary (or infamous depending on your point of view) weather complaint. (This time, “Much colder weather in March and April reduced demand for clothing”.)

Investors seemed bothered by all the above early in the session—the shares fell almost 80p to begin with, but then went on to add well over 6% at their best.

Languishing at the bottom of the list of the FTSE’s worst performers of the year so far will do that for a stock. (Next was still 31% lower YTD at last check, 5%-7% worse than No.99, RBS and No.98, Barclays.)

Next CEO Lord Wolfson, a ‘sitting peer’, but a peerless fit for the term ‘City grandee’, has certainly not been backward about potential reasons. Among other portentous notes he sounded in March, Wolfson also pointed out that growth in real UK earnings had slowed sharply over 6 months, while growth in output across services, manufacturing and construction all decelerated throughout 2015.

But, the Conservative Member of the House of Lords has studiously avoided pinning the blame for consumer tardiness on a steady stream of signs pointing to economic uncertainty over the June vote on EU membership.

“I don’t think anybody consciously says ‘look I’m not going to buy that dress’ because we might leave the EU’. My instinct is it’s not affecting consumer sentiment”, Wolfson said in March. True, UK retail sales posted their 35th straight month of year-on-year growth that month. But unemployment rising for the first time in 7 months in April, and the economy turning in an even more anaemic 0.4% growth in Q1 than 0.6% in Q4, at the very least can’t be ignored, in assessing consumer confidence.

Lord Wolfson does of course support ‘Brexit’ in a personal capacity, though (emphatically) not as CEO of Next.

The distinct punishment investors have meted out to Next shares would have to be something akin to a coincidence, in that case.

Even though Next had fallen far further in the year-to-date than the next comparable FTSE 100 retailer, Marks & Spencer, which was down 7.2% for the year at last check.

The UK’s No.2 clothing seller—which has failed to grow those sales for 20 near-consecutive quarters—is of course just as exposed to sterling revenues, as Next.

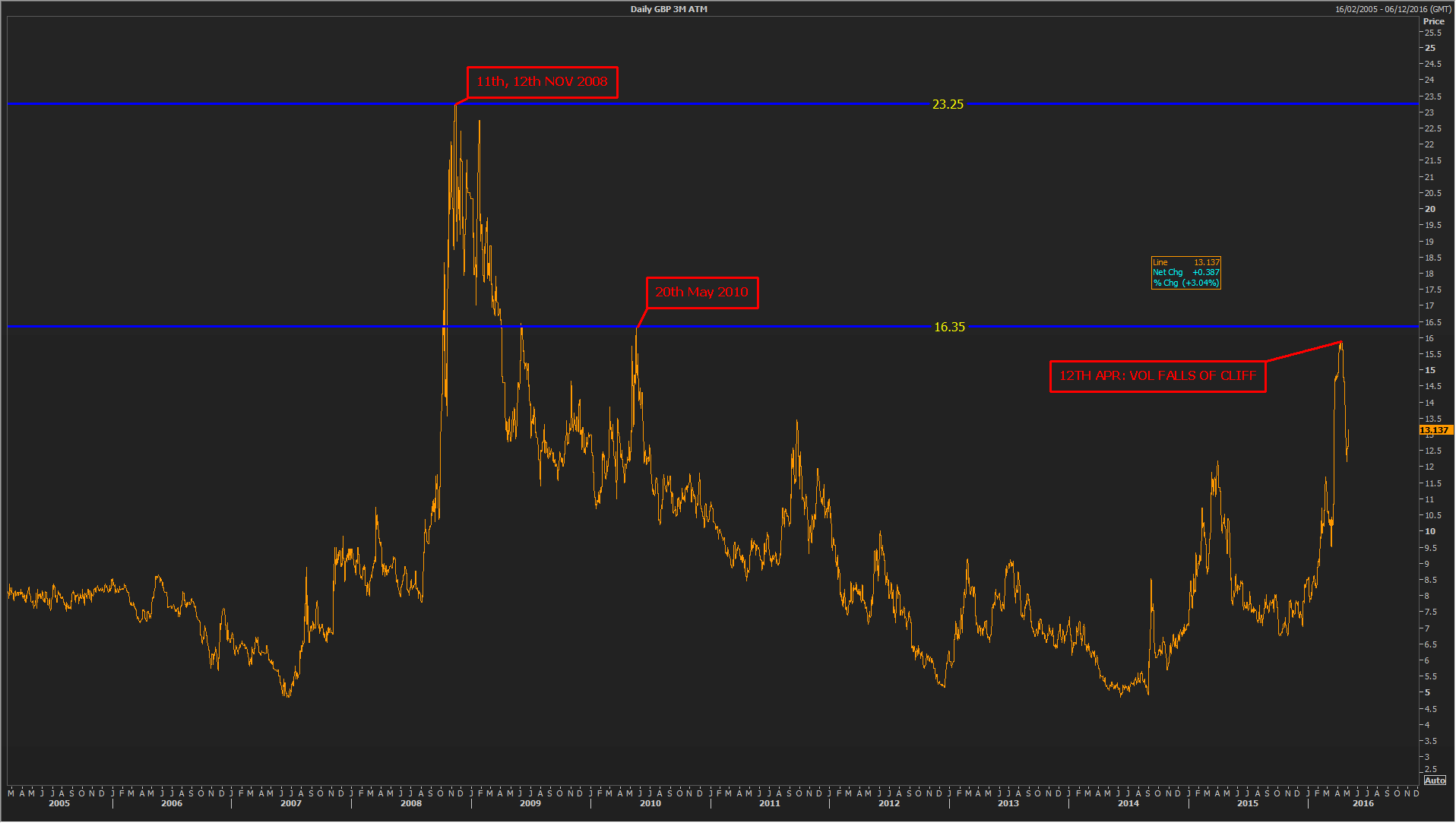

Either way, after a few weeks of calm, sterling options traders retooled on Wednesday.

A key gauge of volatility (see below) saw its biggest jump since the trade went off the boil last month.

Source: Thomson Reuters, City Index

Vol. is still way off the mid-April highs that coincided with enhanced market jitters over a Brexit.

But if it’s anything like a barometer, sensitive shares, like banks and retailers, including Next, might soon lag the market even further.