A dose of reality from Federal Reserve Chair Jerome Powell overnight has brought stocks crashing lower. Wall Street closed in the red, with losses spilling over into Asia, and Europe is unsurprisingly looking to open on the back foot, adding to yesterday’s losses.

Doom and gloom, Jerome Powell spoke of an extended period of weak growth, pouring cold water over the V-shaped recovery fantasy that had been spurring the markets higher. Fears of a second wave of the virus are lingering stubbornly as economies reopen and clusters of new outbreaks are appearing. Adding to traders’ angst were comments from the WHO, that coronavirus may never disappear.

This will be a rocky road to recovery. Whilst it is unlikely that we will return to March lows, there will be fundamental changes to many industries which simply mean that they wont be able to return to pre-virus level output with social distancing measures are in place.

Risk off boosts gold

The rise of risk aversion and the adoption of a risk off strategy is boosting gold this week. The traditional safe haven is back in demand as dark clouds gather on the horizon and the economic recovery starts to look distant. The precious metal is on the rise for the third straight session, trading at a two-week high.

The rise of risk aversion and the adoption of a risk off strategy is boosting gold this week. The traditional safe haven is back in demand as dark clouds gather on the horizon and the economic recovery starts to look distant. The precious metal is on the rise for the third straight session, trading at a two-week high.

Oil recoups some losses

Oil is on the rise, recouping some of the losses from the previous session. Despite an encouraging EIA report which revealed that US stockpiles unexpectedly dropped by 745,000 vs exp. 3.8 million barrels oil still ended the day -1.9% lower. This was the first decline in oil inventories since January, making it a significant sign that energy consumption is on the rise.

Oil is on the rise, recouping some of the losses from the previous session. Despite an encouraging EIA report which revealed that US stockpiles unexpectedly dropped by 745,000 vs exp. 3.8 million barrels oil still ended the day -1.9% lower. This was the first decline in oil inventories since January, making it a significant sign that energy consumption is on the rise.

Initial jobless claims in focus

Initial jobless claims will be under the spotlight layer today. Claims have fast become one of the most closely monitored data points given its timely insight into the US economy’s health as coronavirus batters the US labour market.

Initial jobless claims will be under the spotlight layer today. Claims have fast become one of the most closely monitored data points given its timely insight into the US economy’s health as coronavirus batters the US labour market.

20.5 million jobs were lost in April, the steepest decline since the Great Depression. 2.5 million more Americans are expected to have filled for unemployment benefit in the week ending 9th May. Whilst this is an extremely high number, it is coming down from 3.16 million the previous week and claims have been declining since the record of 6.86 million on March 28th. 36 million have filled for claims since March 21st. April is expected to the bottom, however with so many Americans out of work, any recovery will be a long drawn out process.

FTSE levels to watch:

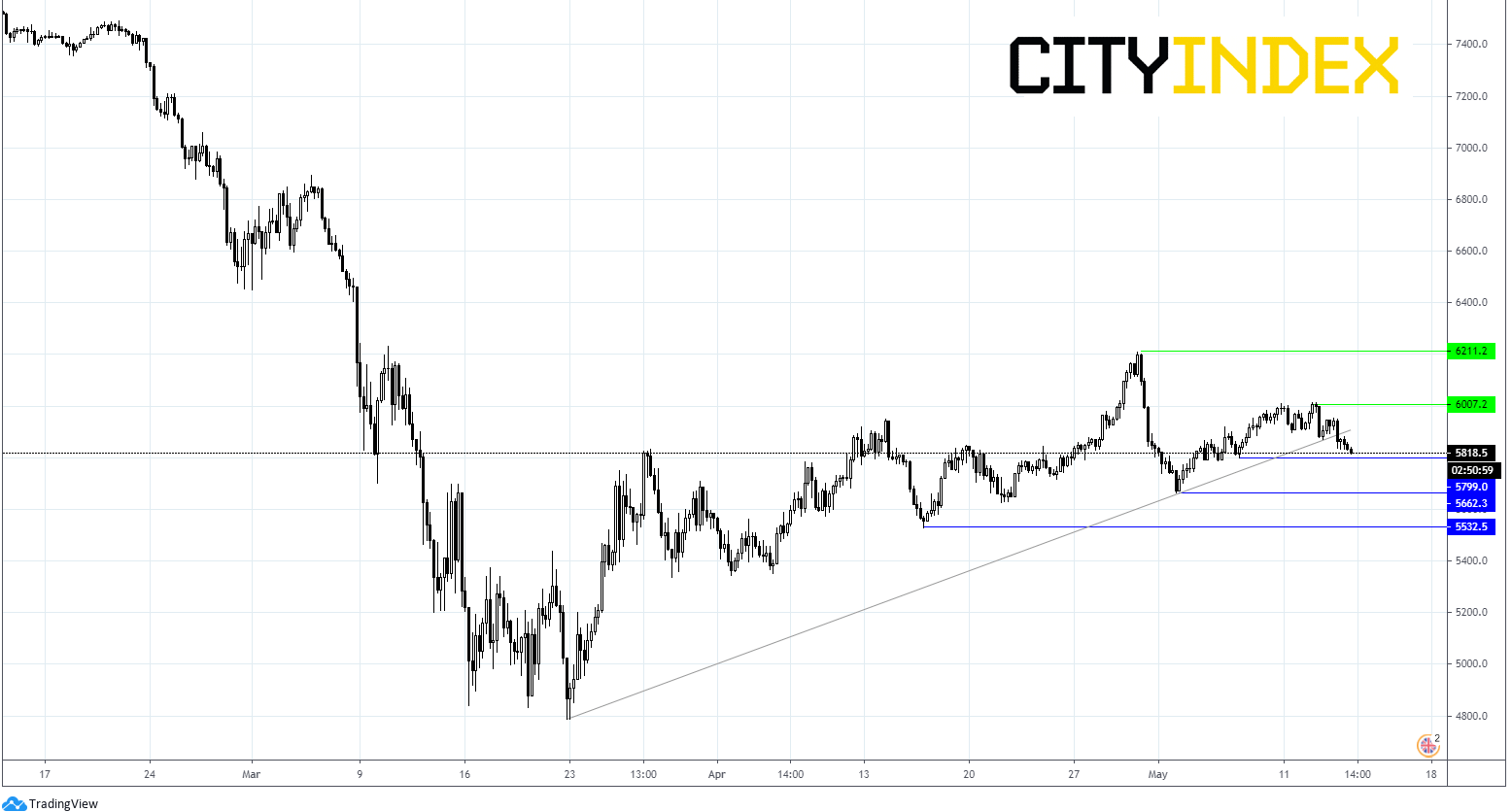

The FTSE closed -1.5% lower yesterday and is looking at another step lower today. The index slipped through its ascending trend line support.

Immediate support can be seen at 5800 (low 6th May) prior to 5660 (low 3rd May) and 5530 (low 15th April).

Immediate resistance is at 5900 (trendline support turned resistance) prior to 6000 (psychological level)

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM