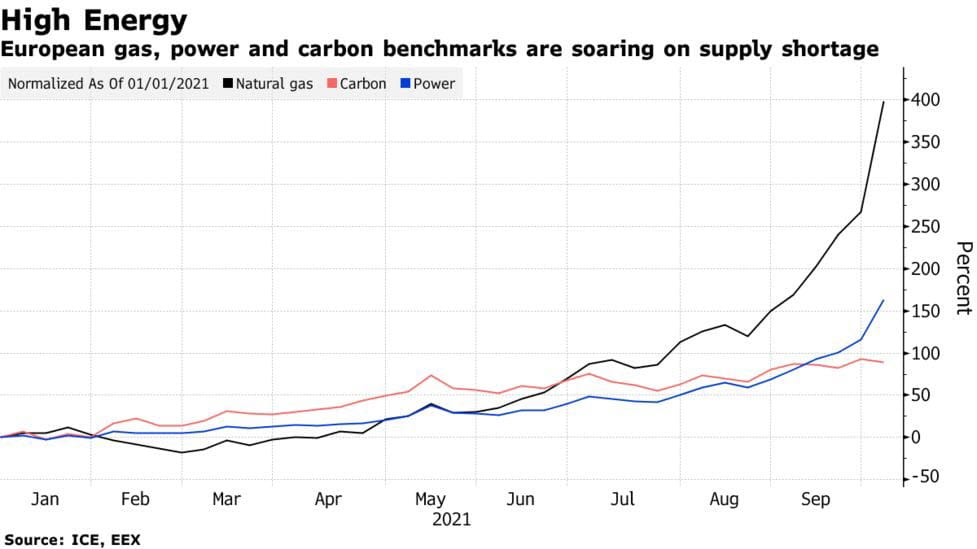

For those across Europe (and much of the world), the economic and market story to watch is the energy crisis. After edging higher throughout the summer, energy prices on the continent have exploded higher over the last 10 weeks in particular, with Natural Gas prices in particular nearly quadrupling over the last six months:

Source: Bloomberg

As my colleague Tony Sycamore explained last week, the shortages in the UK specifically are due to a confluence of factors including panic buying after BP’s warning that it would “temporarily” close petrol stations, a Brexit-driven shortage of drivers, and supply chain disruptions. Regardless of the initial catalyst, fears of a shortage have become a self-fulfilling prophecy, with individuals and firms accelerating purchases to buy any supply they can ahead of continued price increases.

With stakeholders hoarding natural gas in the brick-and-mortar world, we’ve also see a surge in trading activity in Natural Gas across our StoneX retail platforms as traders look to capitalize on the volatility. Total trading volume in natural gas products rose 82% in August, then more than tripled in September, and so far early in October, natural gas volumes are tracking toward another 20%+ rise on top of September’s lofty total.

Today brought a modicum of good news for energy-strapped European nations: Russia has offered to increase natural gas exports to the continent, potentially to record highs, on its recently completed Nord Stream 2 pipeline. These headlines have, at least temporarily, broken the proverbial fever for natural gas prices, with prices on falling nearly 8% on the day to below $6.00/MMBtu.

So does this mark the moment of “peak panic” for the natural gas market?

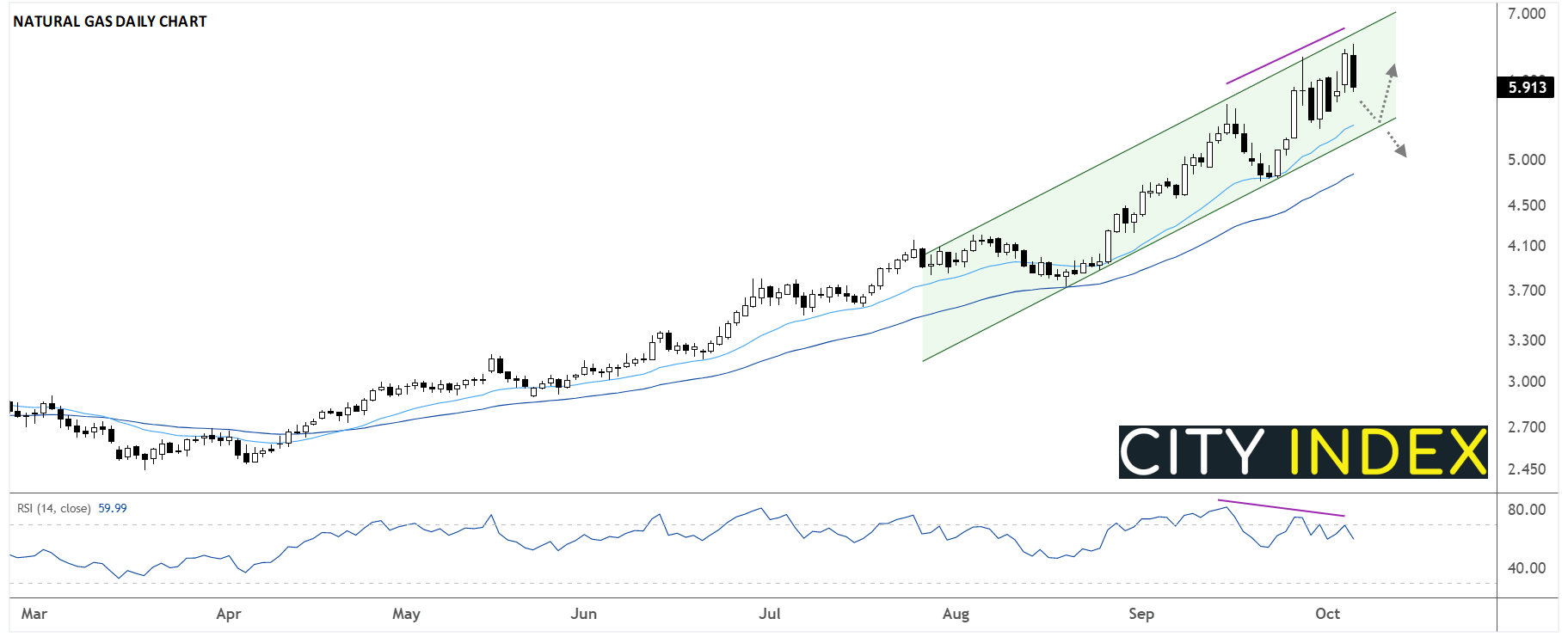

While it’s certainly possible, the fundamental issues across the energy markets are complicated, and there are no quick fixes for them. As the chart below shows, the price of natural gas is still holding above both its shorter-term 21-day EMA and its medium-term 50-day EMA, with prices still comfortably in the middle of the recent bullish channel, so the path of least resistance from a technical perspective is still to the topside for natural gas:

Source: TradingView, StoneX

At this point, traders would need to see a break below at least the 21-day EMA and bullish channel in the low $5.00s to erase the near-term bullish bias. Until then, Russia’s “white knight” offer notwithstanding, fears of rising prices may remain the dominant theme in the natural gas markets.

For those who aren’t able to trade natural gas directly in their region, the commodity tends to have a strong correlation with the USD/RUB pair, which is probing 15-month lows as we go to press. See my colleague Joe Perry’s article from last month discussing the correlation and implications for FX traders!

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Energy articles

April 17, 2024 05:00 PM

March 27, 2024 12:30 PM

March 18, 2024 04:00 PM

March 14, 2024 11:25 AM