MPC uncertainty makes it hard to tell if BOE will hike rates

The pound is the best performer in the G10 today after the Bank of England announced no change to its policy decision for March. Although […]

The pound is the best performer in the G10 today after the Bank of England announced no change to its policy decision for March. Although […]

The pound is the best performer in the G10 today after the Bank of England announced no change to its policy decision for March. Although rates will stay at record lows, there was one dissenter, Kirsten Forbes, who voted to hike rates. This has created excitement in both the UK bond markets and in the pound. GBP/USD is nearly 1% higher today and UK 10-year yields are at their highest level since mid-February as investors question if other BOE members will follow Forbes’ lead in the months to come.

Policy uncertainty as two MPC spots up for grabs

We don’t think that it is reasonable to assume that the majority of BOE members will be willing to vote for rate hikes in the coming months for a couple of reasons: firstly, Kristen Forbes’ term at the BOE is up in June, coupled with the resignation of Charlotte Hogg this week it means that there are two free spots at the MPC. We don’t know who will replace Forbes or Hogg, which leaves considerable uncertainty about the future direction of policy at the Bank.

If not for Brexit…

The second reason why we think that we are still some distance from a BOE rate hike is Brexit. We believe that if the government was not on the cusp of triggering Article 50 at the end of this month then the Bank may have raised interest rates on the back of decent growth and signs of inflation pressure. However, a rate hike at this stage, when there is still considerable uncertainty about the economic prospects of the UK when we are in the middle of Brexit negotiations, makes the prospect of a rate hike unlikely for the next 9 months’ or so, in our view. FYI- the Overnight Index Swaps market is only pricing in a 24% increase of a rate hike by the end of this year.

Could GBP’s good run come to an end?

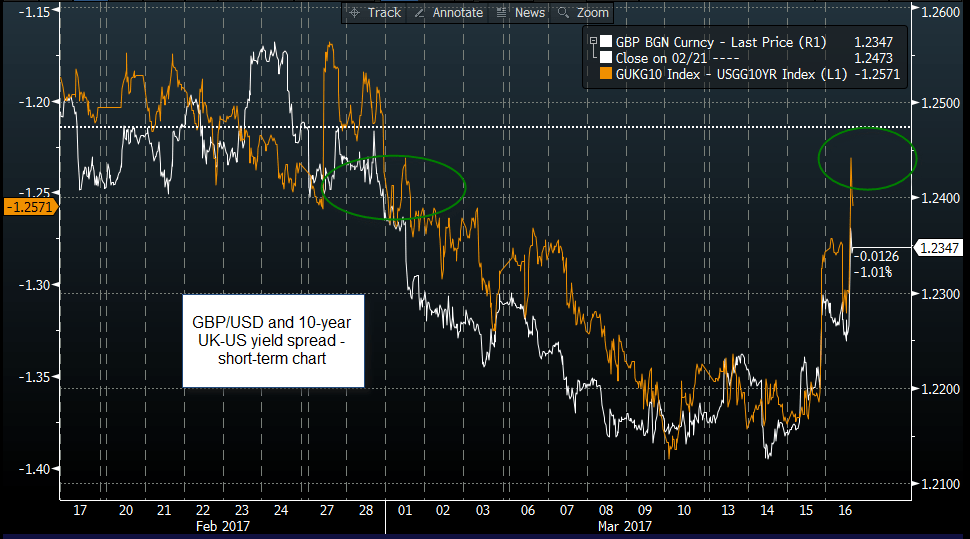

Thus, the market’s bullish reaction to the BOE decision may be over-extended, with only limited GBP/USD upside to come. The 10-year UK-US yield spread, which had reached a record low before the FOMC meeting, has risen to its highest level since the end of February on Thursday. Back then GBP/USD was trading at 1.24, currently GBP/USD is hovering around the 1.2350 mark, we believe that if we don’t see a further recovery in the UK-US yield spread then further upside for cable could be limited, and the market may fade the Forbes effect. Interestingly, the sell-off in the FTSE 100 has been limited post the BOE decision, suggesting that stock investors are not fully sold on the idea of more MPC members voting to hike rates in the near-term.

Figure 1:

Source: City Index and Bloomberg