Morrisons’ appeal goes further than special dividend and expanded Amazon deal

Wm. Morrisons’ special dividend announcement caps a half-year performance by the number-four UK supermarket that looks relatively solid, considering its less than optimal industry position and underlying sales growth that’s seen it pace only the worst performer among established chains, Sainsbury’s, for several quarters. The stock is faring better than its larger rival as the latter continues to lick its wounds after failing to buy Asda. MRW’s 4% so far this year fall compares with a 19% slump by SBRY. That nevertheless demonstrates widely disparate sentiment versus market leader, Tesco, whose long-standing efficiency and growth drive is now reaping benefits warranting a 2019 advance of 25%.

True, Morrisons’ key second-quarter sales—at stores open for at least a year and excluding fuel—were always going to struggle to match Q2 2018’s 6.3% surge. Then, the entire sector was buoyed by beautiful British weather, a royal wedding and the World Cup. In the end though, a 1.9% fall over the quarter to early August this year wasn’t as bad as widely expected. An in-line interim dividend garnished with a ‘special’ one-off payment helps convey the expectation that Morrisons’ strategy is showing increasing traction.

The strategy includes an expanded partnership with Amazon, that ought to provide further reassurance of some protection from the disruptive e-commerce giant. Morrison’s storefront on the platform will now distribute to more UK cities. In fact though, a move that MRW trumpets less than the Amazon deal, its tie-in with McColl’s, holds even higher medium-term potential. The arrangement to supply 300 additional units of the McColl’s chain adds volume, whilst a trial conversion of some units to Morrisons stores could boost the move towards higher joint participation. As such, there are now deeper inroads towards the upper end of a targeted £75m-£125m cumulative pre-tax profit after MRW booked £54m mostly from lower finance costs.

Major challenges remain, at both industry level (see Brexit) and for £4.8bn Morrisons. Sales growth per square foot continues to inch up, but growth remains more fragile than top rivals. MRW also still lacks a well-defined convenience format, leaving it vulnerable to challenges that go alongside the problematic online history with Ocado. The group is still catching up. Still, Ebitda margin expansion of 20 basis points in H1 and a £15m rise in underlying free cash flow back the view that an upturn has been seen. Against an action-packed industry backdrop, to say the least, a major takeaway for investors is that Morrisons remains on track to hit milestones that can open the door to further higher than expected cash returns.

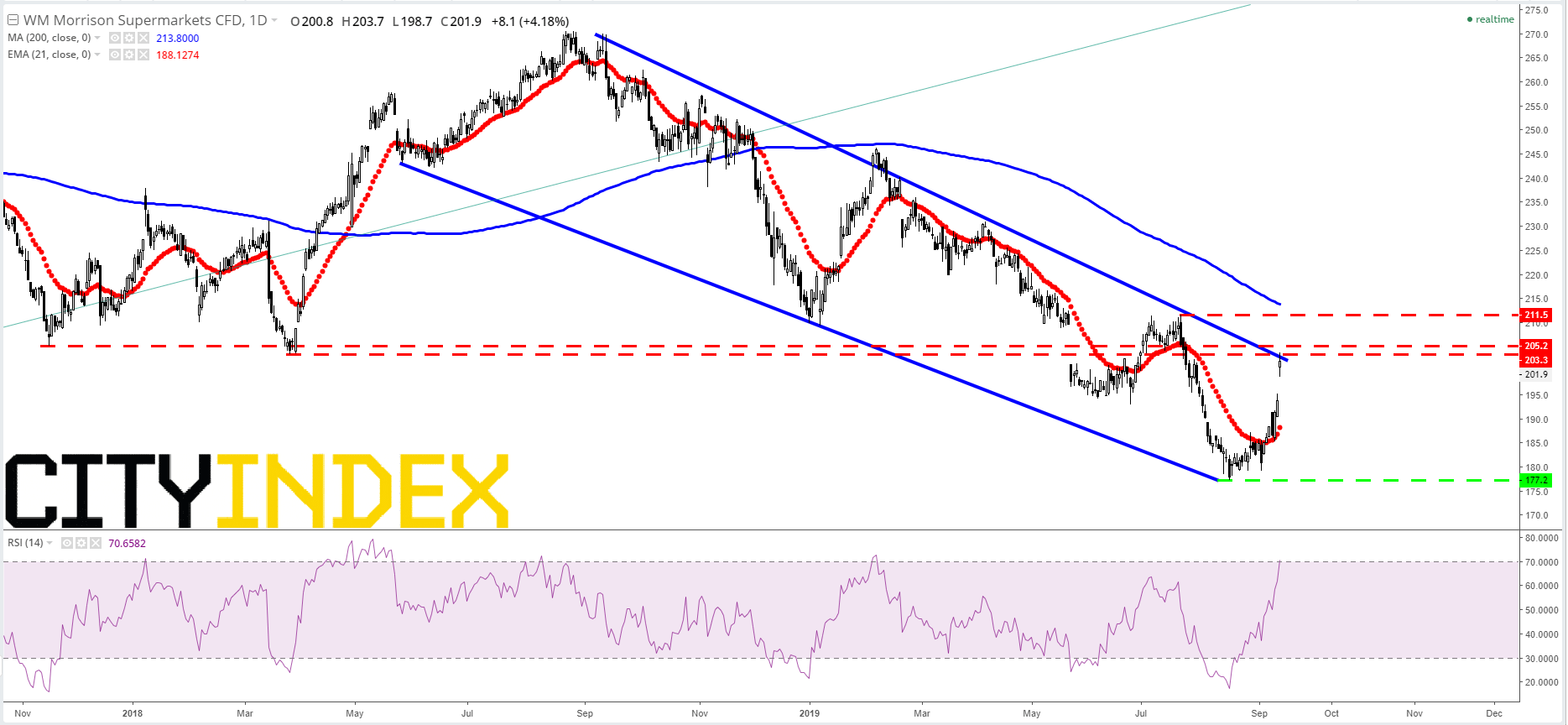

Chart thoughts

- An almost 3-year uptrend was broken last November, posing an overarching selling bias since then

- Some corroboration of that is shown by MRW’s falling channel in place for almost exactly a year; note Thursday’s rally hit the upper wall of the pattern

- The stock has also rallied to resistance from strongly defended November 2017 and March/April 2018 lows of around 205p and 203p respectively

- Failure here would imply another look at the 177p kick back low from August for support

- The 200-day moving average trends downwards encapsulating long-term weakness, but the 21-day exponential average is a ray of light. Its recent supports points to a possible trend change as it curves attractively upwards

- A break above 22nd July’s 211.5p failure high which was just short of the upper wall looks like it would confirm a turning point for buyers

WM Morrisons CFD – Daily

Source: City Index

Latest market news

Today 10:37 AM

Today 08:25 AM

Yesterday 10:36 PM

Yesterday 05:36 PM

Latest Abe articles

October 24, 2023 09:00 AM

October 19, 2023 01:42 PM

October 11, 2023 02:28 PM

April 25, 2023 02:36 PM