Morrisons to update investors in a week of retail surprises

The UK retail sector has continued to surprise this week. But in a break from recent trend, we’ve seen two big surprises on the upside, […]

The UK retail sector has continued to surprise this week. But in a break from recent trend, we’ve seen two big surprises on the upside, […]

But in a break from recent trend, we’ve seen two big surprises on the upside, instead of continuation of the seemingly never-ending string of new retail sector nasties.

Primark owner Associated British Foods on Monday confounded a fashion sector that has recently wilted in unseasonably mild weather, by reporting a rise in full-year earnings per share.

And on Tuesday, Marks & Spencer also surprised, when it posted its first half-yearly profit rise in four years.

No one believes the sector is particularly close to a comeback though.

Even so, this week’s exceptions to the recent retail norm might be worth keeping in mind tomorrow, when the latest British grocery stalwart faces the music.

Wm. Morrison Supermarkets Plc. will release its third-quarter Interim Management Statement, on Thursday 5th November.

We already know the numerous challenges faced by the UK’s biggest grocers have not really moderated since Morrisons last updated markets, on 3rd August.

In many ways, these challenges have intensified.

A monthly report from retail data monitoring firm Kantar Worldpanel released about two weeks ago, showed Tesco sales 3.6% lower in the 12 weeks to 12th October compared with the same period a year ago.

Sainsbury and Morrisons also continued to falter, with sales declines of 3.1% and 1.8% respectively, Kantar said.

During the monitoring period, grocery inflation saw its thirteenth successive fall and stood at -0.2%, Kantar noted.

“This means shoppers are now paying less for a representative basket of groceries than they did in 2013”, the data provider added.

There were some positives in its report, but they were slim ones for the big establishment grocers.

For instance, Tesco’s rate of sales decline was “the grocer’s best figure posted since June.”

Instead, the real benefits emerged at the ‘premium end’ of the market, including the likes Waitrose and Marks & Spencer (partly corroborated by M&S’s results this week) and also at the ‘value end’, including Aldi, Lidl and others.

“We are seeing clear polarisation of the market with both the premium and discount ends of the market gaining share, while the mainstream grocers continue to be squeezed in the middle”, Kantar said.

“Asda has again emerged as the winner among the big four, growing sales ahead of the market, up 1% over the past year, boosting its share to 17.3%” Kantar added.

The question is ‘where does Morrisons sit in the premium-value scale’? (Anywhere?)

And, judging by the scope of the turnaround plan Morrisons announced in mid-March, questions remain about how it seeks to establish a niche that would enable it to regain substantial market share.

The key points of its plan:

Aside from turnaround progress, this year’s grocery sector shenanigans have pushed investor focus on to other major factors by which to judge the UK’s ‘Big Four’, including Morrisons.

Finally, investors have abandoned, at least temporarily, attempts to relatively value major UK supermarket groups on a price-to-earnings basis, largely due to difficulty in establishing a credible run rate for average earnings.

Almost by default, this has left dividend yield as the single most important criterion for whether to hold supermarket shares.

There has been a clear differentiation between the stock performance of Tesco and Sainsbury, largely because the latter has left itself more room to maintain an above-market-average dividend than the former.

And Morrisons’s latest yield at 8.5% would appear to place it above both.

How long can this last?

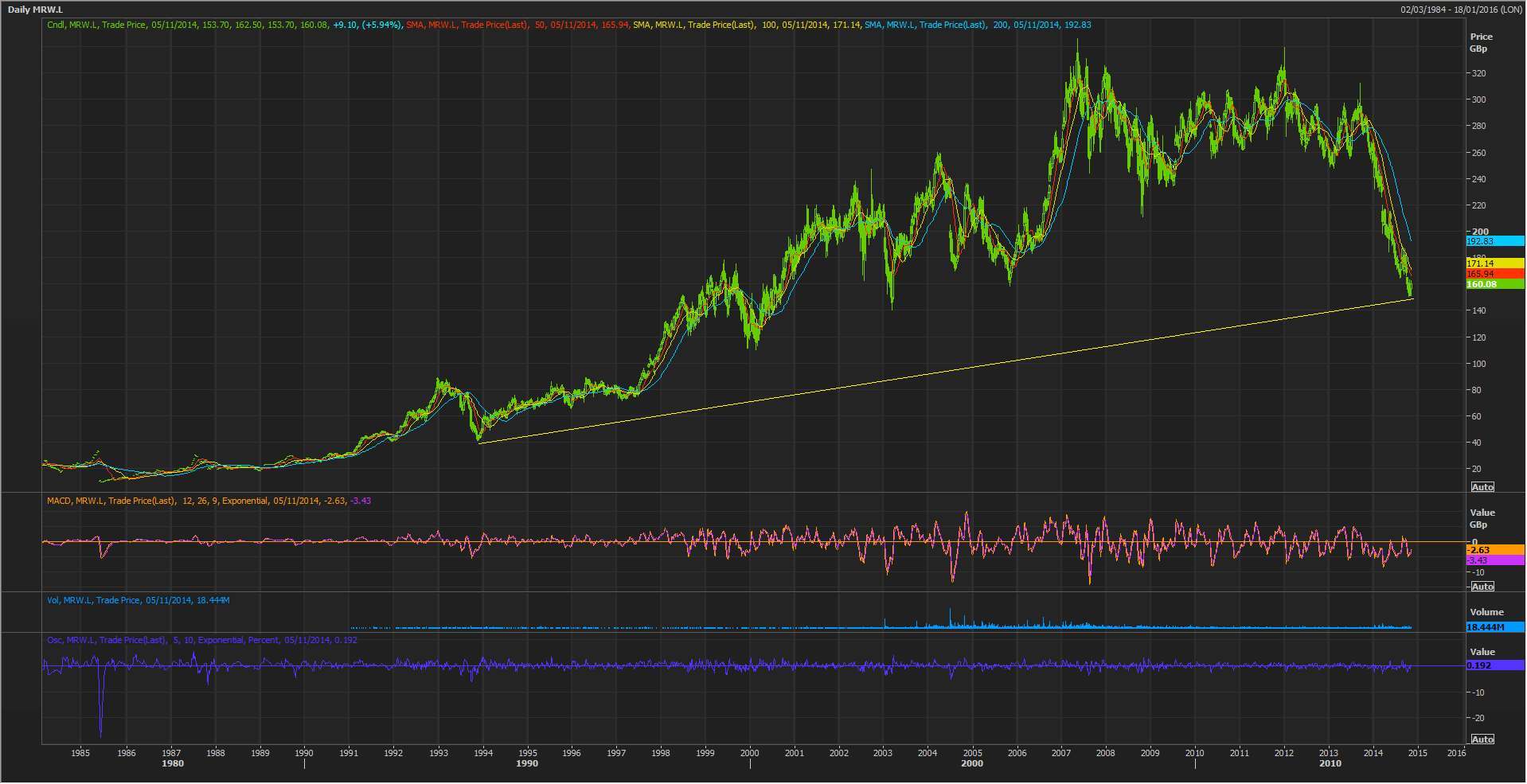

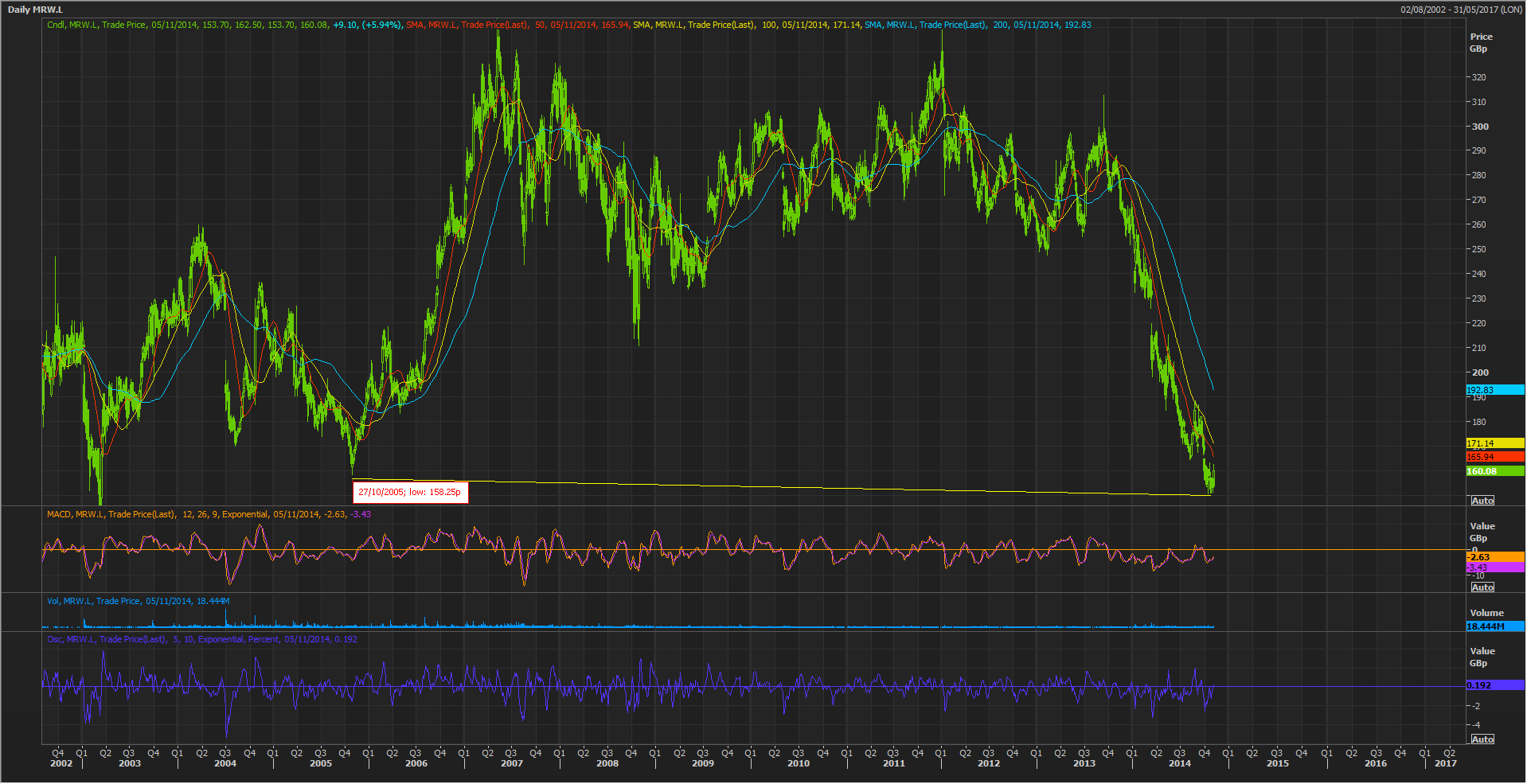

The answer will be a major factor deciding whether Wednesday’s Wm. Morrison stock gains (circa 6%) will be retained.

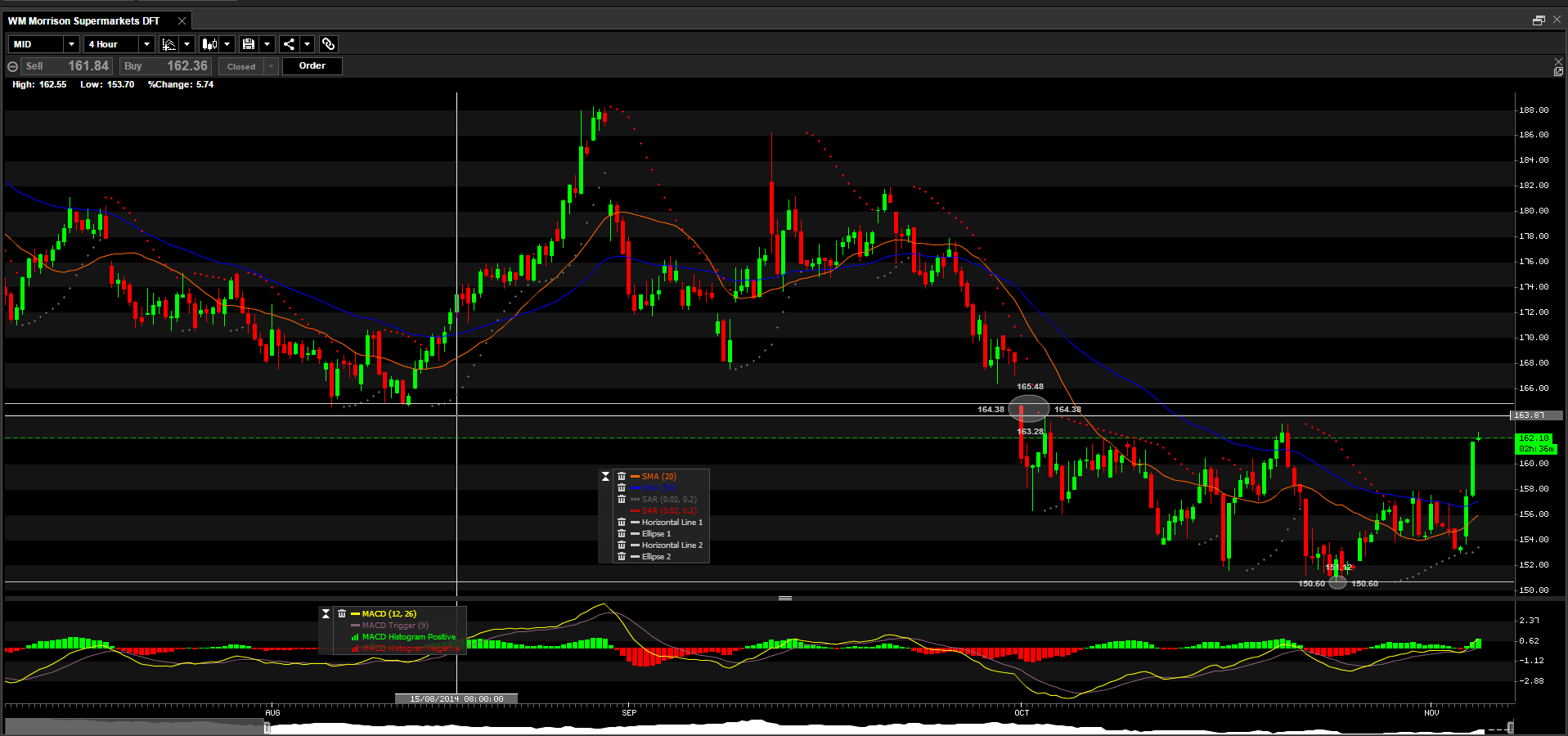

WM Morrison Supermarket Daily Funded Trade, within City Index has clearly retreated beneath a pivot of around 162p since the 1st October, just in case.