Morrisons breakthrough threatened by price cuts

Updated 1.37pm BST Morrisons remains the best-performing major UK supermarket stock this year and is set to report its first profit growth in four years, […]

Updated 1.37pm BST Morrisons remains the best-performing major UK supermarket stock this year and is set to report its first profit growth in four years, […]

Investors in Britain’s grocers, hungry for returns after a punishing couple of years, have steadily added Britain’s fourth-largest supermarket chain, after its shares bottomed last December, six months into new CEO David Potts’ watch.

The re-rating helped the group shrug off Brexit with a sharper rebound than rivals, leaving its shares 31% higher since January.

Potts’ smarten-up-and-cut-down strategy—more localised ranges, lower prices, and a faster supply chain—has borne fruit.

The group has reported two straight quarters of underlying sales growth, the first rises in three years, setting it on course to unveil half-yearly underlying pre-tax profit of £150m, a modest 6.4% year-on-year improvement, but still an end to four-years of losses.

Rivals have, of course, not stood still. Tesco and Sainsbury’s continue to lock horns with their German nemeses, Aldi and Lidl, with relentless price-cutting programmes of their own.

It is also no coincidence that supermarket stocks tumbled last Friday—Morrisons’ the most—after Asda’s new boss introduced his first wave of price cuts.

Wal-Mart’s British subsidiary, the UK’s No.3 grocer, is wary after Morrisons’ same-store sales rose 3.1% in the first quarter whilst Asda’s have lagged the industry for two years.

On Friday, Asda said prices had been cut by an average of 15% on thousands of own-brand products, the latest in a barrage of reductions which began in 2013 with a target of £1.5bn.

The price war has also spread to the fast-growing online grocery market, where Ocado shows further signs of losing first-mover advantage.

Its CEO admitted on Tuesday the group was “seeing sustained and continuing margin pressure and there is nothing to suggest that this will change in the short term”.

Under such conditions, even marginal tailwinds can add value. For Morrisons, heavy investment in food production and packaging that made it Britain’s second largest food manufacturer looks even more astute after Brexit.

The group says it imports much less food than the industry average, reducing exposure to input prices—particularly food—which surged at their fastest rate in almost two years in August, very largely due to the heavy fall of sterling after the referendum.

A multi-channel online approach also offers increased volumes, with little upfront outlay: Morrisons’ renegotiated deal with Ocado won much more favourable terms, and it now supplies recently launched Amazon Fresh too.

It might, for instance, fail to ramp food production fast enough, thereby allowing rivals’ ‘investment in price’ to take root with consumers.

It will also need every ounce of firepower over the coming years to keep a grip on market share, which is still falling, albeit more slowly, and with most of the recent ebb due to closure of loss-making stores.

Morrisons will therefore need to decide if emerging balance sheet strength—net debt down 40% since 2014—should be deployed on returning cash to shareholders in about 18 months, or, yes, invested in more price cuts.

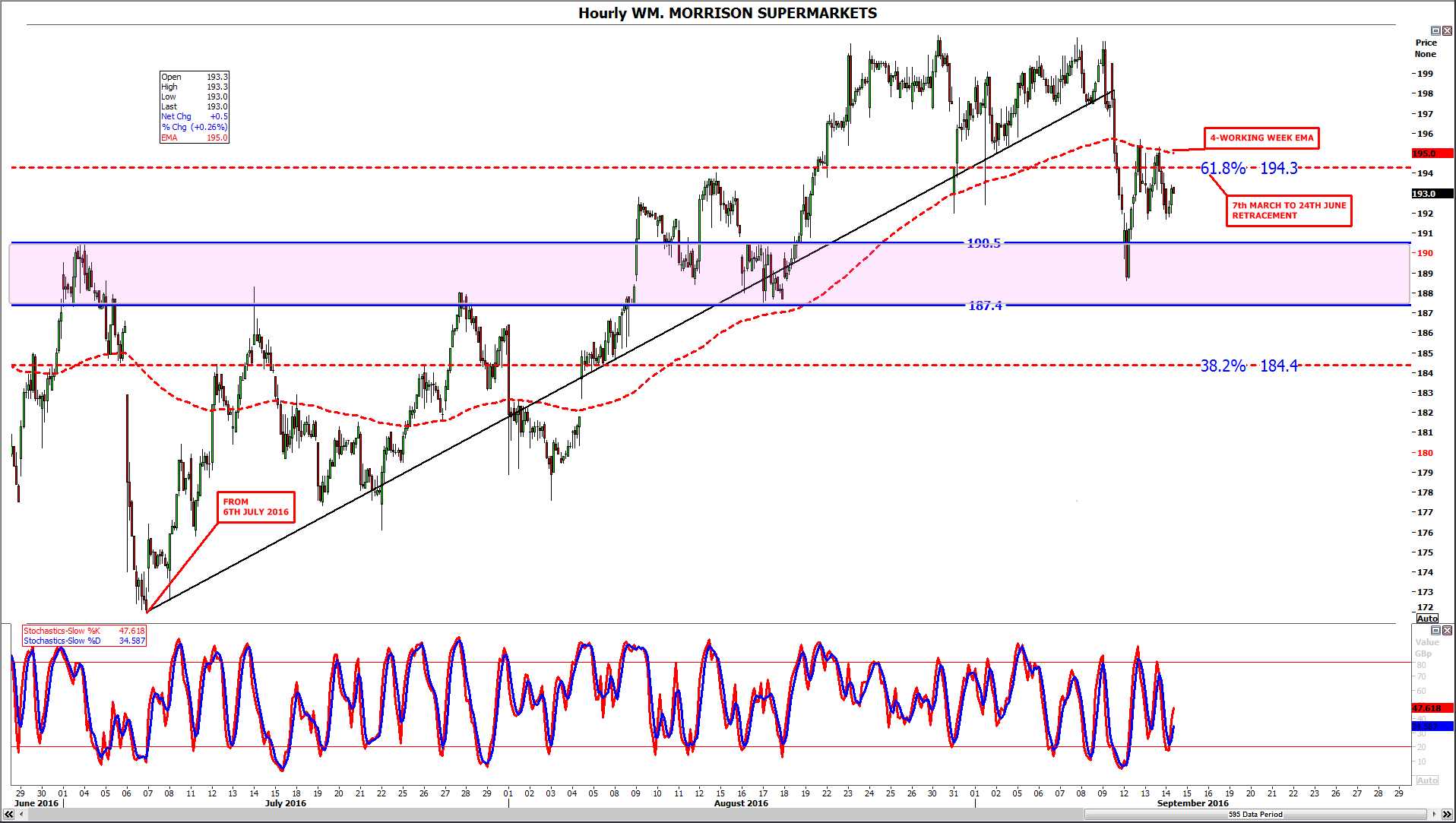

From a technical perspective, Morrisons’ shares are facing their biggest challenge since late June, coinciding with the latest round of the price war.

A jittery rising trend from early July was definitively broken on Friday, when the important 61.8% Fibonacci interval of the share’s March-to-late-June slide, also collapsed. The marker is now a resistance.

Support remains within the range of 190p-187p, the beginning of Morrisons’ Brexit slide and the point of August’s bounce respectively.

Continued inability to best 194p (61.8%) increases the chances of another test of the support which the stock might fail.

Bulls might also like to see a revival of the four-market week exponential average (170 hours) which has also capped the shares this week.

Please click image to enlarge