CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

69% of retail investor accounts lose money when trading CFDs with this provider.

Menu

Morning Briefing FTSE skims Brexit

The FTSE is continuing its remarkable divergence from just about every major stock market everywhere.

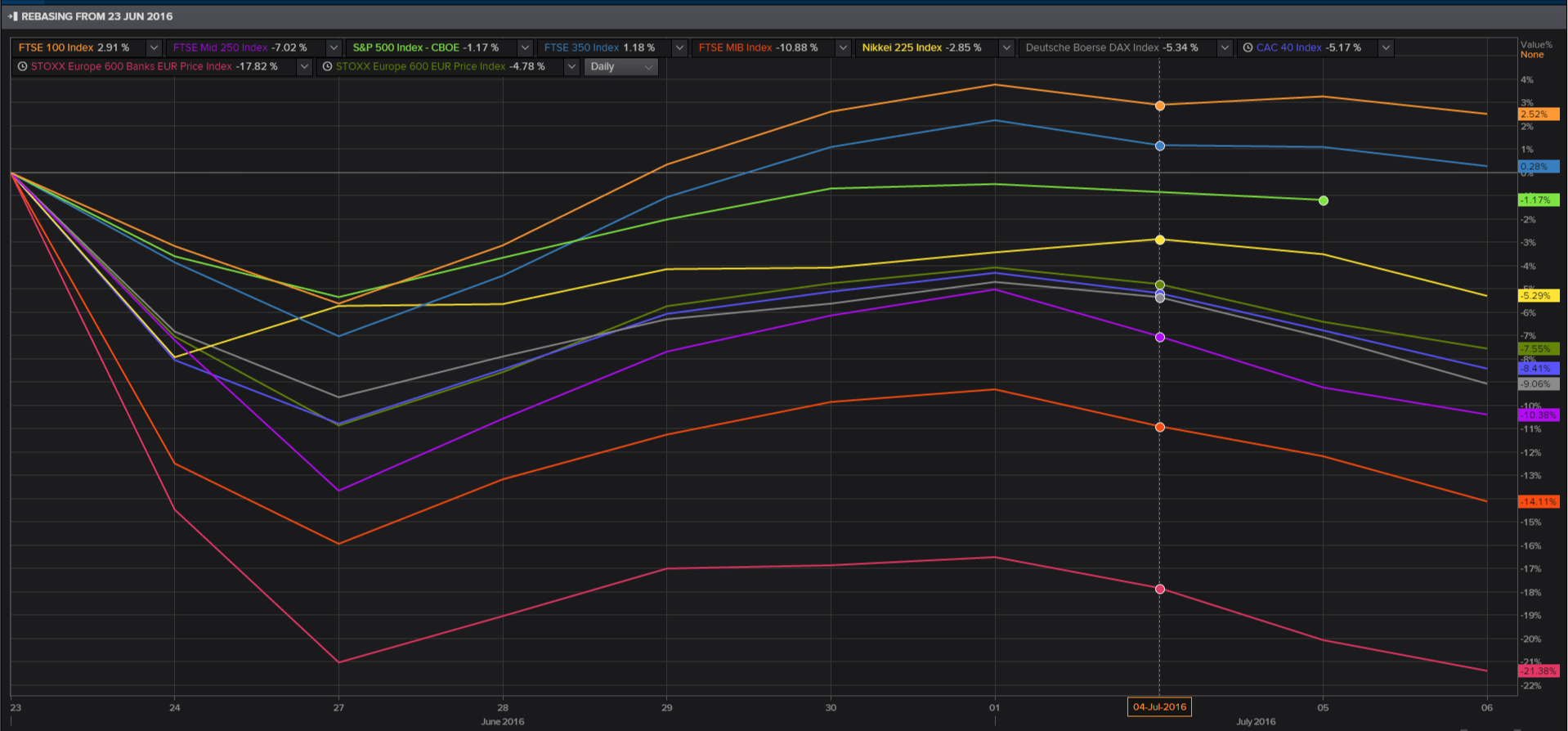

The FTSE is continuing its remarkable divergence from just about every major stock market everywhere. In the wake of the Brexit vote it had inched some 3% higher up till Tuesday’s close, whilst the S&P 500 has eased about a percentage point, Nikkei is down 3.5% and DAX has lost 9%.

Clues about the disparity can of course be found closer to home. The main index of UK-listed firms with lower market values (FTSE 250)—which also tend to be more domestically focused—has tumbled 10%. It’s all about sterling. Multinational behemoths like Shell, BP, HSBC, AngloAmerican, Rio, BHP and others, have about as much to do with British politics and the economy as the price of fish. With the pound etching the latest of its recent string of new 30-year lows against the greenback as I write this—$1.2931—UK administrative costs and export prices are lower, dollar-denominated revenues translate higher. Whether or not the FTSE can derive a sustainable or reliable lift from a weak pound is another matter entirely. The fact that life is more complicated is reflected in the FTSE edging lower on Wednesday, despite cable’s weakest values for three decades.

The clearest trigger for sterling’s latest leg lower was the chilling effect of suspended redemptions from investment funds linked to the property sector. The latter has turned out to be a much clearer channel of market anxiety than even the UK’s big banks, most of which traded in the black on Tuesday when the Bank of England unveiled its plan to divert capital originally intended for regulatory buffers, back to customers. It’s telling that the smaller ‘challenger’ banks, like Virgin Money, Shawbrook, Aldermore and others slid as much as 7% on that news, as investors grew cautious on their bigger and less diversified exposure to the UK. At the same time, Barclays, StandardChartered and HSBC, were in the black for most of Tuesday and closed with just modest losses. Lloyds and RBS were sold for similar reasons, though to a lesser extent than their smaller British rivals.

As for the property firms fear is the key. The biggest shares in this group are being led lower at the time of writing by BarrattDevelopment, which is ebbing a further 6%, and taking its fall this year to 50%. Property values have yet to be confirmed as definitively lower, given that the referendum happened less than a fortnight ago. But market forecasts that commercial property prices could fall at least 10% this year—and even as much as 25% according to research released in March by Colliers—have encouraged investors to flee for the hills. Or at least they would if they could. Either way, any hard data that offers a more contained scenario of Brexit impact could have an elastic effect on many property shares; it stands to reason that some of the selling has been indiscriminate. The next set of relevant surveys are at least a month away though, whilst the Bank of England will announce its interest rates decision next week. Understandably there is much speculation that the days over which the Bank’s 25 basis point rate will continue to apply are numbered accordingly. That brings us back to sterling.

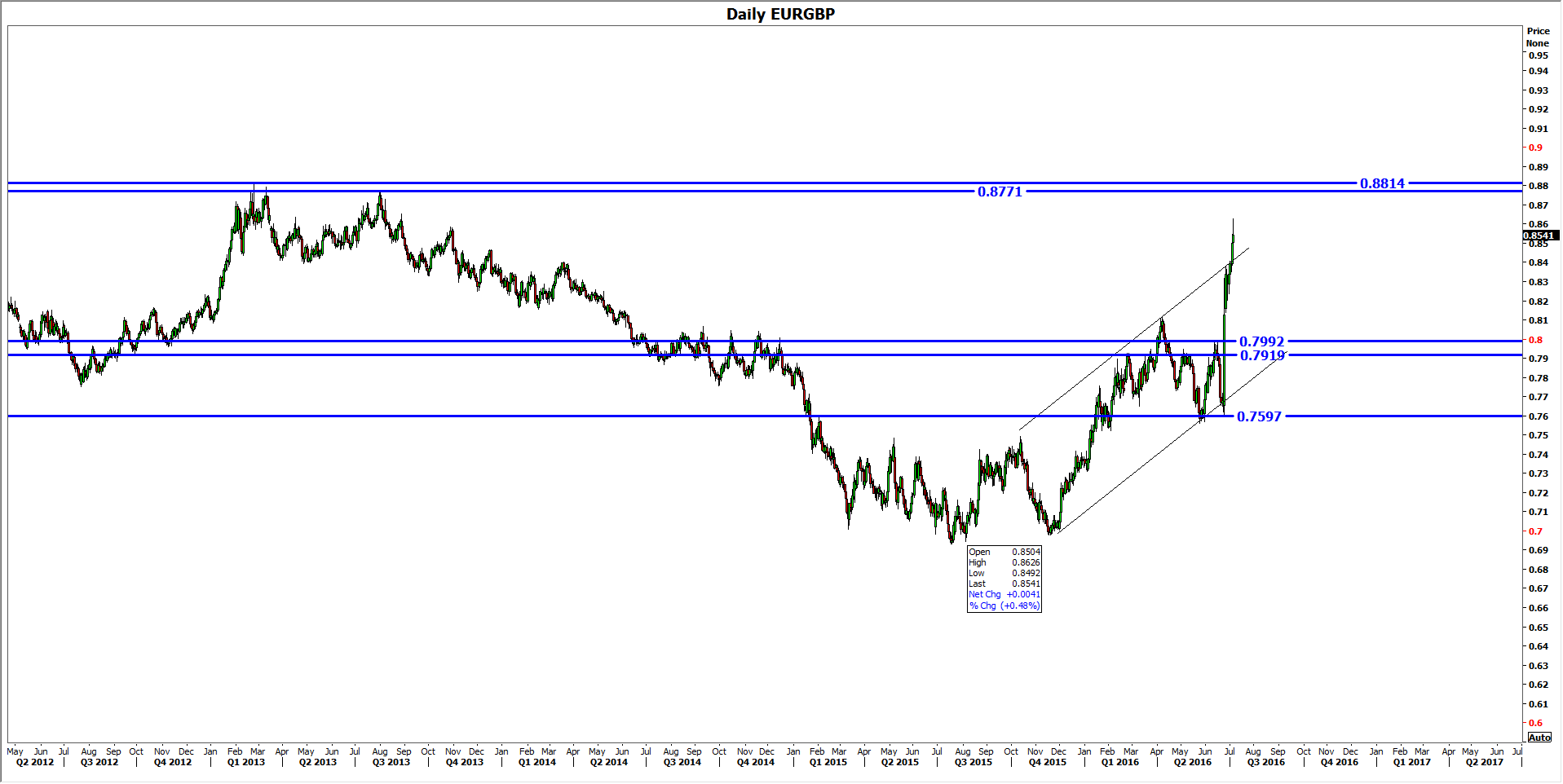

And the reflexive effect of its collapse on the euro.

DAILY CHART: EUR/GBP

In theory, the presumed destruction of stops beyond the rising channel in place since late-2015 leaves the rate unfettered, and with few barriers before 87p at least. It was last at 85.39p, having tagged an earlier 2016 high of 86.26p again, a couple of days ago. On the other hand, the euro’s ascent since 23rd June can certainly be regarded as having been on the wrong side of ‘plausible’—and that’s clear from its collapse against the dollar, against which it set monthly lows on Wednesday at $1.1037. EUR/USD weakness could begin to seep into sterling trading at the first sign of Eurozone weakness. When that weakness might turn up is another issue. Economic data from the region has been steadily confounding low expectations for coming up to two months. Eyes on Thursday’s ECB minutes for further clues about the outlook. Particularly after German manufacturingorders this morning followed the recent trend with a flat reading year-over-year and on the month too, compared to a sharp fall foreseen since May and a still sizeable 0.6% drop expected annually.

Look at Canadian and United Statestrade balance data, for the main economic pointers this afternoon. They’ll be followed by the US ISM non-manufacturing index, a services sector PMI, and, most importantly FOMC minutes at 7pm London time. Any hint from these readings that tilt in any way back to more of a tightening bias at the Fed could stop the yen in its tracks. At least for a while. The advance continues; now on the 100 handle. Remember the low on 24th June was actually 99.11 yen per dollar, 36 sen from the price at last check.