Monitise can survive without Visa Inc

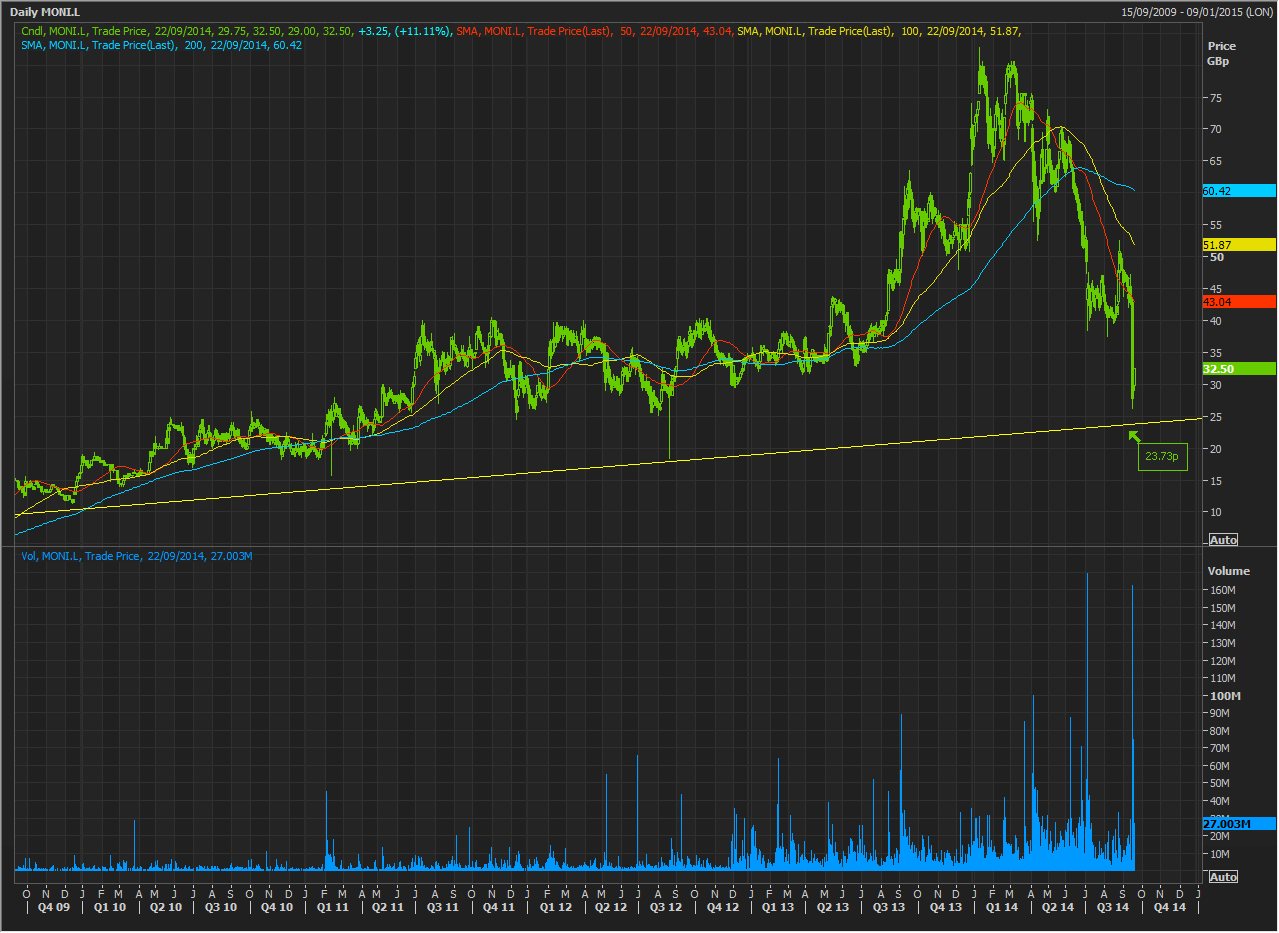

Shares of Monitise, the AIM-listed mobile payments firm, closed 11% higher today, clawing back a fraction of the losses made last week when Visa […]

Shares of Monitise, the AIM-listed mobile payments firm, closed 11% higher today, clawing back a fraction of the losses made last week when Visa […]

Shares of Monitise, the AIM-listed mobile payments firm, closed 11% higher today, clawing back a fraction of the losses made last week when Visa Inc. said it was reviewing its stake.

There didn’t seem to be any specific additional news behind today’s stock bounce which was worth little more than 3p.

However, with the stock having lost more than a third of its value last Thursday alone, Monday’s uptick might still signify that the worst of the recent sell-off has passed.

It was on Thursday last week that Visa Inc., Monitise’s fourth-largest shareholder and also its biggest customer, announced it was considering the sale of its 5.5% stake.

Visa, the world’s largest credit and debit card company said it was “considering its options”, having first invested in Monitise in 2009 by purchasing a 14.4% stake, when the company’s revenue was about £3m. It’s gradually reduced that stake.

“Visa intends to continue increasing its investment in its own in-house capabilities and, as a result, reducing its use of external resources,” Visa said.

Visa’s agreement with Monitise is meant to continue until 2016.

The news came only a few days after Monitise said full-year losses had increased at twice the rate at which the firm was generating revenues.

The firm reported in mid-September a 30% rise in sales for the full year but said cost of sales expanded 70%, whilst losses before interest, tax, depreciation and amortisation (negative Ebitda) increased 62% to £31m.

The company reiterated its intention to be profitable by 2016 and said it would invest between £35m and £45m in capital projects during 2015.

Monitise also announced the second of two major partnerships in recent months with its annual results, an agreement with Santander to introduce Monitise technology.

That came after the firm announced a tie-up with IBM Corp. in August which would provide Monitise with access to companies in the US technology conglomerate’s client base.

Monitise appears to be pursuing a strategy of providing banks and other firms with wireless payments services and also new ways of making money from their data, including using apps as marketing platforms.

Without the announcement of new partnerships shortly before Visa’s re-think, Monitise stock might have fallen even further.

The UK firm’s stock closed down 35% on Thursday and has lost more than 50% of their value in the year-to-date period.

Having hit highs around 80p earlier this year, the tide for the stock turned amid a switch in investor sentiment away from the broader technology sector with concerns over valuations.

Additionally, Monitise made two profit warnings as it began a transition away from a licensing model toward one requiring subscriptions.

Monitise has spun the Visa news as being in-line with Visa’s normal way of operating with start-up investments, investing early and gradually exiting over time.

“What’s happened today is consistent with Monitise’s strategy. For many years we were accused of being a Visa shop, and now we’re an agnostic network”, Monitise’s joint chief executive and co-founder Alastair Lukies said on Thursday.

In further defence of its prospects, the company maintained its 2015 and 2016 guidance and reiterated 2018 targets too.

Monitise’s reaffirmed 2018 expectations suggest it was not expecting a major contribution from Visa after FY16 in any case.

This does not obviate the risk that other major Monetise customers and partners may follow Visa’s lead and take wireless payments in house.

However, Monitise’s forecasts at least suggest it regards its customer base and increasing focus on mobile banking and mobile commerce as sufficiently diverse to offset all but the most severe rate of customer withdrawals.

Traction in these business areas ought to be visible by 2015, so investors will need to scrutinise trading statements carefully.

Even before then, it looks like last week’s share price rout may have been overdone, with the company now trading on an enterprise value over sales multiple of 4 times–30% below the 5-year median level.

It’s also positive Monitise’s debts are worth less than 1% of its equity on a trailing 12-month basis, although as implied by a rising cost of sales, the firm has been cash-flow negative for at least five years.

Overall, sentiment in the stock appears to have reverted to the firm’s ‘base case’ and in keeping with that, traders seem unwilling, at least for the moment, to test a rising support trend line on the chart, which has been respected for more than 5 years.