Money printer De La Rue loses 223m in one morning

De La Rue Plc. the venerable British money printer joined the list of UK firms warning of falling profits on Friday, triggering a sell-off in […]

De La Rue Plc. the venerable British money printer joined the list of UK firms warning of falling profits on Friday, triggering a sell-off in […]

De La Rue Plc. the venerable British money printer joined the list of UK firms warning of falling profits on Friday, triggering a sell-off in its shares of more than 33%.

The stock’s biggest one-day fall in over a decade took the stock to a four-year low and represented the loss of £223m from the company’s market cap on Friday morning alone.

De La Rue warned that trading conditions in all its businesses had deteriorated and said pricing pressures were likely to continue into the 2015-16 financial year.

Contractual price reductions would occur during the same period, the company added, repeating a theme it voiced last year.

Today’s warning is De La Rue’s third in two years.

The company appears to be struggling to keep up with changing conditions in the business of producing national legal tender.

The industry is transitioning in line with an increasing trend toward the use of electronic transactions by consumers and corporations.

In June of last year, the firm slashed forecasts, after adjusted operating profit from the currency division fell by 16% whilst the 12-month order book was £25m down compared to the year before.

Some of the orders were received after the end of the 2013 financial year, De La Rue said.

In October of last year, the firm said it would make around £90m in operating profit for 2013/14, compared with a target of £100m set in its three-year improvement plan introduced in 2010/11.

De La Rue has been warning of pricing pressure since 2012, when it said competitors were adding capacity to manufacture blank banknote paper and printed banknotes.

For the current 2014-15 year, underlying operating profit and underlying pre-tax profit will be approximately £20m lower than that reported for 2013-14.

In its bank note business, De La Rue said pricing remained disappointing, leading to reduced margins.

Growth in its business providing product authentication and cash management processing services had been significantly slower than expected, the firm added.

De La Rue makes over 150 national currencies and UK passports.

It said business had suffered because some expected contract tenders failed to materialise with countries retaining incumbent suppliers. Take-up of electronic passports had also disappointed.

On top of the profits warning the firm also announced a dividend pay-out for the half-year of 8.3p compared with 14.1p in 2013-14 and said it would have to “reappraise” its dividend policy of recent years.

To call De La Rue’s dividend policy up till now ‘generous’, would be something of an understatement.

Pay outs as a percentage of profits amounted to more than 89% in the last fiscal year and an effective 110.63% on an interim basis.

The warning about the dividend surely helps explains the severity of the share price loss today.

Even so, the FTSE 250-listed firm’s chairman, Philip Rogerson was determined to remain optimistic about the company’s prospects.

“While disappointing to announce this trading update, De La Rue … remains a strong, profitable and cash-generative business,” he said in a statement.

“We will continue to pursue efficiency gains, invest in the business and in R&D for the future”, he added.

The group has not had a CEO since March, when the prior chief executive Tim Cobbold left.

Martin Sutherland, formerly of BAE Systems will begin on 13th October.

Before Friday’s warning, analysts had been expecting De La Rue to post pre-tax profit of £81.6m.

The market rating for the next twelve months has gone way out of kilter after today’s share price collapse. Forecasts place the company on a price-to-earnings basis of 12 times, a small premium to the sector.

This must at least be halved now.

De La Rue is not a distressed name although it was geared up almost 500% against the value of its equity over the last 12 months on average –its peer group median is about 47%.

A volatile free cash trend showed a recovery to £27.8m from £4.2m in the red the year before, and £53.4m in the black in the prior year.

De La Rue stock is readjusting today following news earlier this month that it was preferred bidder on a 10-year contract to print Britain’s paper and new plastic banknotes.

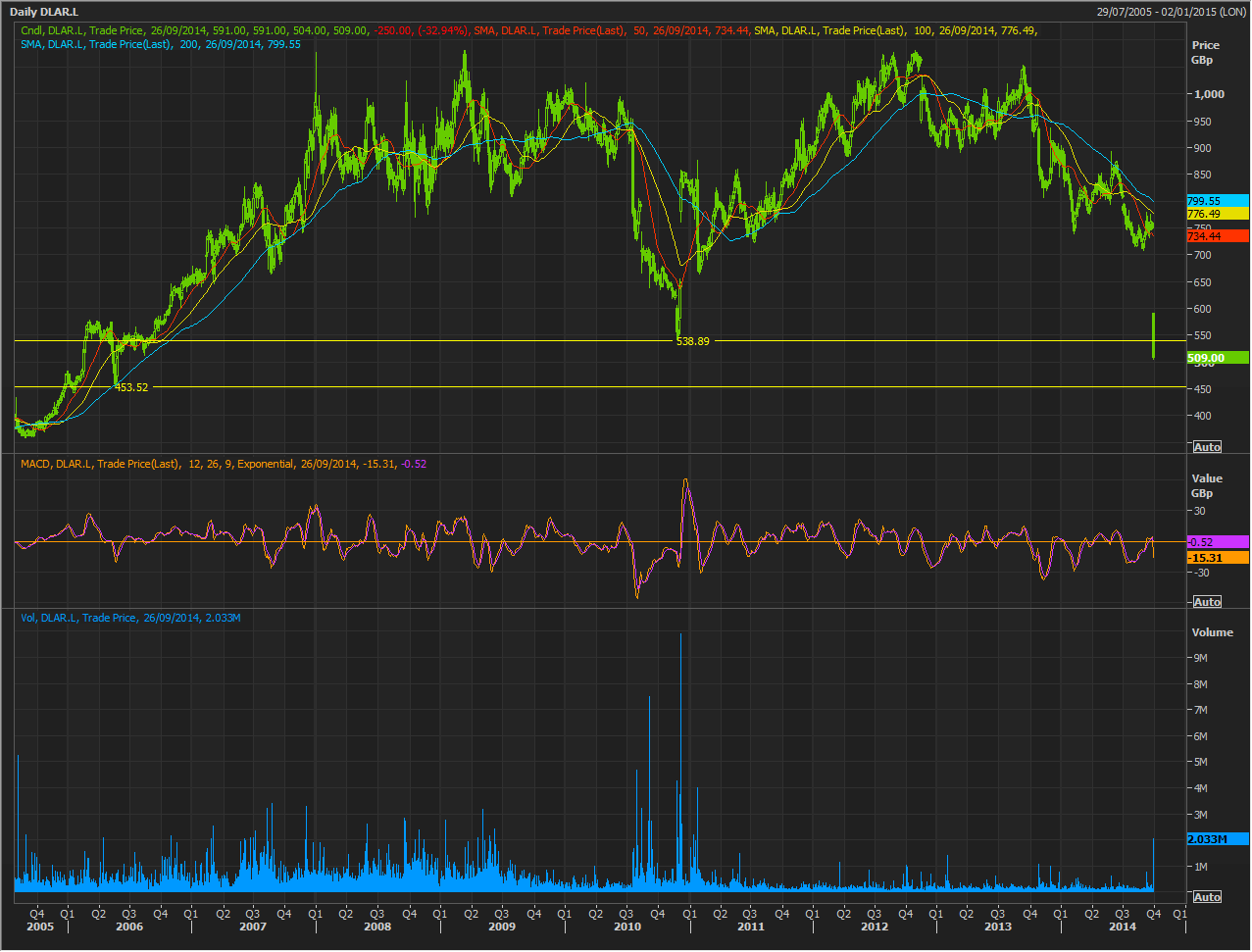

The stock has this afternoon shot past the three-year low point of January 2011 at 538.89p and looks like it might need the next major downside marker, 453.50p, from May 2006, as a landing matt.

Participation in the current sell-off is relatively small so far, compared to prior years.

With momentum on the downside currently emphatic, the share needs to fall significantly more in the near term.