Moderna’s Vaccine Reinvigorates Markets, but Long Winter Still on Tap

Just a week after Pfizer and BioNTech announced interim results on their 90% effective COVID-19 vaccine, Moderna announced its trial vaccine was 94.5% effective in initial results this morning. Perhaps more importantly, there have been no severe cases among people who received the Moderna vaccine, a development that the company’s CEO classified as “a game-changer.” Both Pfizer and Moderna expect to seek emergency-us authorization from the FDA in the coming weeks, with distribution anticipated to start around the turn of the year.

The market reaction has been more muted than the response to the Pfizer vaccine results last week, but we’re seeing some of the same trend play out. Global equities are trading higher across the board, with the notable exception of “stay-at-home” US tech stocks (names like Zoom Video, Peloton Interactive, and Docusign). After rallying 7% last week alone, small capitalization stocks (a proxy for the “reopening trade”) are seeing another strong rally at the open:

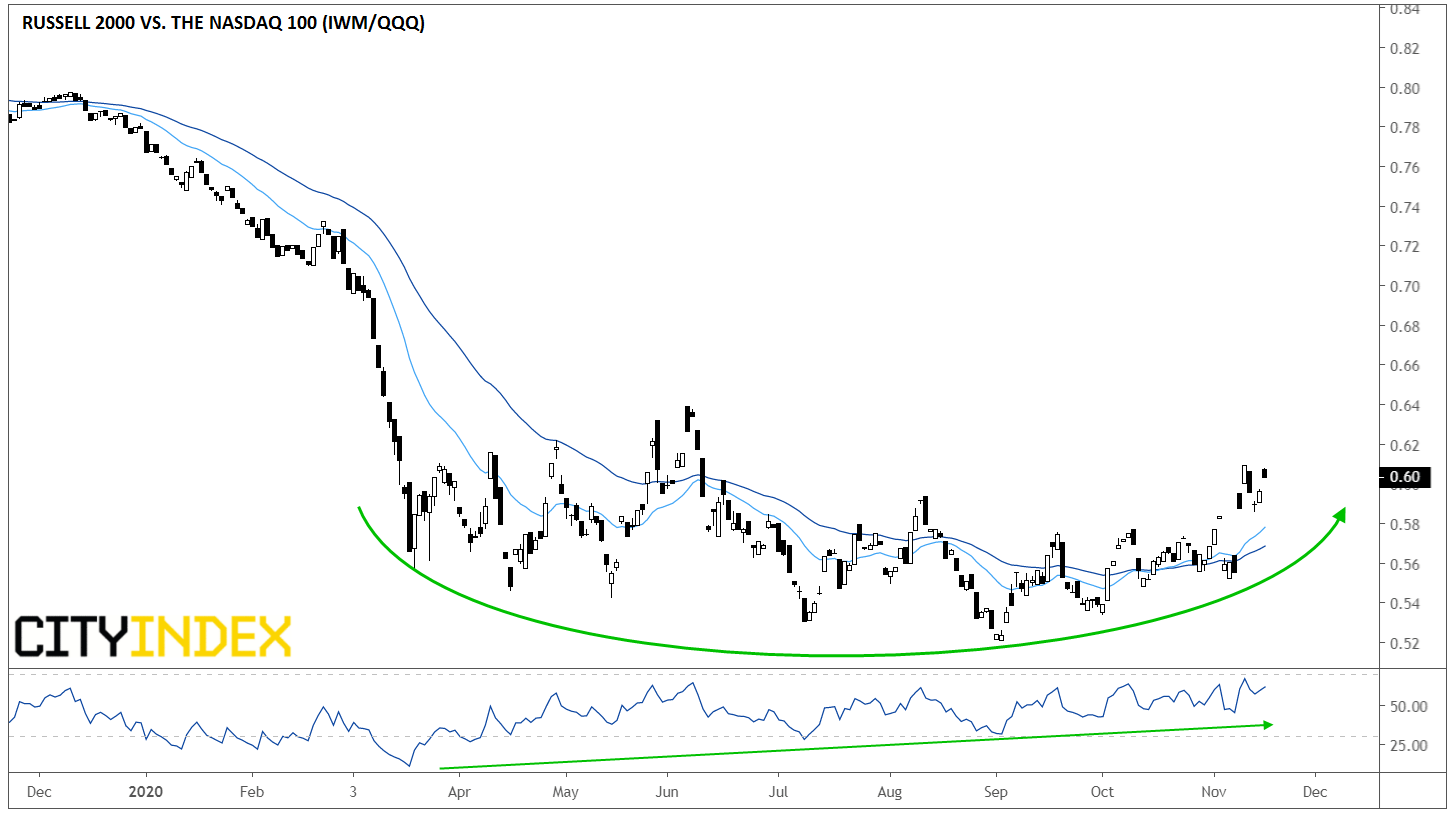

Source: TradingView, GAIN Capital

As the chart above shows, the small-cap focused Russell 2000 is strongly outperforming the tech-heavy NASDAQ 100 over the last week, but it still has plenty of ground to make up to unwind the steep underperformance through the first half of the year.

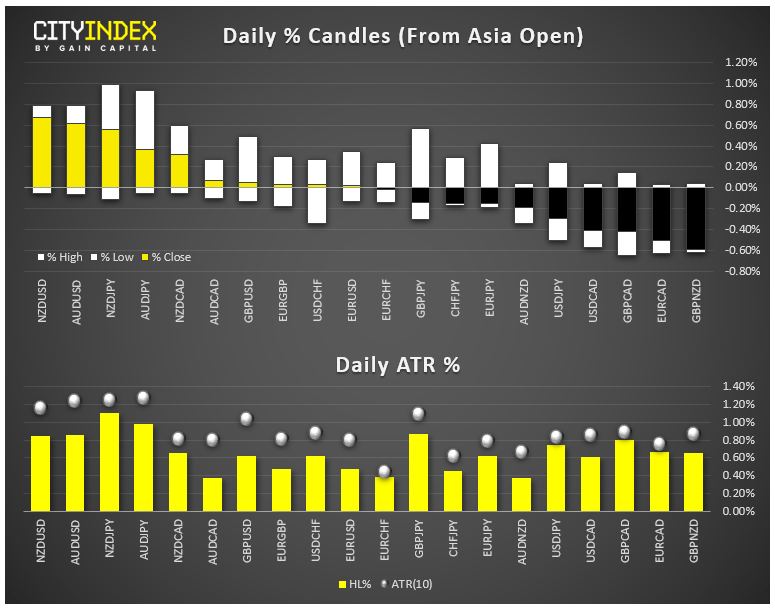

In other markets, oil has caught a bid with the US benchmark WTI contract rallying nearly 5% so far, while gold is essentially flat on waning demand for safe-haven investments. Meanwhile, yields on the 10-year treasury bond are ticking higher to 0.91%. Finally, the trends in the FX market are reflecting the “risk on” sentiment that we’ve seen in other markets, with the “commodity dollars” (New Zealand, Australian, and Canadian dollars) leading the way, while the safe haven Swiss franc and Japanese yen bring up the rear:

Source: GAIN Capital, Eikon

While today’s news is bullish and may help extend the nascent trends we saw start forming last week, readers should recognize that the “reopening trade” will not be a one-way street. With COVID infections surging across the Western world and hospitals overflowing in the hardest hit areas, there will still be plenty of back-and-forth trading opportunities as traders weigh the short-term pain against the long-term economic optimism.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Coronavirus articles

January 5, 2023 08:14 PM

December 6, 2022 05:03 PM

September 1, 2022 04:28 PM

August 1, 2022 08:40 AM