China’s economy shows signs of stabilisation though industry views reveal pessimism

Base metal mining and steel shares led resurgent European stock markets on Friday following some reassuring aspects in Eurozone data. The gains, which saw the big four—BHP, Rio, Glencore and Anglo rise 2%-to-3% each—partly reflecting relief. The industry has been led a merry dance over the last couple of years as deteriorating relations between Washington and Beijing have exacerbated China’s economic slowdown, chilling miners and metal producers’ most important market.

The early part of 2019’s final quarter appeared to show signs of a turn for the better. Chinese data looked set to stabilize, at least on the surface. Readings showing higher than forecast inflation, PMIs, and steady growth so far this year, roughly coincided with a rebound of mining and metal stocks. Bloomberg’s Europe Mining Index has erased a 4% loss that underperformed the FTSE 100 by some 9 percentage points by mid-August to trade around 9% higher over the year-to-date by Friday. That’s now in line with benchmark’s 2019 rise.

Dither and uncertainty continues to characterise prospects for a ‘phase-one’ trade deal, though sentiment has been underpinned by outward progress of talks since a tentative agreement collapsed in May. The tail-off of declines in Chinese indicators together with a calmer trade outlook has even prompted analysts at some banks to upgrade some mineral volume forecasts. For instance, Citigroup now expects a recovery across many mined commodities, except thermal coal, over the next four quarters. That view, as well as a mellower take by investors on trade sees European steel makers ArcelorMittal, Salzgitter and SSAB rise some 2% to 4%.

No one believes the miners and metal makers are in the clear, of course. JPMorgan’s global manufacturing PMI rose in October, though remained below 50, denoting continued broader contraction, despite China’s resilience. Even there, October credit data and a complete standstill of new infrastructure approvals counters improving conditions elsewhere. Little wonder sentiment at the LME’s recent industry event was reportedly ‘unenthusiastic’, particularly about copper, in which demand growth is expected to average below 2% over the next few years. The underlying consensus seems to be that the demand outlook remains too uncertain for markets and producers to fully commit to more optimism.

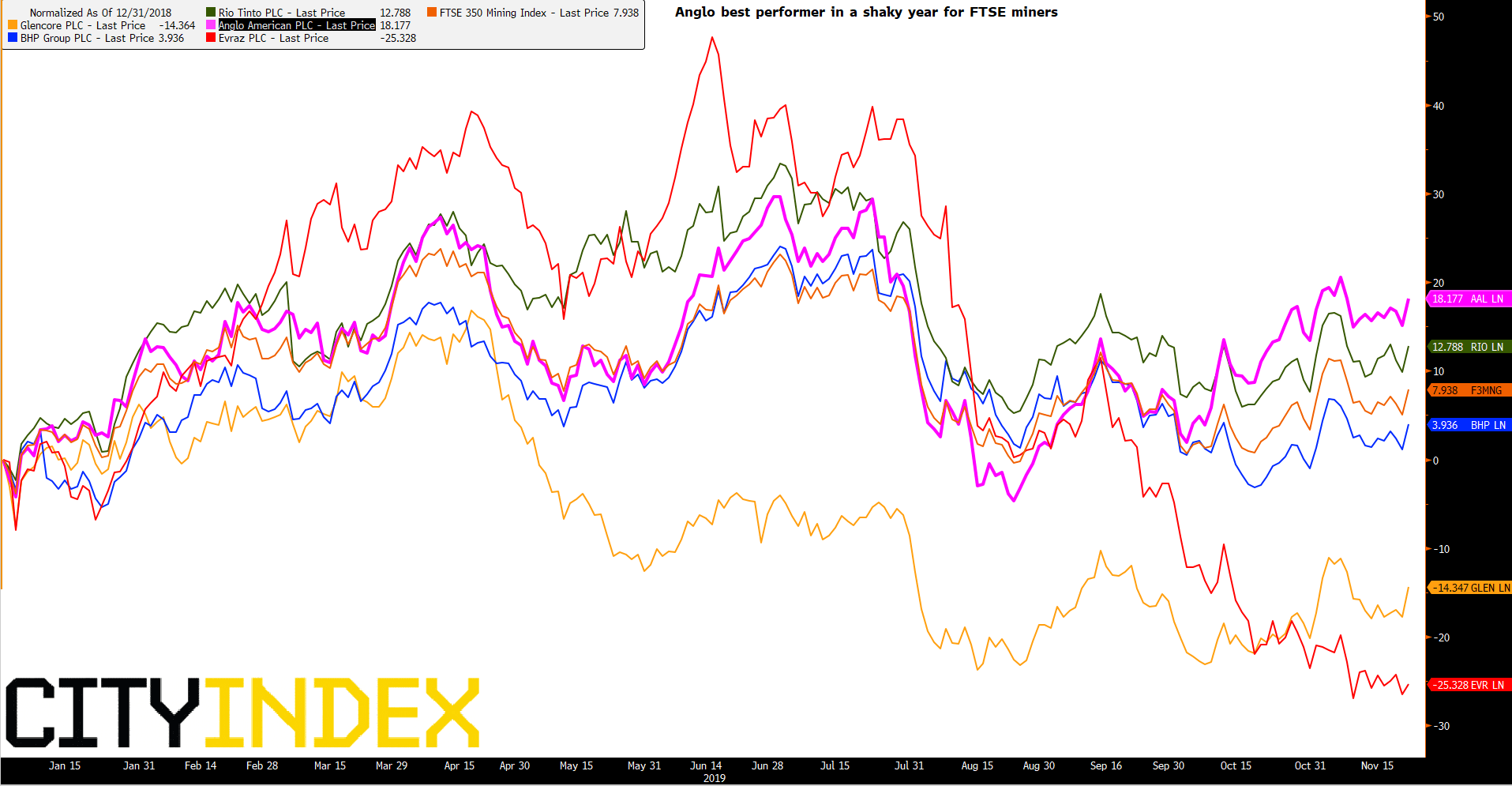

Sentiment is aptly demonstrated by the normalised chart of FTSE 100 miners below. The best performer in the year to date is Anglo American, standing 18% ahead on Friday. But it had been almost 30% higher in July. EVRAZ, the UK-listed Russian steel and mining firm gained about 50% into the mid-year only to erase the advance and slump to a 25% loss this week. Investors clearly aren’t expecting a demand recovery across metals in the near term.

Normalised: FTSE 100 mining stocks, year to date

Source: Bloomberg/City Index