Marks amp Spencer needs breakthrough in General Merchandise

Marks & Spencer will unveil final quarterly results for 2014 on Thursday 2nd April. It’s already clear 2014 was only marginally less of an annus […]

Marks & Spencer will unveil final quarterly results for 2014 on Thursday 2nd April. It’s already clear 2014 was only marginally less of an annus […]

Marks & Spencer will unveil final quarterly results for 2014 on Thursday 2nd April.

It’s already clear 2014 was only marginally less of an annus horribilis for Britain’s fifth-largest supermarket, as for its peers, Tesco, Morrison, Sainsbury and ASDA.

Supermarket sector investors have resigned themselves to marginal sales growth, if any, for years to come, at least judging by the 36% rise off October lows by the FTSE 350 Food & Drug Retailers Index.

As it happens, M&S was the only grocer to actually grow like-for-like food sales growth in each quarter in 2014.

But beyond that, growth was nothing to boast about, just 0.1% to 0.2% for much of the year.

For a retailer for which food contributes over half of group sales and about a third of profit, such a performance is precarious.

Symbolically, at least, this slim lead M&S has over its rivals is one part of its repertoire it needs to maintain in order to keep its stock travelling in the direction of a 40% rise since October.

The market wants to be reassured that M&S’s food product innovation, refinement of existing offers for thriftier times—e.g. ‘Dine in for Two’, andfocus on providing for special occasions, are continuing to pay off.

Analysts on average forecast fourth-quarter like-for-like sales will rise 0.3%, after +0.1%, in Q3.

M&S forecasts full-year food gross margin will rise by 0.1% to 0.3%.

General Merchandise is of course Marks’ second-largest segment, comprising clothing and home wares.

It’s in this business that M&S has felt the full force of a sweeping dive in retail sector growth, posting 14 consecutive quarters of declines, including a 5.8% fall in Q3.

The City forecasts the firm’s last 2014 quarter was better, especially as it was free of the unseasonal weather in October and November and disruption at an e-commerce distribution centre in December that weighed on Britain’s largest clothing retailer, in its third quarter.

A consensus of 10 analysts’ forecasts compiled by the company suggests the like-for-like fall in General Merchandise for Q4 was 1.2%—a relative recovery at least, if achieved.

The other major metrics the market will watch are below.

(Note: full-year results are officially scheduled for 20th May)

Any ‘misses’ compared to the above expectations will bring resumed mutterings in some quarters about CEO Mark Bolland.

Investors appear to be divided into two main camps over Bolland.

One lauds his inarguable success in reversing decades of under-investment, redesigning products, stores, logistics and M&S’s online presence, since being appointed in 2010.

The other queries if he’s still suitable, largely because his initiatives in clothing since 2012 have so far failed to deliver sustained growth.

There’s no sign that M&S’s board largely agrees with the latter view, though continued incremental improvements all round will keep the balance tilting in his favour.

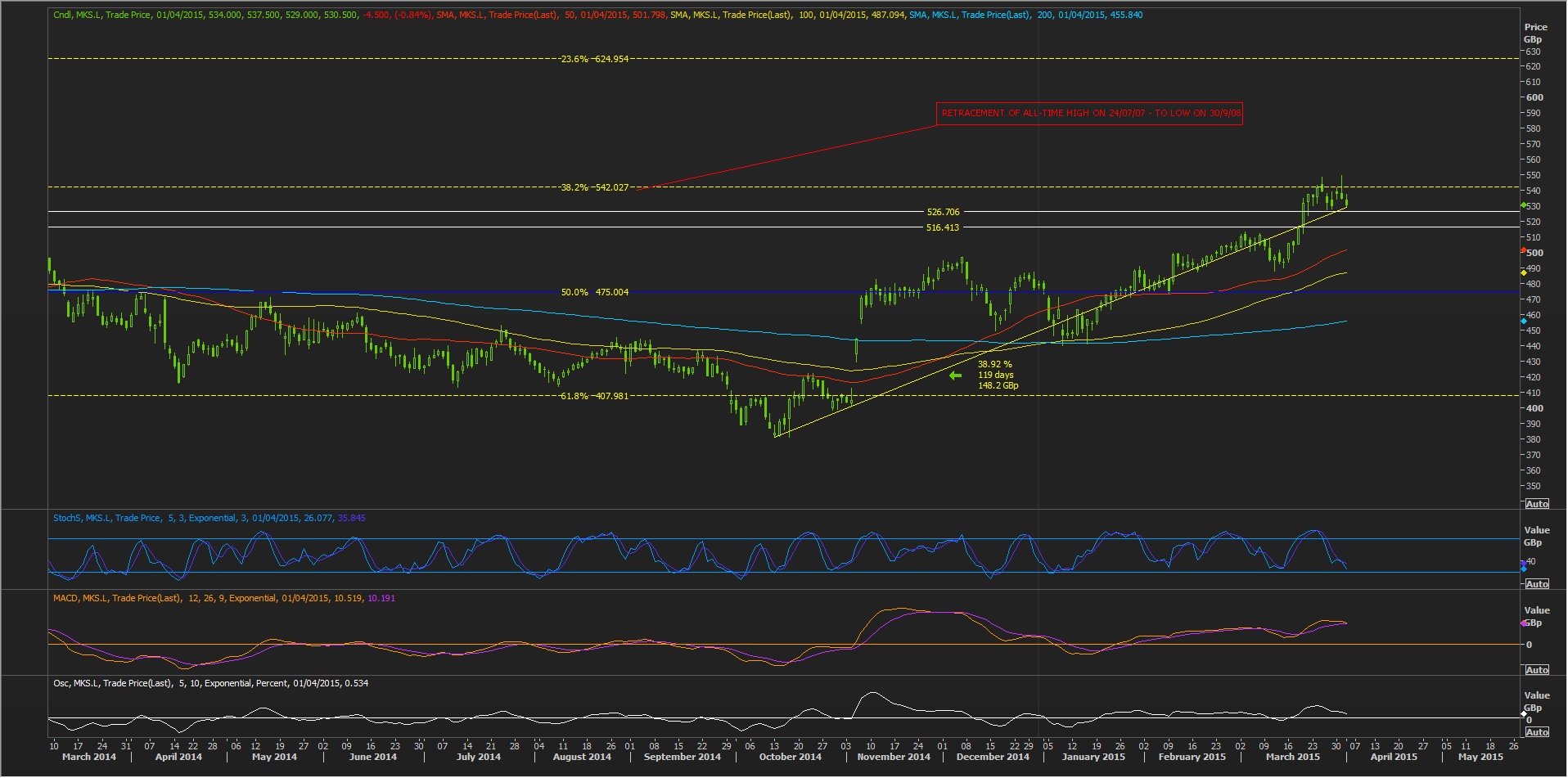

The same continued improvements could also embolden the market for another attempt to overcome a strong resistance level that recently gave M&S stock pause for thought.

It’s the retracement of 38.2% of the stock’s fall from the all-time closing high at 759p on 24th July 2007, to a low at 191.90 on 30th September 2008.

There are supports nearby, but daily momentum is currently slacking off, increasing the risk of a marked fall if tomorrow’s numbers are deemed unsatisfactory.