-

Risk aversion rises as French election 1st round less predictable

-

Hedging costs increase though Le Pen win still distant

-

Mélenchon’s run-off hopes improve

-

Complacency vs. the ‘undecided’

-

How Le Pen could win

The acceleration of support for the left-wing outsider in France’s general election, Jean-Luc Mélenchon, has jolted investors out of complacency over chances of a win by Eurosceptic Marine Le Pen, as shown by a jump in gauges of risk aversion.

- The spread between 10-year French sovereign debt yields and their German counterparts spiked to 72 basis points on Monday, a six week high

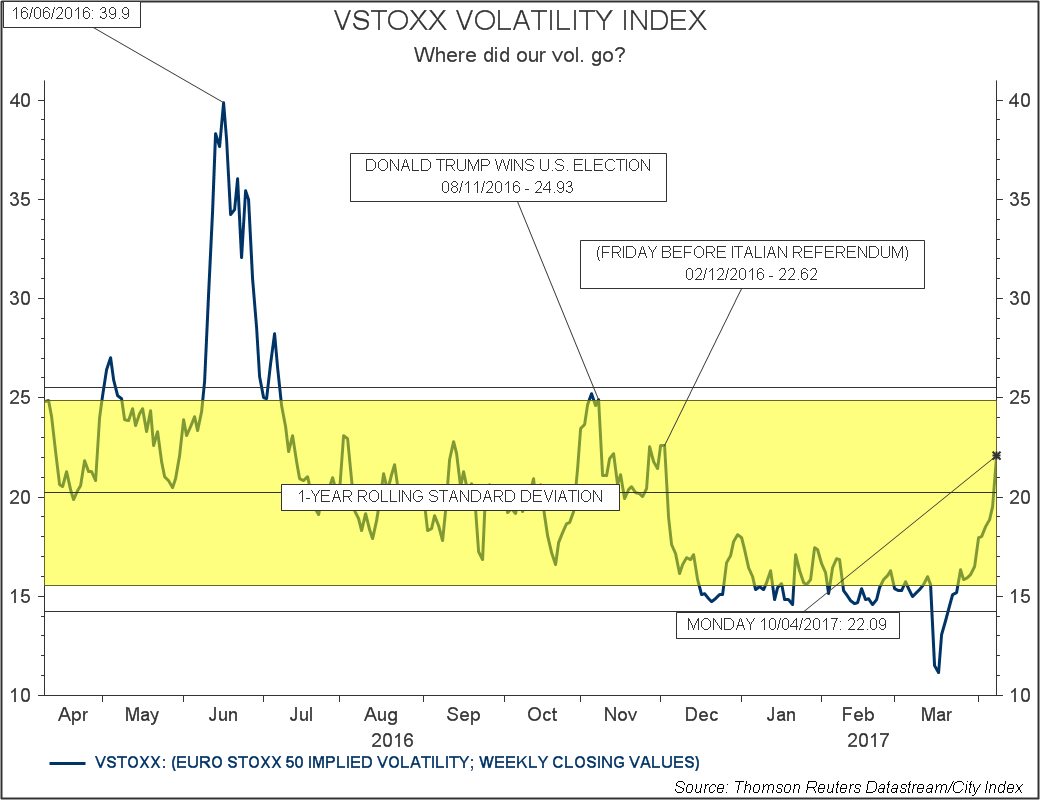

- VSTOXX, ‘Europe’s VIX’ (based on Euro STOXX 50 futures index) has also raced higher in recent sessions, closing in on readings seen slightly before Italy’s constitutional referendum in December, and up from near 2-year lows in March (figure 1)

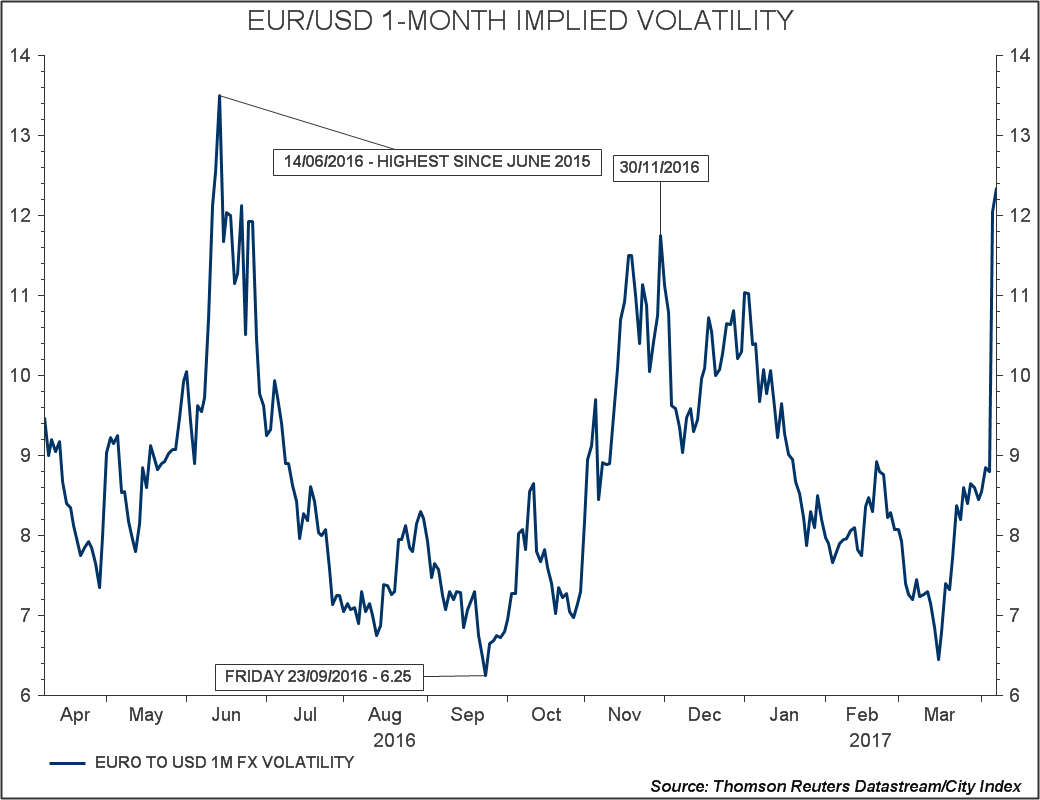

- Volatility implied by trading of one-month EUR/USD option contracts surged to the highest since late November from almost a 6-month low about three weeks ago (figure 2)

Figure 1

Figure 2

Mélenchon’s moment

With less than two weeks ago before first-round voting, this means investors are now faced with the choice of ramping up insurance against whipsaws at greater expense than a few weeks ago, or remaining relatively unguarded.

With polls continuing to point to a rejection of far-right candidate Marine Le Pen, it’s little wonder that financial markets have seemed complacent.

However, wider geopolitical events over the last few trading days have tilted investor perceptions of the need to hedge the French risk event.

It coincides with an advance in apparent support for Communist Party-endorsed Mélenchon. An IFOP poll on Monday showed his share of the 1st round vote could be 18%, one percentage point higher than late last week. Markets are also reacting to Le Pen re-establishing a thin 1st round lead against Macron in latest surveys. IFOP’s Monday afternoon survey gave Le Pen 24%, actually down half a point, but Macron fell by half a point more to 23%. Mélenchon’s share rose from 13.5% two weeks ago in Harris Interactive Polling to 17% by Thursday after TV audiences resoundingly found him to be the star performer of last week’s debate.

The beleaguered conservative Francois Fillon is still slipping, falling further from 20% late last week to 18.5% at the time of writing. For now, the main source of growth in Mélenchon’s vote largely appears to be the Socialist Party’s Benoît Hamon, who has faltered to 9%, below 10% for the first time since late January.

What hasn’t changed is the structure of projected second-round voting. 58% of support would go to Macron, and 42% to Le Pen in the run-off, according to IFOP data released on Monday evening. Even here though, markets have reason to be warier. Opinionway’s poll, out that morning, put the balance at 62%/38% for Macron. It is these recalibrating expectations—particularly the notion that Mélenchon could replace Macron in a run-off against Le Pen—that have finally spurred a rise in European risk aversion.

Indecision risks

Whilst still relatively implausible, chains of events that could install Le Pen as President grow more probable as Macron’s support is eroded, given an almost unprecedented pool of more than one third of voters who continue to say they are undecided.

That takes to us to the crux of persisting risks to European markets from a seemingly low-probability outcome. They will be upended more severely as the probability of the least desirable outcome rises. It is a conundrum when the market’s worst case scenario still seems distant, whilst at the same time markets failed to predict anti-establishment upsets last year. A secondary risk is that a scramble to take cover will be more costly and disorderly the later it is left.

Yet longer-term hedging markets remain subdued despite Monday’s spike in borrowing costs. One that is tied most directly to Le Pen’s intention to take France out of the Eurozone is the 5-year Credit Default Swap. It will pay out if France redenominates back into francs. At less than 54 basis points (bp) late on Monday, the CDS still implies less than a 2% chance of Frexit next year and about a 9% chance over 5 years. Neither term suggests much urgency amongst debt hedgers.

Indeed, the France/Germany benchmark yield spread itself is still nowhere near its 190bp divide in 2011, hit amid heightened Grexit risk. By late Monday, it had eased by two points to 70bp. Noting the 50bp differential in 2014 (pre-QE), the current spread suggests the bond market sees the probability of a Le Pen win at little more than 10%.

Granted, there are many ways that these impressions of how much the market cares could be wrong. Shorter-term protection buying, for instance, can be more telling (see EUR/USD implied volatility chart above). However signal-to-noise ratios deteriorate in more targeted hedging. Alternatively, what looks like under-priced risk may simply reflect sliding price elasticity of demand. After all, it’s been an expensive 10 months for hedging.

Rewriting Le Pen’s chances

More to the point, the market’s preferred candidate Emmanuel Macron last week passed another big test with flying colours. The En Marche! politician again belied his political inexperience during the second TV debate by scoring several political points against chief antagonist Le Pen.

That’s not to say a Le Pen victory is impossible. Assumptions of her defeat are based entirely on polling data—on which scepticism emerged after the Brexit vote and U.S. election. A potential ‘Shy voter’ effect, combined with a more dynamic view of second-round scenarios—when drop-out candidates can be expected to barter their support—suggests higher Le Pen risk. Ironically, we have little option but to use polling data and crowd-sourced variants to demonstrate alternative scenarios.

Our speculative deductions have a more than evens probability of being disproved. Still likeliest scenarios for a Le Pen win are outlined below.

- The Gaullist Eurosceptic, Nicolas Dupont-Aignan, who might win 3% of the vote, according to IFOP, was at pains to outdo Le Pen on nationalist credentials in the second TV debate. He is likely to voice support for Le Pen, if for anyone. IFOP already places 84% of his voters as close in sentiment to Le Pen

- The far-left candidates Nathalie Arthaud and Philippe Poutou each recently had around 0.5% of the vote, and IFOP judges that 19% of the far-left electorate would ally with Le Pen. That suggest a low transfer of fractional support—a cautious assumption might be 0.25%

- We may also assume Mélenchon voters who say they would not vote for Le Pen (recently 5%, according to IFOP) include some who would. Again, conservatively, let’s assume another 0.25%—and even that looks stretched if the sharp rise in Le Pen’s blue-collar support has maxed out

- We’re probably on safer ground in supposing that more of the c. 5% vote for Fillon that currently denies second-round Le Pen support, would in fact largely veer towards Front National

Under these ultra-cautious scenarios, Pen hits more than 50%, even without the unpredictable alliances that ‘soft Eurosceptic’ Mélenchon might forge.

We can see how the Front National candidate could get close to, though would remain below Macron’s current 58% assessment, which itself is likely to rise, should he progress to the run-off.

As per Donald Trump and Brexit though, her opponents and markets should be more concerned that higher levels of commitment among her confirmed support, together with an unusually high ‘free-floating’ electorate, may again combine to increase the chances of a result that appears improbable.

To be sure, severe market dislocations if Le Pen approaches victory or even clinches it, will probably correct themselves quickly, as they did after Brexit, the U.S. election and Italy’s referendum.

Even so, a short-lived rise of the spread between French and German 10-year bonds towards 190 basis points, or higher, in a panic scenario would still be hazardous, as would a 5% or more slide of the euro, and 10%-15% hits to major European stock indices. All are foreseen by major investors if markets’ least expected scenario happens (again).

{kind=link}