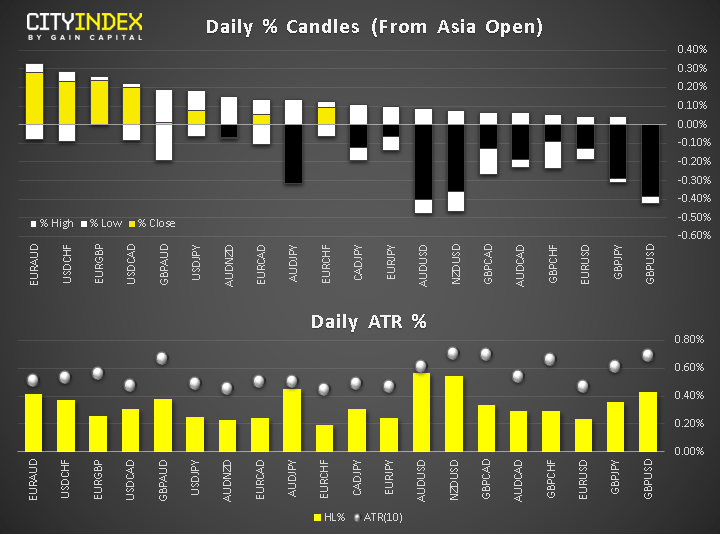

- FX snapshot: As US investors come to the fray, USD is the strongest on the back of positive US data while GBP is among the weakest.

- Data recap: US GDP came in at +2.1% compared to +1.8% expected - the dollar jumped on the back of this. Meanwhile other US macro pointers were also not too bad, further reducing the odds for a large rate cut next week: Core PCE (Q/Q): 1.8% vs. 2.0% expected; Personal Consumption 4.3% vs. 4.0% expected, and GDP Price Index Q2 2.4% vs. 2.0% expected. German Import Prices -1.4% m/m vs. -0.8% expected. Meanwhile once again ECB trimmed its Eurozone growth forecasts to 1.3% for 2020, but kept unchanged its 2019 and 2021 estimates at 1.2% and 1.4% respectively.

- Stocks were mixed in Europe after yesterday’s sell-off, but the overall positive tone from mostly positive earnings kept the bears at bay. Futures pointed to a positive start on Wall Street.

- Earnings galore: big tech companies reported mostly better than expected numbers last night and in Europe Vodafone stole the show with its well-received earnings. Alphabet reported revenue that beat expectations and announced its biggest stock buyback in history - $25 billion worth of stock, no less. Meanwhile, Intel, which also beat profit estimates, agreed to sell the majority of its smartphone-chip business to Apple – the deal is valued at $1 billion. However, Amazon results disappointed investors as costs went up because of its one-day delivery service. Today, Twitter results showed revenue of $841.4 billion (higher than $828.49M expected), with and adjusted EPS of $0.05 (which was below $0.19 expected) – but shares rose as magnetisable Daily Active Users Beat Expectations. McDonald's EPS was in line at $2.05 with sales +5.7% vs. +4.4% expected.

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM