Market Review amp Outlook Stimulus Talk Moves Markets

Stimulus Talk Moves Markets With central banks in renewed stimulus mode and market concerns over Brexit consequences having increasingly faded into the background, this past […]

Stimulus Talk Moves Markets With central banks in renewed stimulus mode and market concerns over Brexit consequences having increasingly faded into the background, this past […]

Stimulus Talk Moves Markets

With central banks in renewed stimulus mode and market concerns over Brexit consequences having increasingly faded into the background, this past week has largely been one of expanded risk appetite for global financial markets.

Stocks surged as yield-seeking investors bid up US equity markets to uncharted territory, with both the Dow Jones Industrial Average and S&P 500 reaching progressively higher all-time highs throughout the week. European stock markets also continued to rise, as did Japan’s Nikkei index. Meanwhile, traditional safe haven assets like gold and the Japanese yen retreated sharply as safety took a back seat to the pursuit of yield.

While the Bank of England (BoE) unexpectedly opted for inaction on Thursday, refraining from cutting interest rates and declining to implement a new round of stimulus measures, the central bank did state that “most members of the committee expect monetary policy to be loosened in August.” Though this was far from a guarantee, the statement did serve to indicate that the BoE does indeed have intentions to ease policy at its next available opportunity. At first, a rapid short squeeze for the beleaguered British pound occurred, along with a pullback for equities, as news of BoE inaction surprised the markets. With assurances of near-term easing measures, however, sterling quickly pared its gains and stocks continued to rally.

Pivoting to Asia, a sharp pullback for the Japanese yen and a surge for Japan’s Nikkei index occurred this past week on a resurgence of support for Japanese Prime Minister Shinzo Abe’s brand of economic stimulus after his party’s landslide political victory last weekend. As a result, the Prime Minister’s Abenomics policies gained renewed strength, and further stimulus measures were announced. Not only did this lead to a surge in Japanese stocks, the news helped further boost global equities, most notably US indexes as they reached for new record highs.

Looking forward, the big question remains as to how the central bank policies of the UK, Japan, as well as the persistently dovish ECB, may or may not affect the US Federal Reserve and, in turn, the US dollar and global equity markets. The market’s view of the probability of a Fed interest rate hike this year has plunged since the Brexit outcome. In the weeks since the UK’s EU referendum, however, concerns over Brexit consequences have faded, and US economic data releases since then have shown better-than-expected indications of the US economy. This included the highly-positive non-farm payrolls employment numbers for June, weeks of lower jobless claims, the producer price index coming in at its highest increase in a year, and retail sales numbers on Friday far exceeding expectations.

When such positive numbers are coupled with declining Brexit worries and a US stock market that has been rallying to record highs, it seems that another interest rate hike by the Federal Reserve may perhaps be closer than previously anticipated. At the same time, however, the Fed will likely be exercising much caution, especially in light of other major central banks being in relatively strong easing mode. Therefore, while there could very well be at least one Fed rate hike this year, especially if economic data and equity markets continue to cooperate, the likelihood is that this will not happen at least until September, or perhaps December. If there are any surprises before then, though, the dollar could see a major surge while stocks could be pressured to retreat significantly from their highs.

Technical Developments

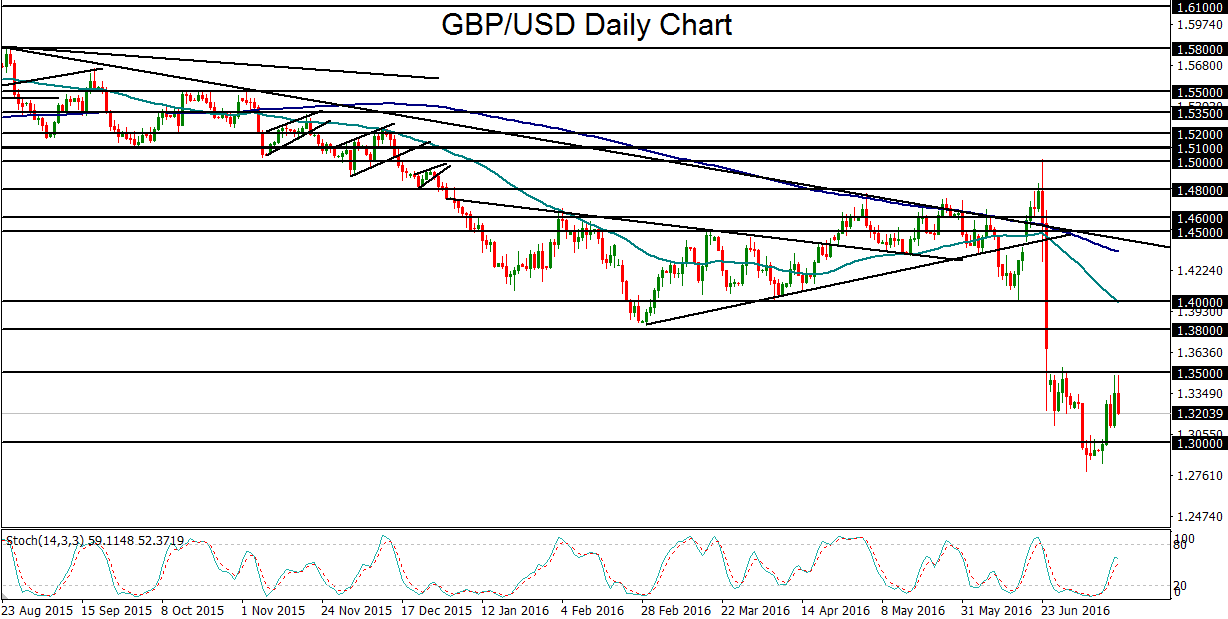

GBP/USD

If the Bank of England is giving strong indications of monetary policy easing next month and the Federal Reserve continues to be provided with evidence of an improving economy and rising inflation to support a near-term interest rate hike, conditions could soon be ripe for a further continuation of pressure on GBP/USD. Although the knee-jerk rise for sterling on Thursday was reasonable considering the BoE’s inaction, the prospect of a near future UK rate cut coupled with an increasing foundation for a Fed rate hike could easily push GBP/USD back on its downward spiral. Thursday’s surge brought the currency pair back up to approach key resistance around the 1.3500 level before quickly paring its gains. If price is able to stay below 1.3500, it would be a strong bearish indication, in which case all eyes should revert back to the 1.3000 psychological support level. Any sustained breakdown below 1.3000 could put GBP/USD on track once again to begin targeting significantly further downside around the 1.2500 objective.

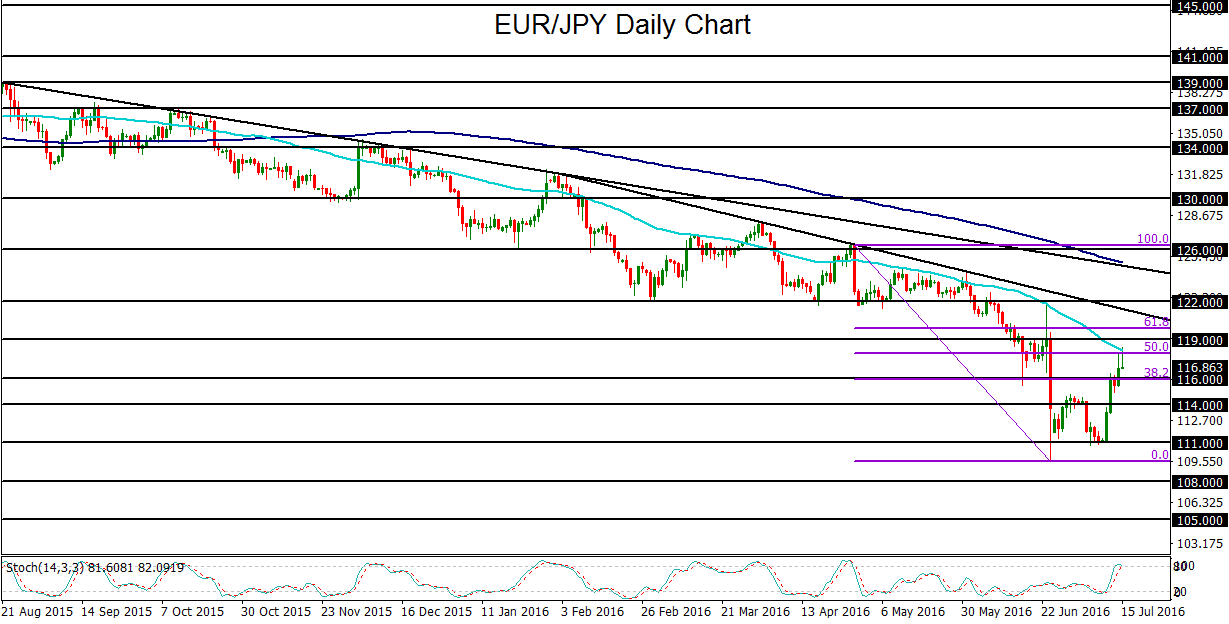

EUR/JPY

A sharp pullback for the Japanese yen occurred this past week that led to a strong rebound for EUR/JPY, lifting the currency pair from near its multi-year lows around 111.00 support to break out above key resistance around the 116.00 level. A few weeks ago, this 116.00 level was broken down decisively in the immediate aftermath of June’s Brexit vote, as the euro plunged while safe haven flows boosted the yen. That June plunge was followed by a quick bounce and then a return back down to the 111.00-area support lows before the sharp rebound this week. Having broken out above 116.00, EUR/JPY has made a key move. With the previously acute concerns over Brexit consequences having faded substantially in the weeks since the historic EU referendum, the euro has begun to stabilize and the safe haven appeal of the yen has declined markedly. With the promised implementation of more Japanese stimulus measures, the yen could continue to retreat, potentially pushing EUR/JPY towards a further recovery. As noted, the 116.00 level represented a key technical area. If this week’s strong break above this level is sustained, the next major upside targets are at the key 119.00 and then 122.00 resistance levels.

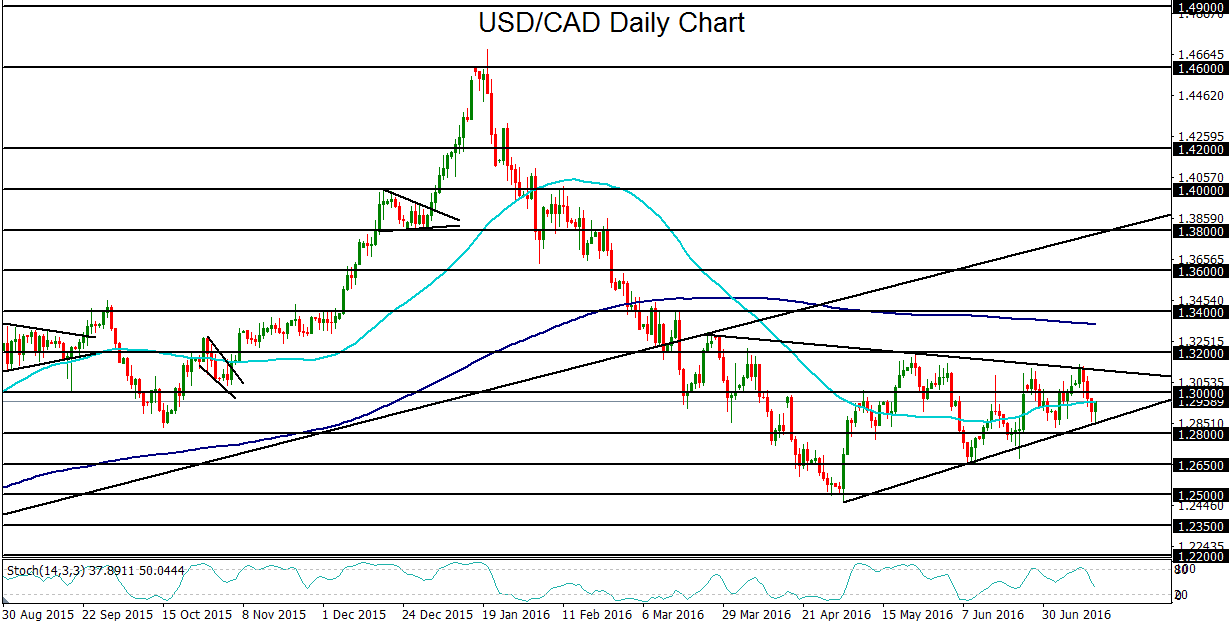

USD/CAD

This past week, USD/CAD fell after the Bank of Canada (BoC) kept interest rates unchanged at 0.50% as expected and then went on to issue a statement that was less dovish than many had anticipated. The policy statement helped prompt a surge for the Canadian dollar, pushing USD/CAD below key 1.3000 support. The currency pair continued to follow through to the downside on Thursday to approach the lower support border of a large triangle consolidation pattern that has been in place since the 1.2500-area lows in early May. Aside from the BoC policy statement, also contributing to a slightly higher Canadian dollar and lower USD/CAD has been crude oil, which has remained relatively well-supported despite having drifted down within the past month from early-June highs. Having approached the bottom support of the large triangle pattern, USD/CAD has reached a critical technical juncture. Any sustained breakdown below the lower border would confirm the triangle as a downtrend continuation pattern, indicating a potential resumption of the sharp bearish trend that started in the beginning of the year. In the event of a breakdown below the triangle pattern, the next major downside target is at the key 1.2650 support level followed by the noted 1.2500 support level, which was last touched in early May and represents the low of this year’s bearish trend.

{kind=link}