Stock market snapshot as of [5/12/2019 2:28 pm]

- Instigators of a Grinch sell-off are again being outflanked by the Santa rally’s advance guard. Metaphorically, these opposing forces are being led by the same person. For weeks, Donald Trump’s assessments of talks with China have demonstrably been the last word for day-to-day market direction. Since his claim a day ago that they are going “very well”, he’s had little else to say about the discussions. By contrast, China’s Commerce Ministry was rather non-committal on Thursday: “China believes if both sides reach a phase-one agreement, relevant tariffs must be lowered”. Going “very well” and lower tariffs as a condition is all we know for sure. All the elements seem to be in place for another volatility spike. We’re just waiting for the next word from Santa Grinch

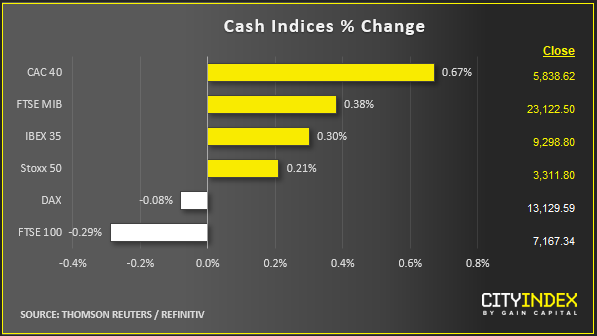

- Meanwhile, major stock markets are almost all higher. Britain’s FTSE 100 is an exception as the pound jumps, leaving the exporter-led market weak. And Germany’s DAX barely gained before slipping under the weight of industrial and consumer shares. German factory orders data showed demand down 0.4% in October, the mirror image of estimates eyeing a 0.4% gain

- U.S. indices are taking the baton from firm futures, trampling over a relapsed VIX. The (no) ‘fear gauge’ is set for a second session in the red after on Tuesday completing its only four-session stretch of gains since July

- Japan Prime Minister Shinzo Abe’s ¥26 trillion fiscal stimulus package left JGB yields little changed and Nikkei 225 futures up just 0.3%. The package is in line with expectations whilst details of the fresh bond issuance are less impressive than the headlines

- U.S. benchmark yields are barely moving, with the 10-year up 1 basis point at last check to 1.78%. EU yields tick lower

- Brent crude extends Wednesday’s bounce on inventory relief as OPEC/OPEC+ begins a two-day meeting. Saudi has offered the carrot of its own deeper cuts if lesser members make greater efforts to comply with current limits. The stick isn’t specified

Stocks/sectors on the move

- EU stocks: Apart from the FTSE, Germany’s DAX is the other European high-capitalisation index that’s underperforming. Heavyweight Siemens and BASF are responsible much of the index dip. Consumer products maker Beiersdorf also responds to disappointing factory gate data. Luxury minnow Moncler’s rather academic rejoinder to takeover reports citing Kering is that “no concrete hypothesis is under consideration”. The stock is up about 8%

- UK stocks: Aston Martin accelerates as much as 13% after a possible bid was reported by magazine Autocar. Battered shares of home ware retailer Dunelm jump 15% on a pre-tax profit forecast upgrade. Ted Baker extends a recent decline by 4.6%. It’s appointed a consultancy to review operations after three profit warnings and last week’s disclosure of an inventory overstatement. Online rival boohoo.com falls a similar amount. The co-founders are selling 50 million shares

- U.S. stocks: Kroger adds to retail industry woes with an adjusted Q3 EPS miss. The stock retreats 2%. Tiffany & Co, after recently agreeing to be acquired by LVMH, reported weak profits; shares fell around 1%

FX snapshot as of [5/12/2019 2:32 pm]

View our guide on how to interpret the FX Dashboard

FX markets and gold

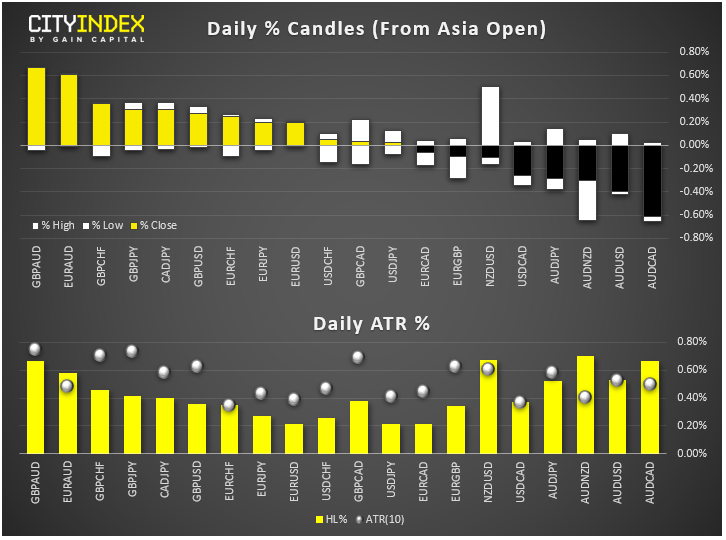

- The Kiwi is the biggest mover again, reaching a four-month high after Reserve Bank Governor Orr said policy was in a “hold phase”. NZD/USD has gained about 1.7% in six days to stand last at 0.65234

- The Aussie slipped 0.3%, losing an initial 0.1% gain following Tuesday’s RBA hold. Retail sales were flat in October

- It’s day five of the dollar slide, the longest losing streak for about a month. Even so, safe havens are still weak vs. greenback, to characterise prevailing appetite as firmly one that is open to risk

- The pound seems to know no bounds. Sterling is up two big figures in two sessions to around $1.314. Election certainty is very much bounded though, considering how unreliable poll indications have been in recent years. Right now they’re pointing more firmly to a Conservative majority in next week’s UK election

- BOC’s hawkish hold a day ago keeps the loon among better performers

- Indian assets also sees some action after the RBI unexpectedly paused rate cuts, despite reducing 2019 growth forecasts. The rupee jumped the most in a session since last month. Bond yields spiked the highest since September, though stocks edged lower

Upcoming economic highlights

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM