View our guide on how to interpret the FX Dashboard

FX Brief:

- Global growth bears have more to cheer about on the back of weak data from Asia.

- South Korean exports hit a 4-year low and contracted for an 11th consecutive month at -14.7% YoY. CPI was stagnant at 0% YoY, although above last month’s 30-year low of -0.3%.

- Japans final manufacturing PMI was lowered to 45.4 from 48.5 prior (below 50 denotes contraction) whilst Austrian manufacturing slowed to 51.6 from 54.7 prior. Producer prices were also lower, coming in at 1.6% YoY vs 2% prior.

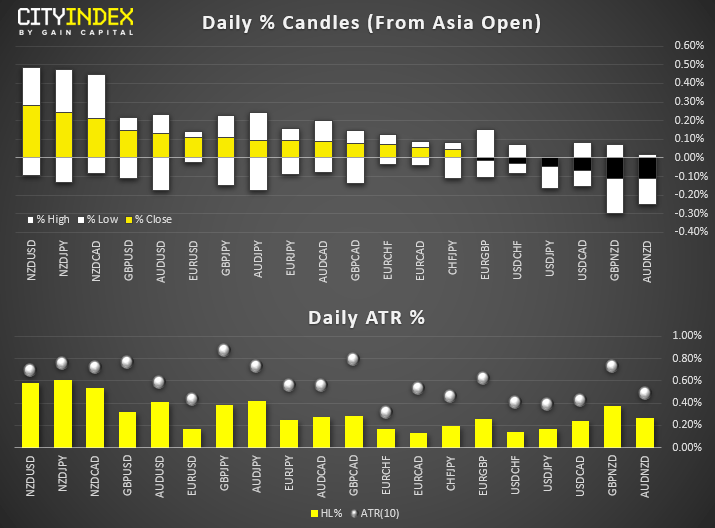

- The USD remained under pressure for a third session and is weaker against its peers. NZD, GBP and AUD are the strongest majors. NZD/USD hit a marginal 7-week high and USD/CHF and USD/JPY teased yesterday’s lows.

- Volatility remains contained, with all 20 pairs monitored remaining within their 10-day ATR. Although the average range of ATR is 50%, so above the usual 30% we’ve become accustomed to in recent sessions.

Equity Brief:

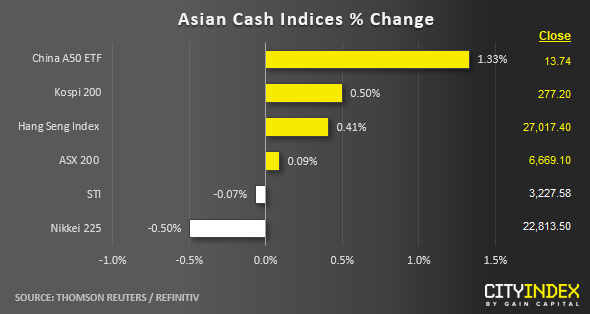

- A better than expected Caixin China Manufacturing PMI for Oct (51.7 versus consensus estimate of 51.0) has helped to offset a negative trade related news flow reported yesterday that cited unnamed Chinese officials airing doubts whether a comprehensive long-term U.S-China trade deal is possible. The latest reading of the Caixin PMI has pointed to the strongest pace of expansion in the manufacturing sector since Feb 2017.

- China A50 has rallied by 1.33% to hit a 5-day high follow by South Korea’s Kospi 200 and Hong Kong’s Hang Seng Index that have gained by 0.51% and 0.41% respectively.

- Hong Kong stocks have shrugged off the negative impact caused by the 5-month long of streets protests that saw its economy entered to a technical recession for the first time since 2009. Flash estimates for Q3 GDP shrank by -3.2% q/q from -0.5 q/q recorded in Q2. Also, China government has vowed to bolster Hong Kong’s national security laws to clamp down on the on-going street protests that may backfire as such actions may incite more defiance behaviour from the protestors.

- Japan’s Nikkei 225 is not showing much optimism today as it has shed by -0.50% dragged down by a stronger JPY where the USD/JPY has dropped to a 3-week low of 107.90 in today’s Asia session. The under performers are export-oriented and cyclical sectors; Automaker Subaru declined by -1.0% while electronic device maker Kyocera and optical equipment maker Olympus tumbled by around 3%.

- The S&P 500 E-mini futures has inched higher from yesterday’s U.S. session low of 3020 to record a modest gain of 0.28% and printed a current intraday high of 3044 in today’s Asia session.

Up Next:

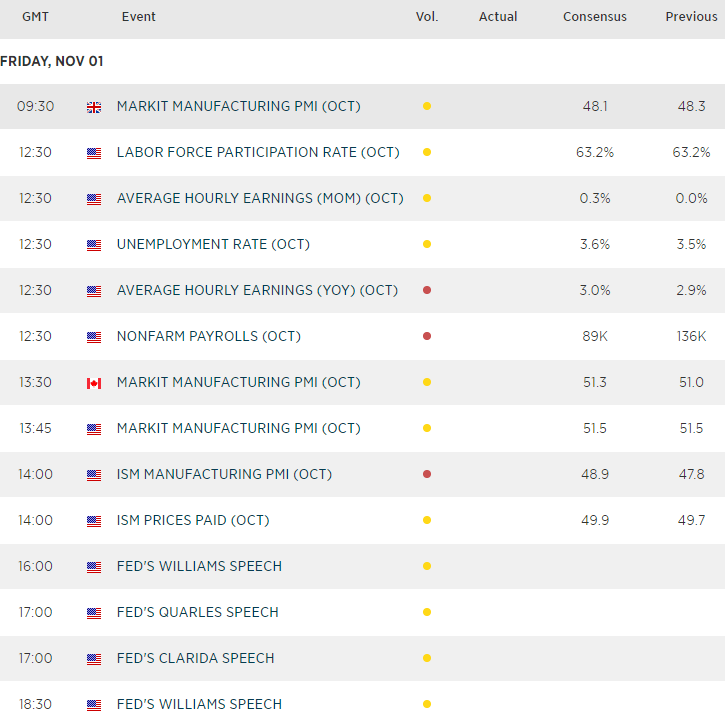

- Today’s NFP report is the main event in today’s calendar. Whilst unemployment is its lowest since the swinging 60’s, job growth is expected to 89k from 136k prior and all eyes are on hourly earnings after it fell to 2.9%, its sharpest monthly drop in 11-months. And with USD at a make or break point, it could make for an interesting weekly close for several major currencies.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM