View our guide on how to interpret the FX Dashboard

FX Brief:

- The US House voted to reign in Donald Trump’s military action against Iran, with the resolution passing along party lines at 224-194. This means Trump can no longer use US armed forces against Iran without consent from Congress.

- Trump reconfirmed that the “phase one” trade deal will be singed on 15th January, after China confirmed yesterday that Premier Li will be in Washington to sign. Trump also suggested that “phase two” could be signed after the election, although talks are to begin “right away”. That’s another 10 months of talking about phase two….

- Japanese household spending fell -2% YoY (-1.8% expected) although gained +2.6% in the month of November (-11.5% prior). With the sales tax hike and consumer reaction now out of the way, policy makers will be closely watching spending habits to see if the tax hike negatively impacts growth potential (which makes it a proxy for future stimulus).

- Australian retail sales beat expectation in November, rising 0.9% versus 0.4% executed and 0% previously. All thanks to Black Monday sales. Which could well pave the way for disappointing Christmas sales.

Price Action:

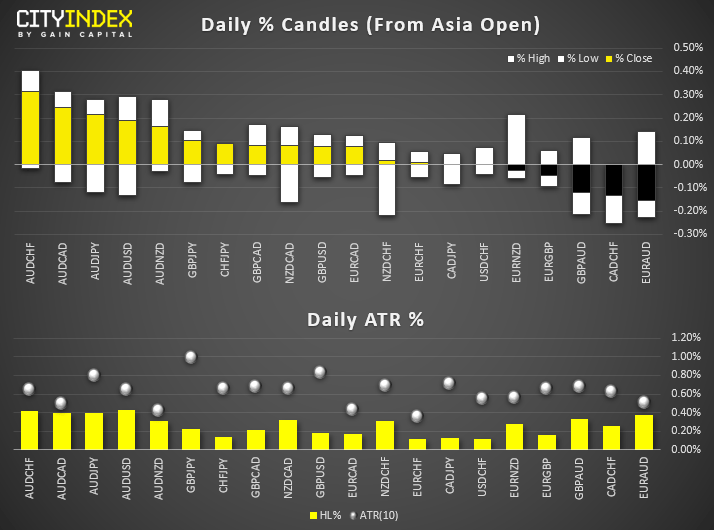

- USD/JPY remains anchored to yesterday’s bullish highs, with 109.73 resistance nearby. Given this key level held through December, it will be a clear line in the sand for bulls to overcome, if NFP data and risk sentiment allows.

- CAD/JPY hovers just below 83.90 resistance, where CAD bulls are looking for unemployment to revert to 5.8% and print around 25k jobs to label last month’s dire numbers an outlier. However, a clear break above 84.0 may be the better benchmark for a successful breakout. If we see another miss, expect prices to roll over, especially if we have weaker oil prices.

- A small doji candle formed yesterday to suggest downside momentum is waning for EUR/USD. A break above 1.1120 confirms the near-term reversal candle.

Equities Brief:

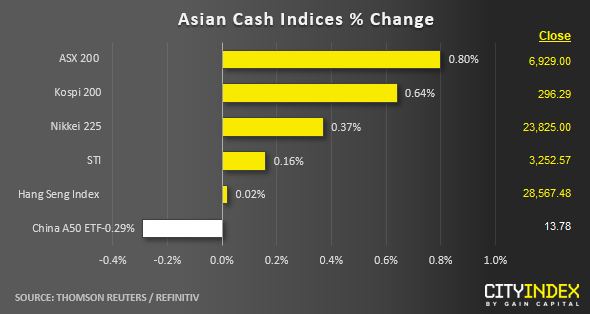

- Asian stock markets have managed to hold onto their earlier gains in place yesterday reinforced by a positive performance seen overnight in the U.S market where all three major indices (S&P 500, Nasdaq 100 & Dow Jones Industrial Average) have recorded another fresh all-time highs respectively.

- Today’s top performer so far is Australia’s ASX 200 where its has surged by 0.80% as it has staged a bullish breakout above a key technical level of 6880/90 led by healthcare and consumer non-cyclicals stocks.

- South Korea’s Kospi 200 has continued to rally led by semiconductor stocks on the backdrop of positive risk appetite. Samsung Electronics have added on to its gains this week and rallied by 0.85% today to print a fresh all-high level of 59,700 on an intraday basis.

Price Acton (derived from CFD indices):

- US SP 500: Pushed up as expected to print an intraday high of 3275 in yesterday’s 09 Jan U.S. session. In today, 10 Jan Asian session, the Index has continued to rally and staged a challenge on the 3280 medium-term pivotal resistance (printed an intraday high of 3283 so far). Short-term uptrend remains intact, watch the 3260 key short-term support for now (former swing high of 03 Jan 2020 and 23.6% Fibonacci retracement of the on-going up move from 08 Jan 2020 low of 3181) for a further potential push up to target 3300 next (psychological & Fibonacci expansion cluster).

- Japan 225: Short-term upside momentum remains intact with key short-term support to watch at 23600 (former minor swing high areas of 07/09 Jan 2020) for a further potential push up to retest the 24200/400 major range resistance in place since 23 Jan 2018.

- Hong Kong 50: Still below 29000 major resistance (the descending trendline from its all-time high level of 33530 printed on 29 Jan 2018 that has capped previous rebound). Watch the short-term support at 28445 for today and a break below it sees a slide towards 28100 and 27900 (the former swing high area of 07 Nov 2019 that has managed to hold on 08 Jan after the outbreak of the Iran strikes on U.S. bases in Iraq).

- Australia 200: Bullish breakout above the 6880/90 previous current all-time high level. Right now, a daily close above 6890 reinforces the start of a potential impulsive upleg sequence to target 7040 next in the first step.

- Germany 30: Eyeing to break above 13600 current all-time high level while the broader based STOXX 600 has hit a fresh al-time high yesterday, no clear signs of bullish exhaustion. Watch key short-term support now at 13450/370 (the former range resistance from 19 Nov 2019) for a further potential push up to target 13750 next in the first step.

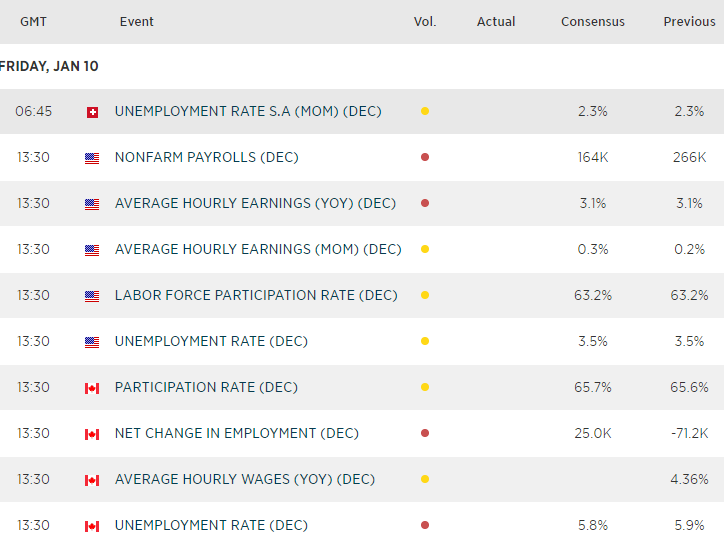

NFP Preview: Mixed Report Expected, Stationary Fed May Limit Market Reaction

USD/CAD In The Crossfire Of Today's Employment Reports

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 08:15 AM

Latest Dollar articles

Yesterday 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM