- A ‘limited’ trade deal between US and Japan has been signed by Trump and Abe, which cuts tariffs on US farm goods and Japanese machine tools. The move is expected to open-up around $7 billion of US exports to Japan, and Trump has reassured Abe that the US won’t impose the ‘section 232’ national security tariffs on Japanese cars and auto parts.

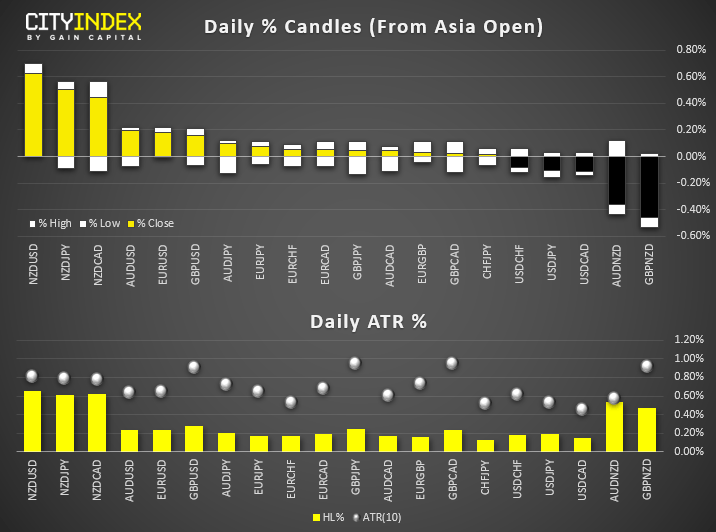

RBNZ Governor Orr hit the wires, saying rates are to remain low “for a number of years” and they’re unlikely to need unconventional policy tools. This follows on from similar comments from RBA’s Governor Lowe, who said in a speech that whilst they doubt they’ll use QE, they know how to use it if they have to. - Orr’s QE comment helped lift NZD which is today’s strongest major. NZD/JPY, NZD/USD and NZD/CAD are the biggest gainers and close to reaching their typical daily ranges. AUD/NZD and GBP/NZD are the day’s biggest losers.

- USD trades lower for the session, with DXY in a narrow range just off yesterday’s breakout highs. EUR/USD has pared losses yet remain firmly below 1.10. GBP/USD remains trapped below 1.24 and trades just off-of yesterday’s lows which closed below key support.

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Equity Brief:

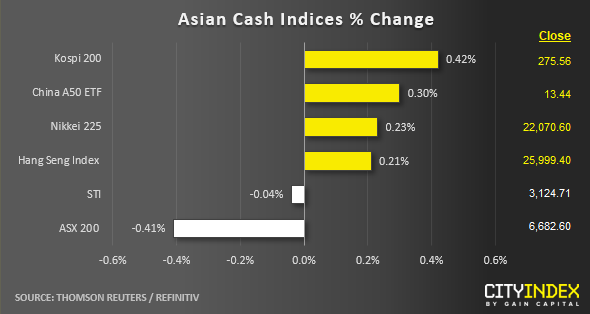

- Asian equities gapped higher and took Wall Street’s lead initially, although most have pared gain as they attempt to fill said gaps. The US-Japan trade agreement hasn’t filtered through to sentiment, which is probably due to it ‘limited’ status with no solid agreement over autos.

- The ASX200 has fallen to a 5-day low, led by the communication services, utility and health care sector. Gold road, Silverlake, Newcrest and North Star (gold miners) are currently the four largest decliners, taking their bearish lead from lower gold prices overnight.

- US futures are tickling slightly lower, yet structurally the cash indices look supported after rebounding off of key support levels overnight.

Up Next

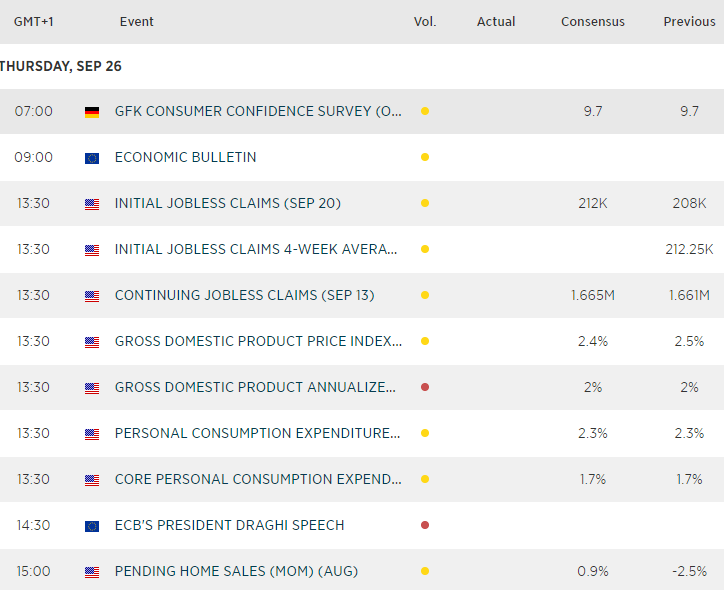

- No major economic data points, although a few central bankers will hit the wires.

- President Draghi speaks at 14:30 GMT at a conference in Frankfurt (along with other EU central bankers) although we’re not expecting fireworks with this one.

- German GkF consumer confidence is expected to hold steadily optimistic at 9.7, although the index appears to have topped in 2017 and traders are more alarmed with the negative sentiment among German businesses. Still, a notably deterioration in consumer sentiment will be seen as the final nail in the coffin for their economy.

- US Final GDP is unlikely to deviate too far away from the prior two reads, although expect carnage for the USD if it is revised heavily lower. Jobless claims warrants a look after hitting fresh multi-decade lows but, again we’d need to see a notable miss for it to impact markets.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM