Stock market snapshot as of [9/8/2019 4:06 PM]

- After a week like this, it would be a big ask to go into Friday’s close with no trepidation about the FX and futures open on Sunday night. (Nobody really loves a gap!) Hence, caution is prevailing and the more sure-footed tone of stock markets in the middle of the week is morphing into a retreat to the side lines

- Continued negative geopolitical events add another nudge to reduce risk. Italy’s deputy Prime Minister Matteo Salvini has finally pulled the trigger on a long-speculated snap election, aiming to capitalise on advantageous polling figures that suggest his Northern League party could win a vote without support from coalition partner 5 Star, with whom relations have deteriorated.

- Italy’s notoriously volatile BTP government bonds have duly cratered and yields have surged. At 1.79%, the 10-year BTP’s yield is well below the almost 3.7% touched last October. But Friday’s move of some 28.5 basis points is the biggest one-day jump since May 2018

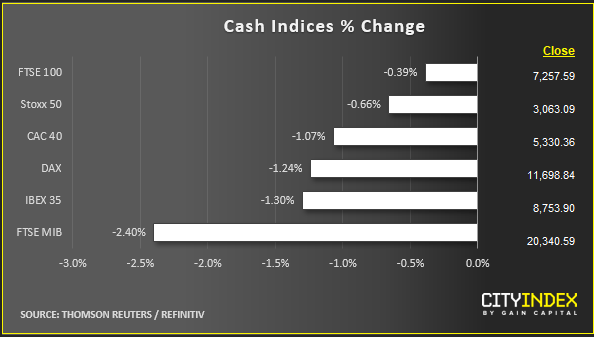

- Italian stocks, led by banks have slumped, again, in line with the usual pattern of reactions to disquiet in Rome. Shares of lenders in the rest of Europe have also turned tail to lead the Continent’s broader markets lower

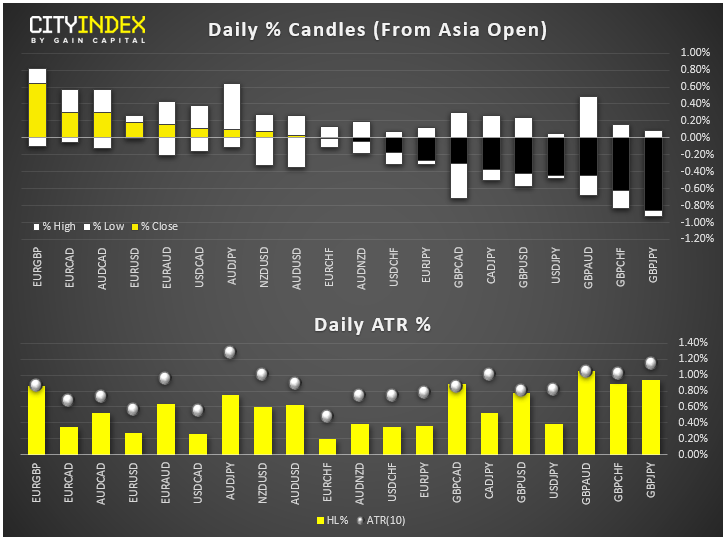

- A shock contraction of the British economy also appears to be echoing more broadly. If the 0.2% fall in second quarter UK GDP (compared to the flat reading expected) is just for starters as to the consequences of pre-Brexit stasis, then the European region is just as much in for a degree of further fallout out down the line. There are one-off factors that could see growth rebound in Q3, but even then it’s likely to be anaemic. Sterling isn’t waiting; it sets the latest in a recent string of fresh cycle lows, touching $1.2056 on Friday, for the first time since January 2017

- As for U.S.-China trade, the latest twist is that Washington has floated the idea of not relicensing U.S. firms to do business with Huawei after all. Reports say the Commerce Department has vetted the 50 license requests received from suppliers and customers of China’s telecom hardware giant, but decisions, which were supposed to have been made by now, are still pending

- Sensitive currencies reacted; like the Aussie dollar, which fell, and the haven yen, which rose. The yuan inched further below the threshold Chinese authorities had previously prevented it from depreciating to. Offshore-traded CNH last stood at 7.0807 to the dollar, holding sharply lower after collapsing at the start of the week

- Wall Street is on the back foot led by the tech-heavy Nasdaq

Stocks/sectors on the move

- European sectors losing most are almost the inverse of those that roared higher a day before on forlorn geopolitical hopes. Technology is worst hit though banks are close behind with an almost 1% fall for the STOXX super sector index. Materials, including China-sensitive metal mining and steel shares follow, down 0.9%. The Automobiles & Parts sub-sector plunges 2.2%, the worst industrial segment performance, with Banks sliding 1.7%. Italy’s UniCredit and Intesa San Paolo, tumble 6% and 4%

- WPP becomes one of a handful of outright large-cap earnings season success stories, with better-than-expected underlying revenue growth. Its stock’s 10% surge partly reflects the group’s weak rating relative to the European advertising sector

- Shares of On The Beach, a UK mid-cap tourism operator that admits it has no sterling hedge, lost a quarter of their value, the most since their listing four years ago

- Microsoft leads heavyweight technology shares lower in U.S. trading, falling 1%. There’s a similar sectoral breakdown there as in Europe, though with more emphasis on defensive moves. Utilities, an industry investors typically reach for in times of trouble, rises 0.3%. Uber sinks 8% after delivering a slightly bigger quarterly loss—$5.2bn—on Thursday night than expected. Gross bookings and revenue also missed expectations, just days after key rival Lyft posted better than expected figures and upgraded forecasts

FX snapshot as of [9/8/2019 4:06 PM]

FX markets and gold

- Sterling is the biggest loser whilst the yen is the most in demand as a severe risk-off mood returns and markets sharply downgrade views of Britain’s economy after a shock growth contraction in the second quarter

- This was the first time GDP contracted since Q4 2012, thanks to increased Brexit uncertainty and weakening global growth. Meanwhile the latest manufacturing production (-0.2%) and construction output (-0.7%) numbers also disappointed

- The pound is heavy across the board, leaving the franc, Aussie, and the Canadian dollar as outperformers against sterling. The euro also rises sharply against the pound, though a more than moderate EUR/JPY drop betrays misgivings over developments in Italy

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM