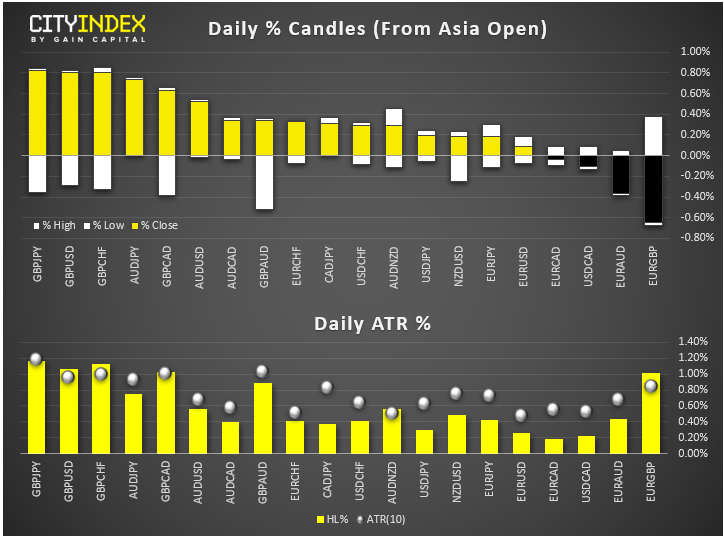

- At mid-morning London, the pound was the strongest among G10 currencies, followed by the Aussie, while the yen and US dollar found themselves near the bottom of the leader board.

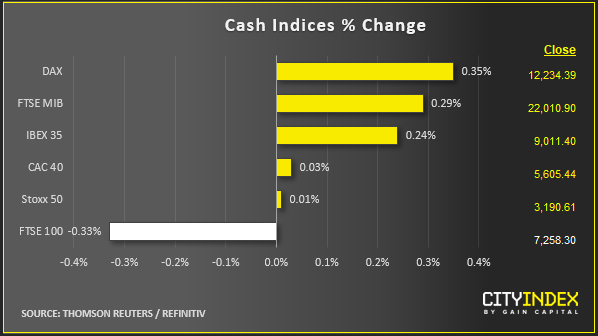

- Brexit, what Brexit? Pound rallied and the FTSE 100 struggled in an otherwise risk-on day for European markets this morning. A solid UK GDP figure surprised the markets. The Brexit-hit economy unexpectedly expanded by 0.3% month-over-month in July. Manufacturing production also rose 0.3%, while construction output jumped 0.5% m/m – both higher than expected. The Index of services likewise surprised with a print of +0.2% on a 3m/3m basis versus +0.1% expected.

- China’s exports unexpectedly contracted in August, hurt by US tariffs – decreasing by 1% in dollar terms, with the nation’s sales to the US declining by 16% from a year earlier. China’s imports fell 5.6%, although this was better than a decline of 6.4% expected.

- We are expecting a quietish session from the US with no major data scheduled for release. But the calendar should get busier later in the week. The main macro event is probably going to be Mario Draghi’s last policy meeting as the ECB President. Will he go out with a bang and introduce more stimulus? In addition, we have inflation figures from the US and more economic pointers from the UK. Read our week ahead report HERE.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM