FX Brief:·

- Inflation in Tokyo fell to a 16-month low, adding calls for more stimulus from BoJ at their upcoming meeting.

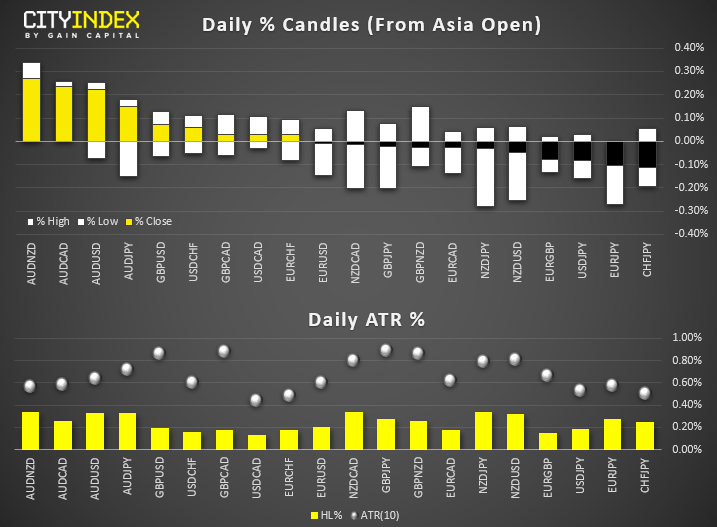

The four largest banks in Australia are now calling for RBA to cut next week to 75 bps. The ASX implied yield curve suggests around an 80% chance of a cut on Tuesday. - AUD and GBP are currently the strongest majors, CHF is the weakest. Ranges are narrow overall with none of the pairs we track coming close to testing their typical daily ranges.

- Traders will want to keep a close eye on where EUR/USD closes the week. Currently testing a key support trendline above 1.0900, a close above 1.0930 could suggest downside a bear-trap, at least over the near-term.

- Britain will be to blame if no Brexit deal is reached, according to EU’s Juncker.

- China’s top diplomat is saying that Beijing is willing to buy more products from the US.

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Equity Brief:

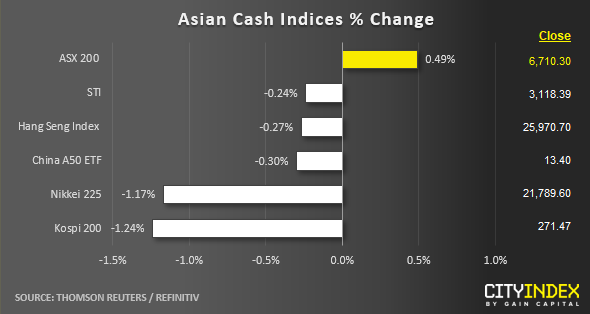

- Trump has blasted Democrats for their latest “witch hunt” and spent the night tweeting clips from Fox News which aim to undermine the impeachment proceedings. Asian equities fell to a 3-week low following the release of the Trump whistleblower complaint.

- The Nikkei 225 fell through the July highs to a 9-session low and currently trades -1.17% for the day. The ASX200 diverged and looks set to close higher for the session.

- US futures have opened slightly lower (ranging between –0.12% to -0.22%)

- BMW have ‘no interest’ in settling with EU antitrust authorities, after being accused of colluding with Daimler and Volkswagen to block the rollout of cleaner emission technology between 2006 – 2014.

- Toyota are to increase their stake in Subaru to over 20%, according to sources. Separately, Toyota are also planning to develop hydrogen fuelled cars with their Chinese partner FAW Group and Guangzhou Automobile Group.

- Huawei are claiming to have begun production of 5G base stations without US parts, a move which is likely to irk president Trump.

Up Next

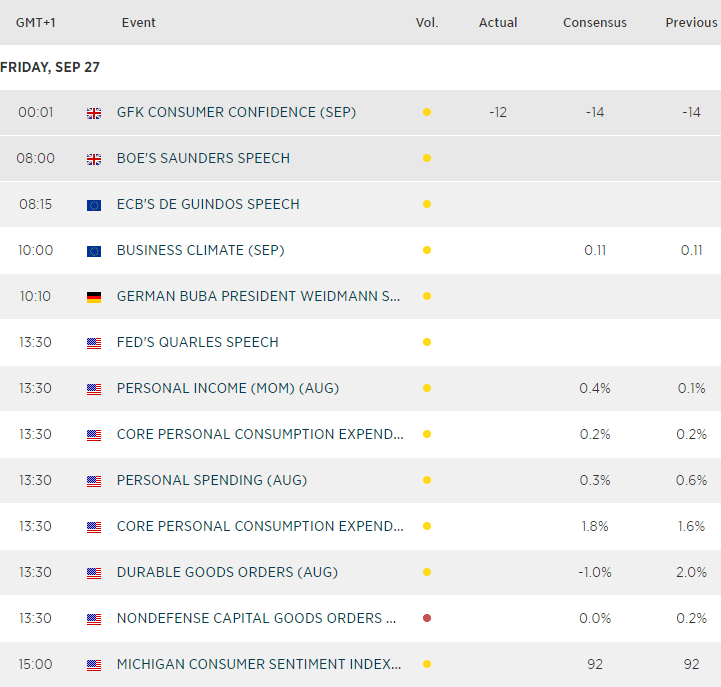

- No top tier economic data today means we could be in for a fairly quiet session. Unless of course Trump wants to stir things up, or the impeachment headlines begin to make a larger impact.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM