- Trade tensions continued to thaw with US and China both providing goodwill gestures; China decided to exempt some anti-cancer drugs and other goods from its US tariffs, Trump agreed to delay tariffs on $250 billion of Chinese goods from 1st to 15th October.

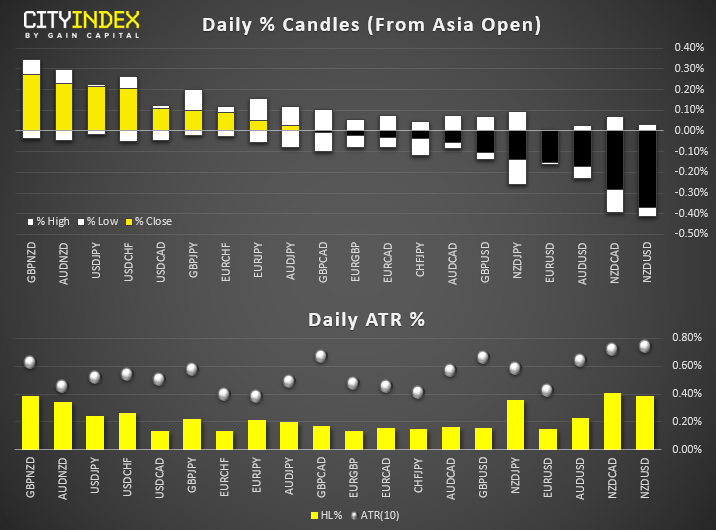

- NZD and AUD were again the strongest majors throughout Asia, JPY was the weakest. AUD hit fresh highs against safe havens CHF and JPY, tracking bond yields higher from their multi-year lows. EUR/NZD broke lower out of range ahead of today’s ECB meeting, NZD/USD tested this week’s high and shows potential for a bull-flag breakout.

- USD/PY broke its bearish trendline for the April high, although with several yen pairs testing key levels, we’re on guard for an interim inflection point. That said, with trade sentient continuing to blossom, it should provide another tailwind for risk and support markets such as indices, carry trades and commodities (excluding silver and gold).

- Wholesale prices in Japan contracted by -0.9% year over year, below the -0.8% expected and down from -06% prior. With prices having peaked in 2018, and machinery orders also contracting, it adds to expectations that BOJ may provide more stimulus. Especially with reports floating around that BOJ may expand their program at next week’s meeting.

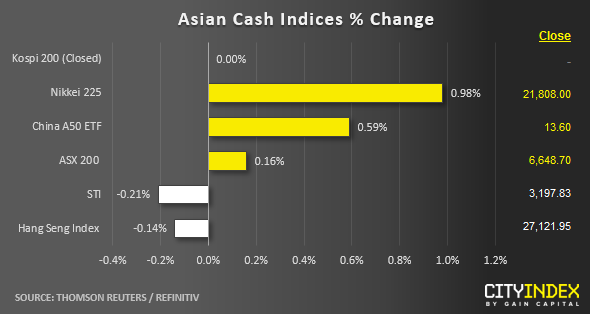

- Most Asian stock markets have extended their gains in today’s Asian session after U.S. President Trump said he will delay the additional 5% tariffs on US$ 250 billion worth of China imports from 01 Oct to 15 Oct as a gesture of goodwill before the upcoming trade negotiation talk takes place in Washington later in Oct.

- The top performer so far is Japan’s Nikkei 225 where has rallied by close to 1.00% to hit a 3-month high with semiconductor and robotics manufacturers that are closely dependent on China’s demand leading the rally. Fanuc Corp, Keyence Corp and Advantest have rose to 2.2%, 1.4% and 4.4% respectively.

- Interestingly, value-oriented stocks such as banks and automakers that have led the rally in Japan stock market since last week have started to see profit taking activities where banking stocks have declined by -0.3% on the average after it has rallied by more than 10% in the past 5 days.

- The weakening USD/CNH (offshore yuan) is also supporting the on-going “risk on” sentiment where it has slipped by close to 400 pips to print a current intraday low of 7.0732 in today’s Asian session.

- The S&P 500 E-min futures has also extended its gain from yesterday’s U.S. session; it has inched up by 0.40% in today’s Asia session to print a current intraday high of 3019, just a 0.3% whisker away from its current all-time high of 3029 printed on 26 Jul 2019.

Up Next:

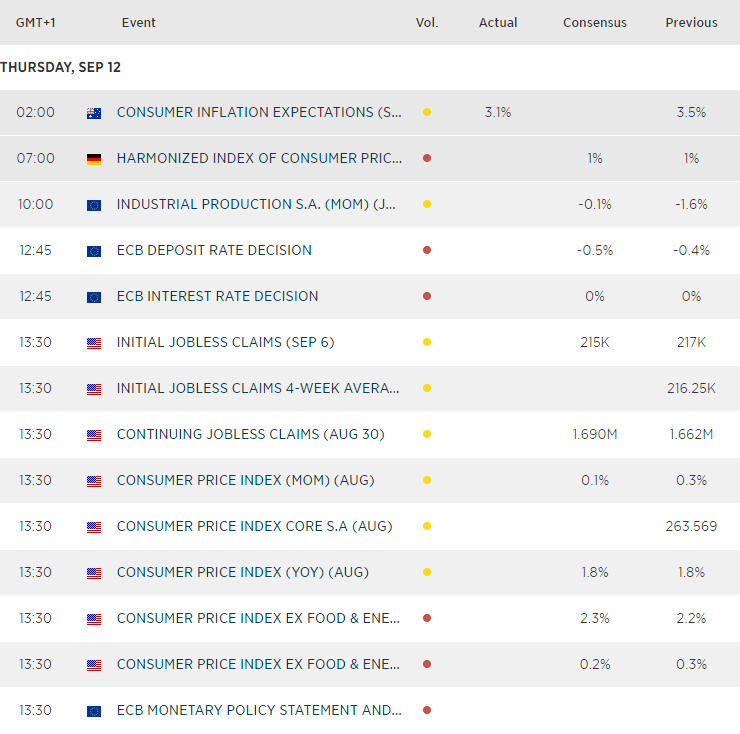

- Today (and pretty much this week) is all about today’s ECB meeting. Whilst a 10bps cut is expected, a 20 bs cut is not off the table. Moreover, we could see QE reintroduced and ECB venture into equities. Will Draghi leave rom for his successor to introduce the latter, or simply go out with a bang? We’ll find out I a few hours, which puts Euro pairs, bonds and indices into the limelight.

- Germany CPI data for Aug where consensus is set at 1.4% y/y and -0.2% m/m over Jul data of 1.4% y/y and -0.2% m/m respectively.

- US inflation data will be the next major event today, with CPI expected to rise to 2.3% YoY. If the consensus is correct, it will be the highest rate of inflation since June 2018 and likely lower expectations of a 25 bps cut from the Fed next week (although we still expect the Fed to cut).

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM