- News that US and China are set to resume trade talks in Washington next month extended yesterday’s relief rally.

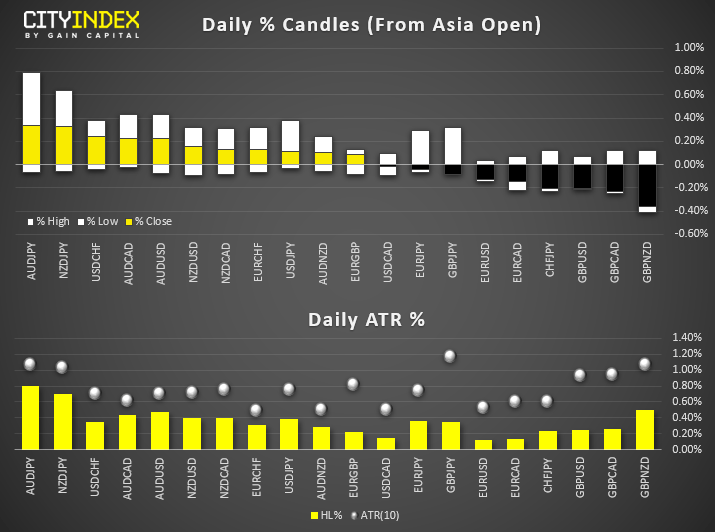

- Commodity currencies (AUD, NZD and CAD) were quick to react and are today’s strongest majors. AUD/USD rebounded to its highest level since 1st August although has stalled beneath 0.6832 resistance – a pivotal level traders should be keeping an eye on.

- The positive sentiment also saw PBOC weaken their FIX ad allow USD/CNH to fall to an 8-day low. USD/JPY hit resistance at 106.78, GBP/USD remains within its bearish channel but could be headed for a break higher. WTI trades in a tight range around $56. Gold and silver remain stubbornly high, despite the weaker USD pricing, although both trade slightly lower for the session.

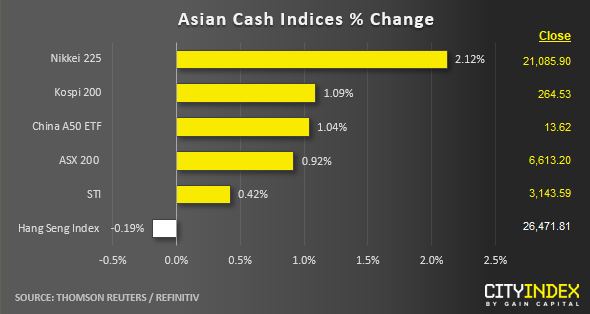

- Equity markets were broadly higher on trade optimism today, adding to yesterday’s relief rally fuelled by improved Chinese data and Hong Kong’s withdrawal of the extradition treaty.

- The rebound was led by Japan and China, with the Topix and CSI gaining 1.84% and 1.62% respectively. The exception to the rally was the Hang Seng Index (HSI) which trades -0.13% lower. Index futures are also pointing higher, with the S&P500 E-mini breaking to a 1-month high.

- The Hang Seng, which rallied over 3.7% yesterday when Hong Kong’s PM officially withdrew the extradition treaty, failed to extend gains today. Whilst the withdrawal was a step in the right direction, protestors still want their four remaining demands met. Three of which include the PM stepping down, HK having control over the selection of a new leader and the end to police brutality

Up Next:

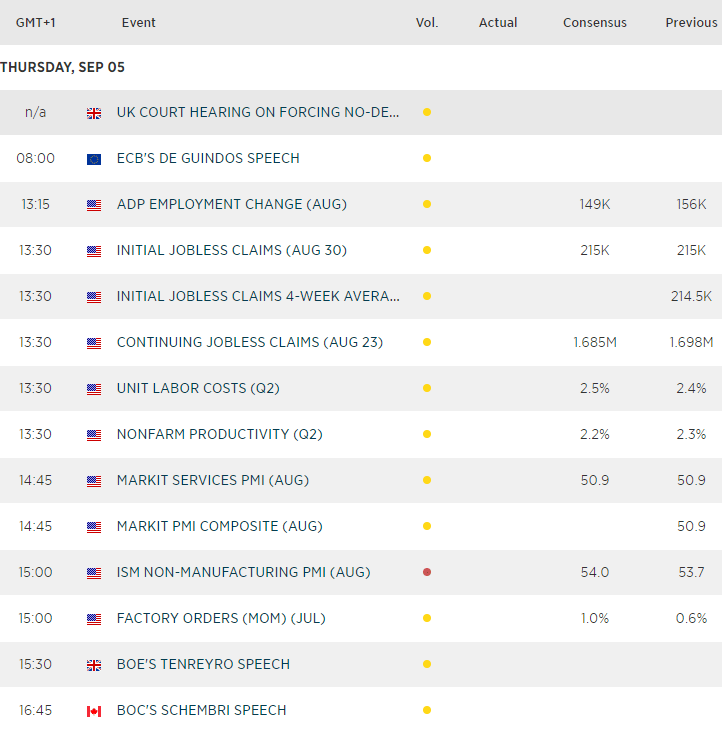

- UK's PM Boris Johnson is set to 'speak to the public' around 3pm GMT today, and is expected to say he wants an election and that the "surrender bill" would effectively overturn the largest democratic bill in he UK's history.

- ISM non-manufacturing (services) is expected to rise to 54 from 53.7 prior, although the weak print from ISM manufacturing could have traders on edge for a soft print from services today. Whilst it remains expansive at 53.7, it has nose-dived since peaking at 60.8 in 2018. Keep USD crosses and US indices on your radar around this release.

- ISM aside, it’s mostly 2nd tier data, so it could be trade which remains at the forefront for traders. This places commodities, commodity FX and JPY pairs on trader’s radars.

Latest market news

Latest Forex articles

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM