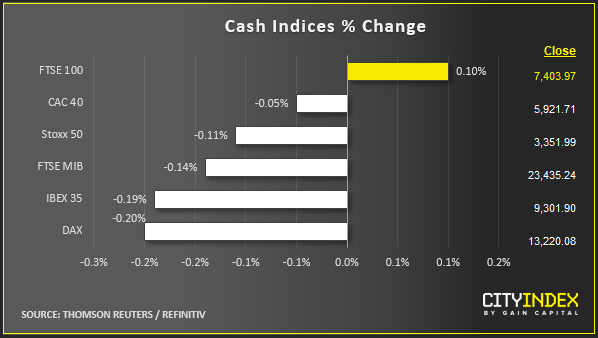

- Market update at 11:45 GMT: In FX, USD was the strongest and GBP the weakest in a lacklustre session. European stock indices and US index futures were mostly lower, with the exception of the FTSE which was supported by a weaker pound. Gold and silver rebounded as benchmark government bond yields edged lower. Bitcoin fell back after yesterday’s short-covering bounce. Crude oil was up a little.

View our guide on how to interpret the FX Dashboard

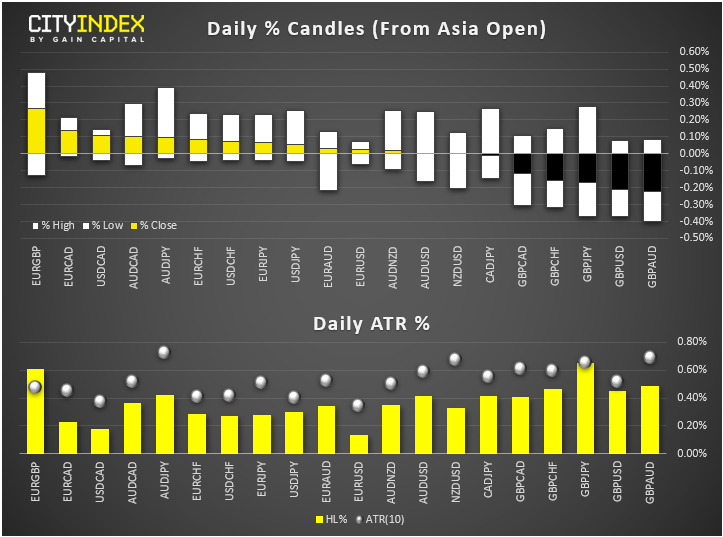

- GBP fell on the back of an opinion poll by Kantar showing support for Tories weakened a little in favour of Labour. Tories still lead by 11 points.

- AUD rose then fell back as RBA’s Lowe said "...we have no appetite to undertake outright purchases of private sector assets as part of a QE program". But if they did, Lowe says they "would purchase government bonds, and we would do so in the secondary market." Was that a hint of looser policy to come?

- NZD was unable to break through key resistance circa 0.6425 despite data showing New Zealand retail sales rose in the third quarter by 1.6%, beating expectations of 1.5% and up from 0.2% prior.

- Stocks: Unfortunately, once again, the focus remains firmly fixated on US-China trade negotiations, as there’s very little in the way of key macro data or other major news to drive sentiment. On that front, talks continue and apparently the two sides have reached a degree of consensus about resolving the issues standing in the way of a phase one trade deal. Given this doesn’t actually cover any new ground at all, there has been very little market reaction. Indeed, index futures initially rallied to fresh highs overnight before paring their gains as Asia sold off, leading to a weaker open in Europe. US index futures were little changed.

- Stocks in focus by my equity market expert colleague Ken Odeluga:

○ A big slate of UK groups with results saw Topps Tiles tank the most. It blamed the upcoming general election for increasingly challenging trading conditions that unexpectedly trashed same-store sales growth, sending the shares as much as 11% lower.

○ Building materials supplier CRH rose 2.8%, after pitching full-year underlying earnings guidance above the market's forecast of €4.15bn. 9-month sales rose 9.5% on the year.

○ Utility group Pennon rose 1.7%, after H1 results were in line with forecasts, with revenues down 4.6%.

○ Full-year revenues from catering services firm Compass also met expectations but its shares tumbled 5.6%. The £31bn group noted it would adjust its cost base amid a deteriorating environment in Europe

○ US firms reporting ahead of Wall Street's open include Hormel Foods. Its Q4 earnings and net sales met forecasts, though it raised its 2020 sales outlook above estimates. The shares trade slightly higher pre-market.

○ Best Buy is also set to report ahead of the US open.

- Coming up: A hand full of second tier US macro data including trade balance and wholesale inventories at 13:30 GMT, followed by CB consumer confidence, Richmond Manufacturing Index and New Home Sales at 15:00 BST. FOMC’s Brainard will be speaking at 18:00.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM