View our guide on how to interpret the FX Dashboard

FX Brief:

- Volumes were lighter due to the public holiday in Japan today.

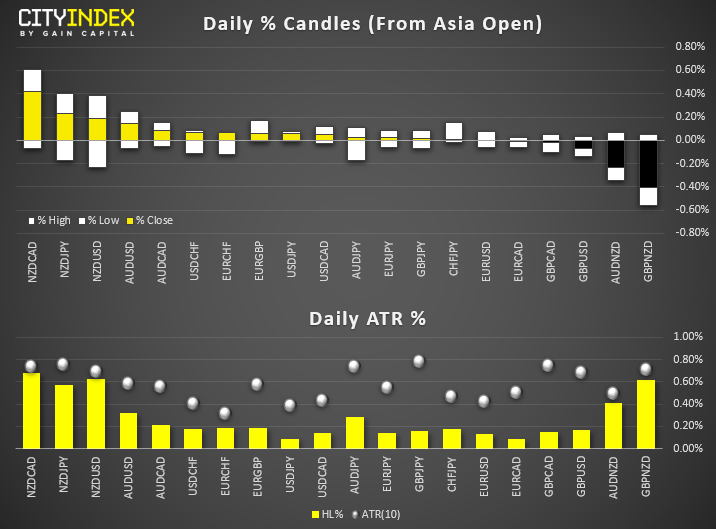

- NZD is the strongest major on the announcement that New Zealand has concluded its negotiations to upgrade their free trade deal with China. NZDCAD is today’s biggest gainer, and its daily range has hit 91% of its 10-day ATR. NZD/USD touched a fresh 3-month high.

- Trade optimism has seen the Yuan strengthen and send USD/CNH to it lowest level in 3-months.

- Australian retail sales declines -0.1% in Q3, showing further signs that tax brakes and record low interest rates are failing to prop up the economy. ANZ job adverts also declined by -1%. Take note that AUD/USD has paused beneath a long-term bearish trendline ahead of tomorrow’s RBA meeting. Whilst there’s no expectation of a cut, a dovish statement could topple the Aussie.

- EUR/USD is trading in a tight range just off last week’s highs ahead of European PMI data and a speech from ECB’s Christine Lagarde. USD/JPY is trapped between the 20 and 50-day eMA, near Friday’s high.

Equity Brief:

- Another bout of U.S-China trade deal optimism news flow coupled with a strong U.S. job/non-farm payroll data for Oct reported on last Fri, 01 Nov have continued to lift Asian stock markets at the start of a new trading week.

- U.S. Commerce Secretary Wilbur Ross expressed optimism over at a media interview over the weekend that U.S. would reach an agreement on the “Phase 1 of the trade deal” with China by this month and mentioned licenses would be issued very shortly for U.S. companies to sell components to “blacklisted” Huawei Technologies Co.

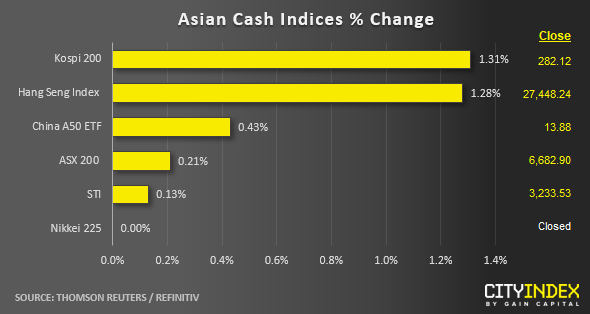

- The best performers today are South Korea’s Kospi 200 and Hong Kong’s Hang Seng Index as both have rallied by around 1.30%. Japan’s Nikkei 225 is closed today for a public holiday. The Kospi 200 has hit a 4-moth high of 282.49 led by the financials and industrials sectors that have gained by 2.31% and 1.79% respectively.

- Hong Kong’s stock market has shrugged off a series of violent street protests over the weekend that caused two people in critical conditions. More demonstrations are planned for this week that includes Guy Fawkes Day on 05 Nov by putting on banned face masks in the streets of Hong Kong.

- Both Singapore’s Straits Times Index (STI) and Australia’s ASX 200 has only gained modestly by 0.13% and 0.20% respectively. The ASX 200 has been dragged down by financial shares again where the big 4 banks; CBA, NAB and ANZ have dropped by -1.72%, -3.03% and -0.65% respectively. Westpac shares are halted for trading after it has announced a A$2.5 billion capital raising in fresh equity to bolster its balance sheet. In addition, Westpac also reported a 15% decline in full-year cash earnings and cut its dividend pay-out for the first time in a decade.

- The S&P 500 E-mini futures has continued to inch higher by 0.22% in today’s Asian session to print another fresh all-time high of 3071 with a current intraday low of 3064.

Up Next:

- The Euro will be in focus as new ECB head Christine Lagarde delivers her first official speech.

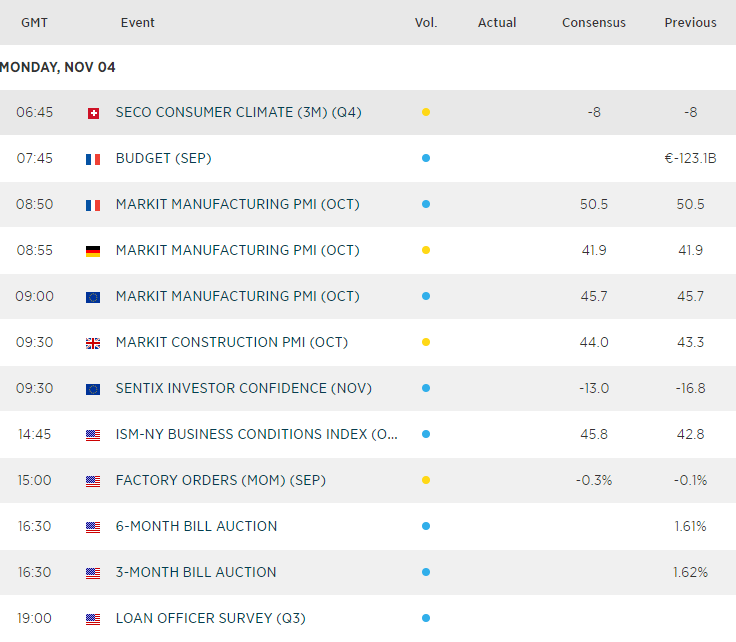

- German PMI data is expected to remain firmly within contraction (below 50) at 41.9. The broader EZ read is also expected to remain within contraction at 45.7, with France bucking the trend to remain slightly expansive at 50.5. So Euro pairs have plenty to keep an eye on later this session.

- UK construction PMI is expected to weaken further to 44 versus 43.3 prior.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Dollar articles

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM