FX Brief:

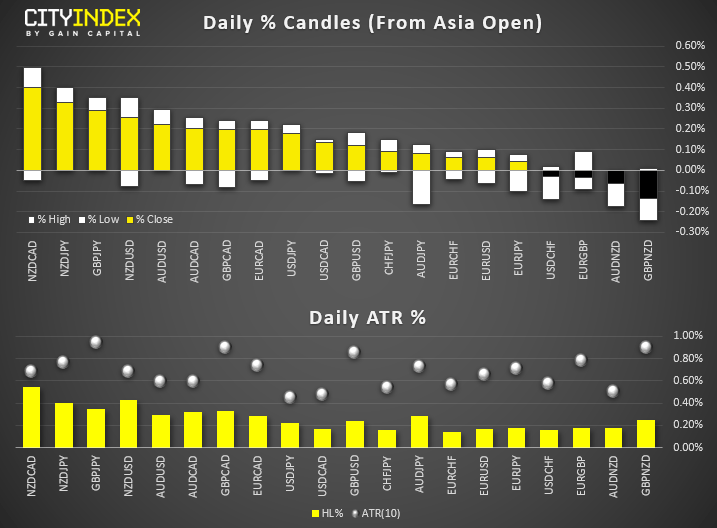

- A public holiday in Japan saw volumes lower than usual in today’s Asia session. At time of writing, all majors and crosses remain well within their typical daily ranges (leaving potential meat on the bone for the European and US session).

In contrast to the second half of last week, NZD and AUD are the strongest majors whilst JPY is the weakest. - All majors remain within Friday’s ranges. This has allowed NZD/USD to retreat marginally from four-year lows, although given the lack of volatility, is too difficult to read too much into the moves until volumes return.

- Australian’s manufacturing PMI contracted in September, although services reverted to growth to lift the composite PMI back above 50.

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Equity Brief:

- Thomas Cook group, the world’s oldest travel firm collapsed after rescue talks broke down over the weekend. This brings an end to the 178-year travel company, which survived two world wars and leaves thousands of holiday makers stranded. AlixPartners have been appointed to manage the administration, subject to the approval of courts.

- Softbank Group are exploring ways to replace WeWork’s CEO Adam Neuman, after delaying its IPO last week.

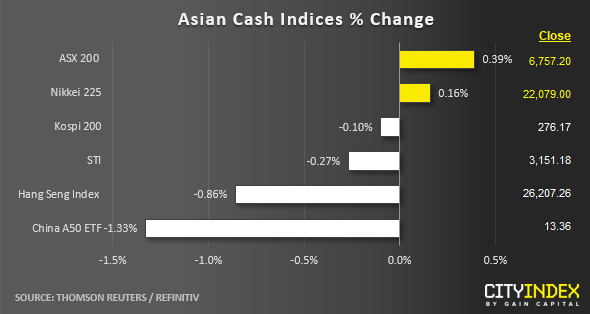

- Asian equities were broadly higher according to MSCI indices, on hopes that talks between US and China were improving, with both countries describing them as “productive” and “constructive”.

- At the index level, China’s CSI 300 and the Hang Seng were down -1.3% and -0.86% respectively, whilst the ASX200 was higher with rising expectations of an RBA cut in October. S&P500 E-mini futures also climbed 0.5%.

Up Next

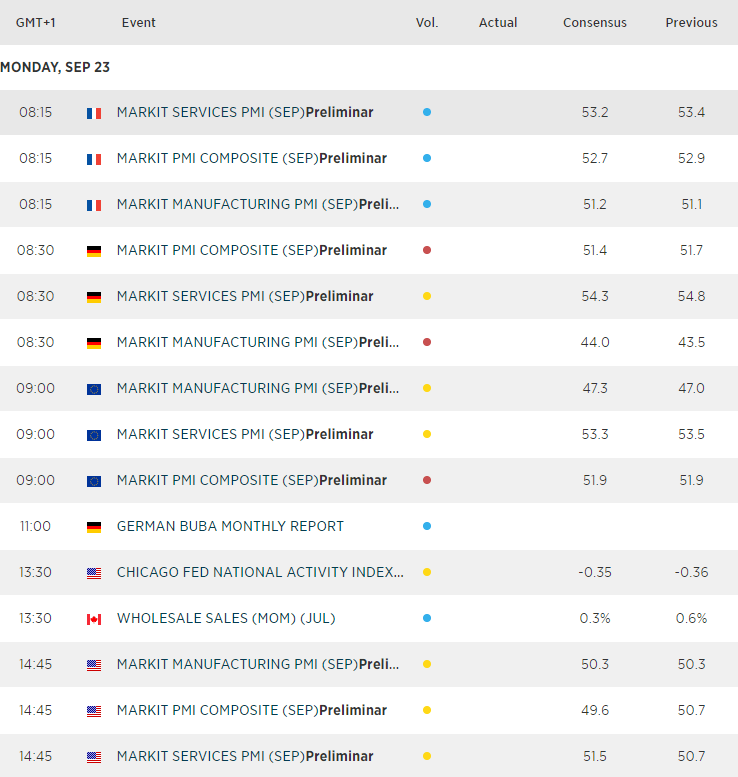

- It’s all about PMI’s with France, Germany and data for the Eurozone due to be released.

- Of the three, France bucks the trend with growth in both the manufacturing and service sectors, whist Germany the Eurozone manufacturing reads remain in contraction.

- Later the US also release PMI data for manufacturing and services. Given the ISM manufacturing read was a negative print in August (below 50) traders will keep a close eye on the Markit read to see if it confirms the negative print for the sector. Keep EUR/USD on the radar around these reads.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM