FX Brief:·

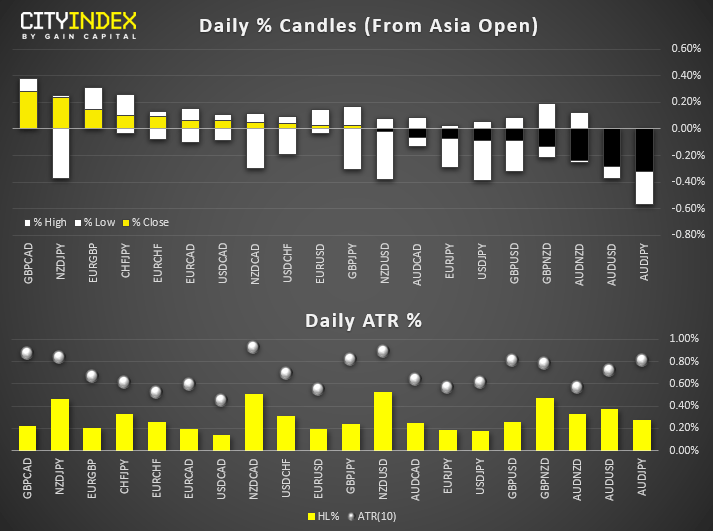

- It was the usual narrow ranges ahead of today’s NFP report, although NZD is currently the strongest major and largest mover. (CHF is the weakest). NZD/CAD extended its bullish reach to a 3-week high and a 6-day high against the dollar.

AUD is firmer on stronger retail sales and sit at a 3-day high against the greenback. AUD/CAD has touched a 6-day high. - The RBA flagged the housing market as a key source of potential systematic risk which needs to be monitored closely. And unemployment and ongoing weak income growth is a risk to the housing market. However, the resilience within the financial sector has improved.

- RBA’s Ellis said that flat-to-falling retail prices are a big change in pricing behaviour for some parts of CPI, and that the strong performance in wage growth for the public sector is expected to be a one-off.

- Fed member Clarida says they’ll certainly be discussing standing repo facility in recent meetings and that a 25-bps cut in September was appropriate. He sees the economy and consumer are in a good place and growth is solid, and that President Trump’s Tweets don’t effect monetary policy.

- Fitch ‘cannot rule out’ further easing from BOJ.

Equity Brief:

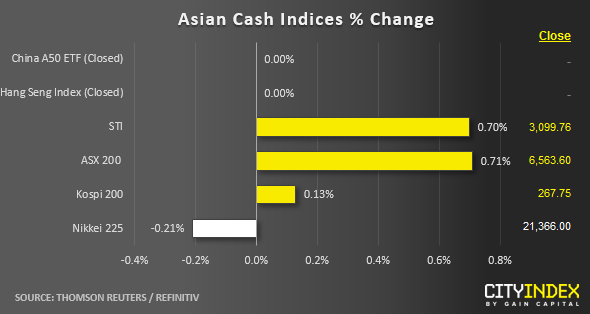

- Most Asian stock markets have managed to recoup some of the losses inflicted over the past 3 days, taking the cue from a positive performance seen in the key U.S. benchmark stock indices overnight where the S&P 500 and Nasdaq 100 have rallied by 0.80% and 1.16% respectively.

- The current turnaround can be attributed to the expectations set by market participants on the U.S. central bank, the Fed to be more dovish on its monetary policies in the near future after yesterday’s lacklustre U.S. ISM Services PMI data for Sep (52.6 versus 55.00 consensus & a decline from 56.4 seen in Aug). Coupled with a horrendous print on the ISM Manufacturing PMI, markets are expecting more interest cuts from the Fed where the Fed funds futures has indicated 88% probability of another 25 bps cut after the 30 Oct FOMC meeting, up from a 49.2% chance seen last week according to the CME FedWatch tool.

- The Hong Kong’s Hang Seng Index has failed to capitalise on the positive performance seen in the U.S. stock markets due to localised factors. It has declined by -0.45% after the SAR government is looking to implement a certain form of emergency rule for the first time since 1967 that will ban face masks for protestors in public. The law is expected to be passed today where social media accounts have indicated anti-government protestors are planning demonstrations today and over the weekend as a form of defiance. Major property developers’ stocks are leading the decline so far with Sun Hung Kai Properties and CKH Holdings have dropped by -1.93% and -1.36% respectively.

- The S&P 500 E-Mini futures has continued to hold onto its overnight gains where it has managed to inch up higher by 0.10% in today’s Asian mid-session to print a current intraday high of 2918 that has surpassed yesterday’s U.S. session high of 2911.

Up Next

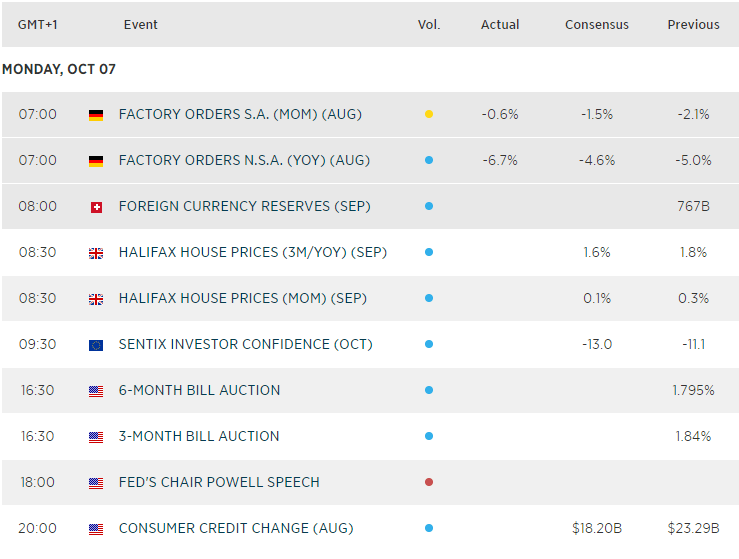

- Today’s Nonfarm payroll report is the main game in town today, where the consensus is set for an increase of 145K. The latest set of data from ISM has indicated a deterioration in growth on U.S. manufacturing and services sectors, thus a weaker than expected print in NFP increases the odds of a more dovish Fed which may see a further weakening of the USD and a continuation of the bounce in U.S. stocks.

- Canada's Ivey PMI shot up to an 11-month high in September, so we’ll find out if it was a fluke or whether strength will be maintained (and Canada remain the envy of weak global PMI reads). Lee CAD crosses on your radar, as a stronger print should be bullish / weak print bearish for the Loonie.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Yesterday 08:33 AM

Latest Dollar articles

Yesterday 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM