Stock market snapshot as of [28/8/2019 6:08 PM]

- One key government in the EU, for now, could be headed for collapse. Another one could do the same, though a new, less rancorous administration could swiftly take its place. Those are the backdrops in the UK and Italy respectively, for a moderate rally of British blue-chip stocks and a small dip of Rome’s FTSE MIB. In other words, Wednesday’s big political dramas weren’t strongly reflected in stock markets

- That’s certainly true more broadly. U.S. shares are on a stronger footing, though the Nasdaq’s flagship index was the weakest with a 0.2% rise a short while ago, compared to the Russell’s 1.4% jump. Dow gained 0.8%

- Principal European indices spanned a narrow range between lacklustre gains and small losses, with the export-led FTSE 100 out in front, getting its customary lift from sterling’s biggest setback for weeks. Most continental markets were lower though, largely in a holding pattern. Partly this was on a wait for definitive news out of Italy. Latest reports suggest that leaders of a new potential coalition, excluding the right-wing Northern League which called for snap elections, will shortly meet Italy’s Head of State, President Sergio Mattarella. Mattarella’s traditional role is to appoint and dissolve governments. He could soon do both in quick succession. It’s reported that the centre-left Democratic Party has dropped opposition to the reappointment of Giuseppe Conte as Prime Minister, after he quit a few weeks ago due to the 5-Star/League’s deteriorating partnership

Stocks/sectors on the move

- Energy shares are doing much of the heavy lifting Stateside, as the official weekly U.S. energy administration report backs up industry data to show a much bigger crude oil inventory drawdown than traders were expecting. Brent and U.S. crude were futures were up more than 1% a piece. S&P 500’s Energy sector led all others with a 1.4% gain, followed by Materials and Financials, both up 0.9%

- Regional banks and financial firms like BB&T and Citizens shine the most, suggesting investors are remaining selective about buys in the sector, opting for those with the least international exposure

- With Big Techs underperforming, the sceptre of the trade dispute is not far from investors’ minds. Cloud software groups Autodesk and Adobe led the tech downside falling, 8.2% and 2.4%, with the digital design/marketing application giant following its smaller rival lower after Autodesk’s meeker than expected outlook comments

FX snapshot as of [28/8/2019 6:08 PM]

FX markets

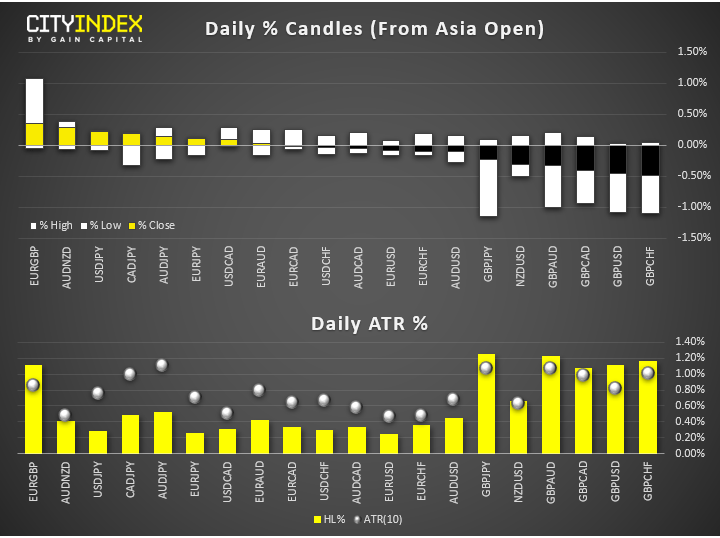

- Sterling is stuck on the backfoot against all majors and most minors as the market prices the latest twist in the Brexit saga

- Besides that, only the Canadian loon looks a standout on the back of crimps emerging in global oil supply lines, which could push up prices of that country’s biggest export

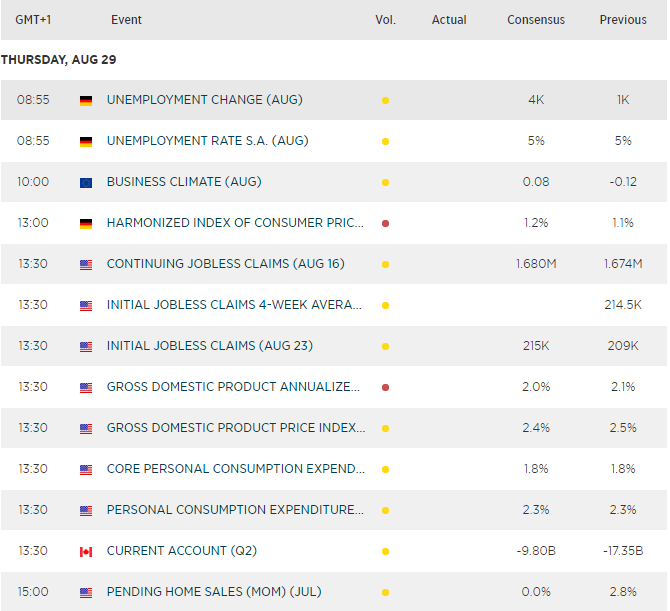

Upcoming economic highlights

Latest market news

Today 08:15 AM

Today 05:45 AM

Latest GBP articles

April 3, 2024 02:49 AM

March 29, 2024 10:00 PM

March 9, 2024 04:00 PM

October 24, 2023 02:20 AM