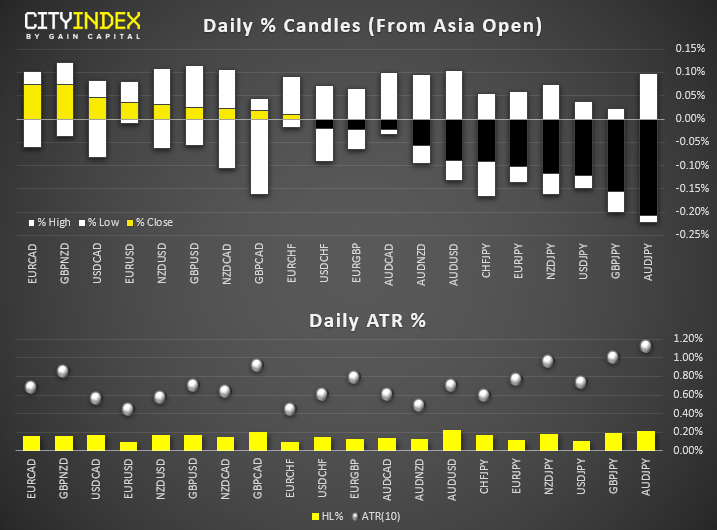

- AUD and NZD are today’s strongest major after the release of RBA's August minutes. Whilst little new could be gleaned from them, the lack of any dovish surprise helped support the Aussie after their release.

- Narrow ranges once again overall due to the lack of first tier data. However, a cautious approach is expected ahead of the Jackson Hole symposium and keynote speeches from Central Bank governors.

- PBOC Vice Governor Liu says future interest rate policy focus will be on LPR (loan prime rate), and benchmark rates may not be changed over the near-term

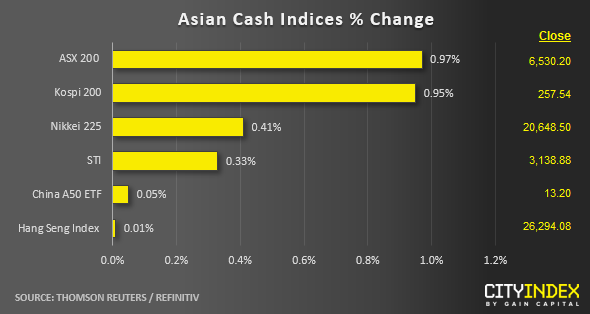

- Ahead of the European session open, most Asian stock markets have continued to inch higher for the second consecutive day on the backdrop of more stimulus hopes from major developed central banks.

- The Australia’s ASX 200 and South Korea’s Kospi 200 are the star performers as at today’s Asian mid-session where both indices have rallied by close to 1.00%.

- The outperformance seen in the ASX 200 has been led by the energy sector which has gained by 2%. Over at Kospi 200, the energy and technology sectors are leading with gains of 1.87% and 1.43% respectively. In addition, the on-going optimism seen in the South Korean’s stock market has been fuelled by a positive regulatory news flow where the Vice Finance Minister has announced today that South Korea may consider easing market restrictions on share buy-backs, while tightening short-selling rules to stabilise local markets.

- The S&P 500 E-mini has inched up higher by 0.21% in today’s Asia session after three days of consecutive gains since last Thurs, 15 Aug. Overall, the U.S. stock market has almost recovered the losses inflicted by the yield curve inversion seen on the 10 year and 2 year Treasuries (US govt bonds) on last Wed, 14 Aug.

Up Next:

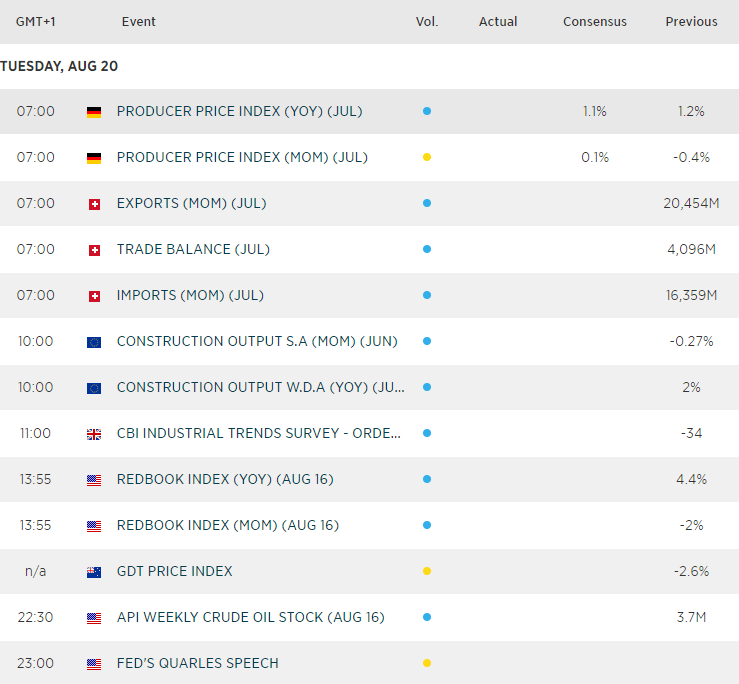

- German producer prices were flat in the month of June and the YoY% rate is polled to drop to 1% (from 1.9%) to take it to its lowest rate of growth since December 2016.

- Late US session sees dairy prices and milk auctions, which puts NZD crosses on trader’s radars.

Matt Simpson and Kelvin Wong both contributed to this article.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM