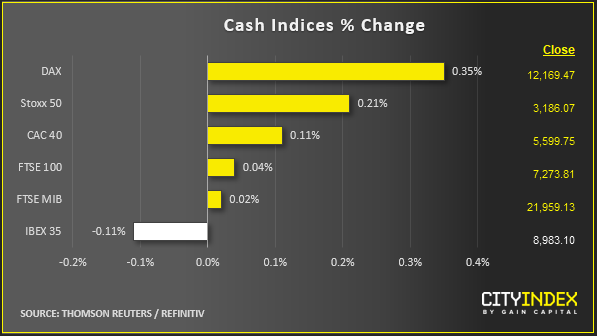

Stock market snapshot as of [6/9/2019 4:13 PM]

- Weaker than forecast U.S. jobs data are the first challenge to recently improved risk appetite. Stock markets are faring better than the dollar which faced sharper setbacks, including against the Canadian dollar. Job growth diverged relative to expectations between the neighbouring countries, with Toronto reporting a massively above forecast 81,100 in August compared to the 130,000 posted by Washington’s BLS. Payrolls expectations had ranged between 160,000 and 150,000

- Revisions also trimmed employment gained in July to 159,000 compared to 164,000 reported last month. With U.S. Census-related hiring thought to have inflated recent readings, underlying growth might even be trending further to downside than thought

- The read for rate-policy expectations ahead of next week’s Federal Reserve decisions is mixed, particularly after wages growth surprised to the upside with a rise of 0.4% on the month, above the long-standing run rate of 0.2%-0.3%. Futures markets have baked in another 25 basis-point Fed funds rate and disappointment is unlikely. However, with policymakers’ commentary increasingly ambivalent, signs that consumers’ earnings may be strengthening could sow fresh doubt on the policy outlook beyond this month

- Still, although stock markets headed to their lows in reaction to the data, most retain a positive tilt. Treasurys nevertheless erased losses, enabling yields to weigh on the dollar anew. Absent an unexpected development on the trade front, only a speech by Fed chair Jerome Powell, a little later, has the capacity to darken the mood. Likewise, European shares are posting a third week of gains even after paring their advance like Wall Street

- On Friday, the People’s Bank of China cut the Required Reserve Ratio for banks by 50 basis points whilst noting that it intends to make further 50bp cuts of the RRR in coming months. The news was not a major surprise as it has been well flagged, though still underpinned risky assets

- In London a High Court judge threw out a second legal challenge against Prime Minister Boris Johnson’s planned suspension of Parliament. Even so, sterling is holding on to most gains in a recovery by more than 3% since early-week lows. Investor focus remains on dwindling chances Johnson’s government has of taking Britain out of the European Union without a deal on 31st October. Opposition parties have agreed they will try to scupper government plans for a mid-October election, ahead of a vote on that question in Parliament on Monday, according to reports. Instead, Labour, the Liberal Democrats and others, favour a late-October election at the earliest. A vote of no confidence in the government also now looks less likely in the immediate future

Stocks/sectors on the move

- European share buyers strongly favoured China-related natural resource shares, enabling STOXX’s Metals & Mining sector index to outperform. However, paper and packaging producer, Ireland’s Smurfit Kappa, inflated the aggregate rise of Materials with a gain of more than 4%. Its bond offering, at relatively advantageous rates as fixed-income yields trend lower, will provide it with much cheaper financing. Physical security and business services firm G4S is another standout with a 7% rise on news it’s in talks to dispose of its cash guarding business. A mixture of Consumer and Health Care names also outperformed

- Standout S&P 500 industrial segments seem even more on the defensive side, with Real Estate leading and Healthcare also near the front. The broad technology grouping underperformed, though was still in the green at last look, as Semiconductors, Hardware and Software rose 0.1% or less. ‘Interactive Media’, AKA Facebook, Google, Twitter and others continued to experience a recent bias for reduction, losing as much as 2% a piece

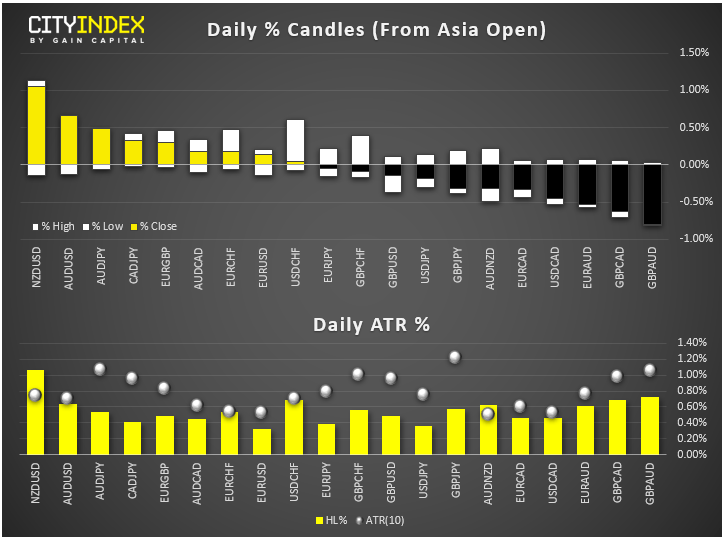

FX snapshot as of [6/9/2019 4:13 PM]

FX markets and gold

- Sterling’s fightback is still on, though a mixed job report has ironically bolstered the dollar on an intraday basis. This looks down to a perceived reduction in the urgency of additional Fed rate cuts after the one almost 100% priced in for next week, on the back of better than expected growth in average employee earnings. The risk-associated Aussie surged higher against the pound, yen, Kiwi, and greenback earlier before paring if not losing gains in the wake of the stronger hourly wage growth in August

- The top commodity currency is continuing to reflect improving prospects that the trade war could soon begin to calm, following news that Washington and Beijing have largely agreed to continue negotiations in October, with China’s vice premier Liu He set for another U.S. visit sometime in October

- Canada’s Loon is another standout, spiking up to fresh monthly highs after that country’s much better than forecast employment gains in August

- The gold rally to multi-year highs that has appeared threatened with the beginnings of a fierce retracement in recent days looks more on track, in reaction to the payrolls miss. Spot bullion completely erased the loss it faced for the week and last stood around $3 higher, at $1,522, closer to this week’s $1,557 6½-year high

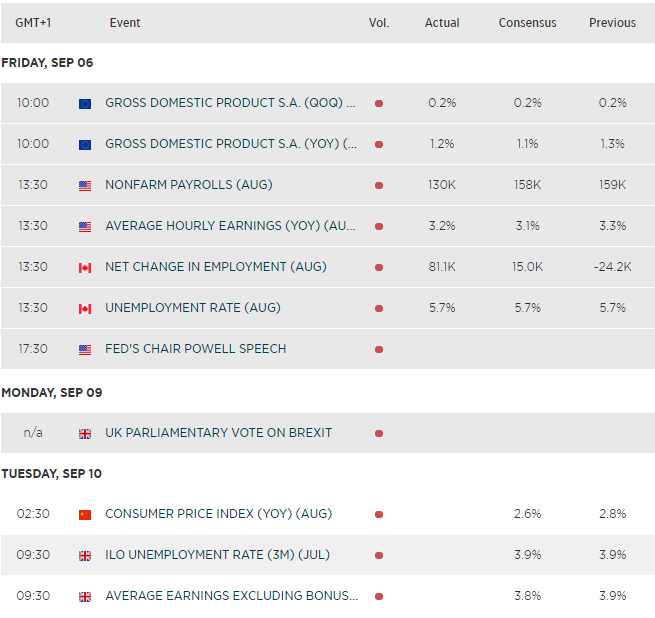

Upcoming economic highlights

Latest market news

Today 08:33 AM

Latest Interest rates articles

March 7, 2024 03:34 PM

February 9, 2024 04:37 PM

December 13, 2023 08:10 PM

November 27, 2023 08:19 PM